Stuck in a range – case for growing divergence still not compelling

EUR: Strong euro-zone data matches the US

As we highlighted here last week, since the start of 2023 roughly 90% of the time since EUR/USD has traded in a 5-big figure range between 1.0500-1.1000 and despite the continued expectations of a ‘higher for longer’ Fed monetary stance fuelling renewed US dollar strength, it still has not materialised. The FOMC minutes on Wednesday that highlighted increased concerns over monetary policy not being restrictive enough certainly highlights the risk of another leg higher in yields if the US economy doesn’t start to slow more meaningfully.

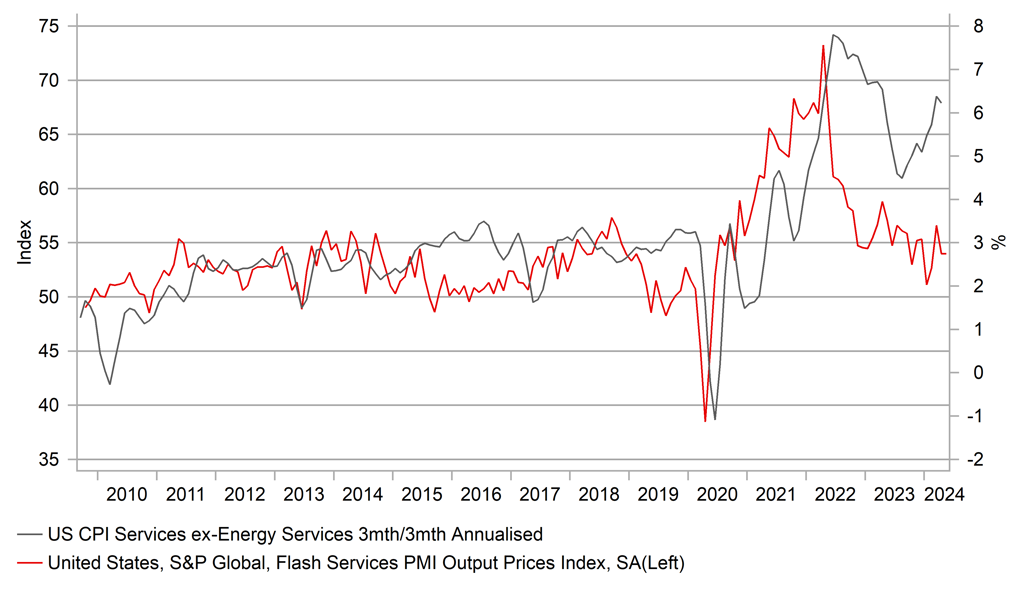

The FOMC minutes may have increased the sensitivity of US yields to any signs of economic strength or higher inflation. We were somewhat surprised by the reaction to the PMI data from the US. It tends not to prompt as much reaction as the data in Europe given the ISM data is the business survey data most watched. But the Services PMI was certainly strong – gaining from 51.3 to 54.8. Some of the breakdown was less alarming however with the employment index rebounding from 47.3 to 49.4, still below the 50-level – the first consecutive readings below the 50-level since June 2020 in the midst of the pandemic turmoil. So the data is still consistent with a weakening labour market. Secondly, as the chart above indicates, the PMI Output Price index remained subdued – and was unchanged at 54.0. It certainly doesn’t change the signalling of the data, which is for renewed disinflation going forward.

So again we are little but surprised by the extent of the move on the back of the US PMI data and our sense is that this in part at least reflects the FOMC minutes that revealed increased concerns over whether policy is restrictive enough which could over the short-term at least result in greater sensitivity to any incoming strong data.

Offsetting the PMI data from earlier in the day was of course the PMI data in Europe. Again, we continue to see evidence of a mild recovery taking hold as the negative consequences of the energy price shock fade. The euro-zone services employment index jumped from 53.2 to 53.7, which was the highest level since June 2023. Despite better signs of activity, the inflation readings remained subdued. The Output Price index fell to 54.1 in May, the lowest level since May 2021. That may ease some concerns that have possibly increased after the release yesterday of negotiated wage data that revealed the YoY rate accelerated from 4.5% to 4.7% in Q1. The data we believe is consistent with the June rate cut going ahead (it’s hard to back-track now) but then likely skipping another cut in July. Incoming data will then dictate cuts following the summer break but we by then would expect a similar trajectory of cuts from the ECB and the Fed. Assuming we avoid a further rebound in inflation and see some further moderation in employment growth, it is hard to see conviction of divergence and hence EUR/USD moves will remain contained.

STRONG SERVICES PMI BUT INFLATION INDEX SUBDUED

Source: Macrobond, Bloomberg & MUFG Research

JPY: But BoJ policy stance leaves JPY vulnerable

While we don’t see prospects for a EUR/USD breakout, the risks in USD/JPY are slightly different and the current excessively loose monetary stance in Japan leaves the yen open to renewed selling and a retest of the high set just before probable intervention by the MoF. Today, nationwide inflation data was released and we saw YoY rates decline broadly as expected. The core CPI YoY rate slowed from 2.6% to 2.2% in April while the core-core rate slowed from 2.9% to 2.4%. The breakdown saw inflation in most sectors decelerate although transport and communications jumped from 2.4% to 2.7%.

The BoJ won’t be surprised by this and it’s unlikely at this stage to alter the trajectory of policy changes going forward. Governor Ueda yesterday spoke ahead of a G7 finance ministers’ meeting in Italy, stating that “there is no change in the overall view of the economy” and emphasised that a soft landing for the US economy was the “key issue for the global economy”. In our view it is the international economic conditions that will be most important for the trajectory of BoJ monetary policy.

In any case, the deceleration in inflation in Japan should soon bottom out with a portion of the utility subsidies ending at the end of this month and the pipeline inflation measures showing a pick-up in inflation starting to emerge in part fuelled by the depreciation of the yen and higher commodity prices.

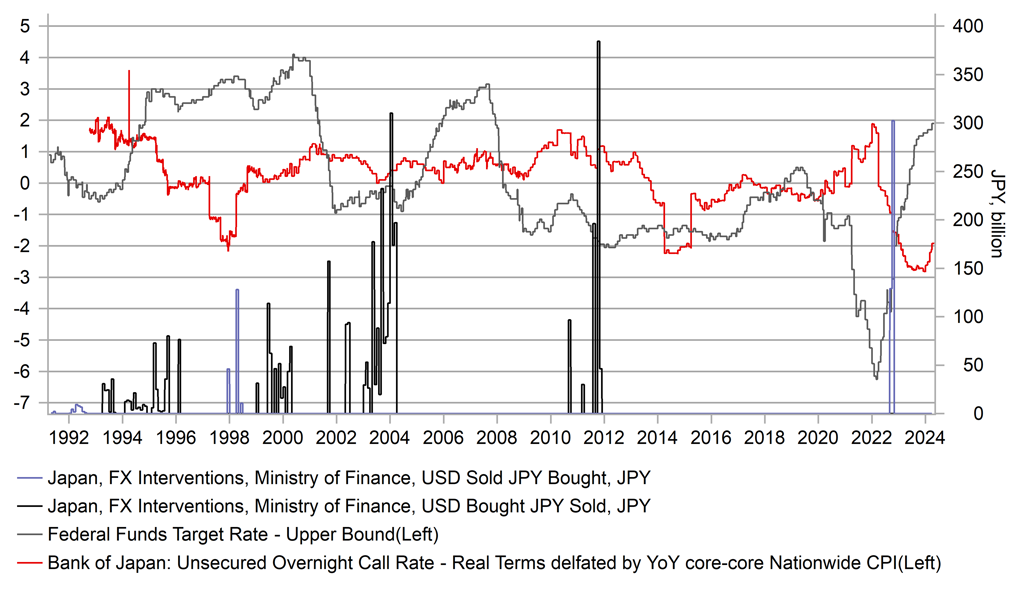

But the BoJ has never been battling against yen moves with the monetary stance so inconsistent with FX intervention. Back in 1998 when the MoF intervened to buy JPY, the BoJ real policy rate was significantly below the US real fed funds rate but that was in part driven by a sales tax lift to inflation. Then when the MoF was selling JPY (most of the time), the BoJ real policy rate was often higher than the real fed funds rate but the divergence now points to the most inconsistent monetary stance in real terms relative to intervention actions. While the Fed cutting rates will be key, the urgency for the BoJ to lift rates is increasing given the move in US yields.

PERIODS OF JPY BUYING & SELLING INTERVENTIONS VERSUS THE BOJ & FED POLICY RATES IN REAL TERMS

Source: Macrobond & Bloomberg

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

08:00 |

ECB's Schnabel Speaks |

-- |

-- |

-- |

!! |

|

SZ |

08:45 |

SNB Chairman Jordan speaks |

-- |

-- |

-- |

!!! |

|

GE |

10:15 |

German Buba’s Nagel Speaks |

-- |

-- |

-- |

!! |

|

US |

13:30 |

Core Durable Goods Orders (MoM) |

Apr |

0.1% |

0.2% |

!! |

|

US |

13:30 |

Durable Goods Orders (MoM) |

Apr |

-0.9% |

2.6% |

!! |

|

US |

13:30 |

Durables Excluding Defense (MoM) |

Apr |

-- |

2.3% |

! |

|

US |

13:30 |

Durables Excluding Transport (MoM) |

-- |

-- |

0.2% |

! |

|

US |

13:30 |

Goods Orders Non Def Ex Air (MoM) |

Apr |

0.1% |

0.2% |

! |

|

CA |

13:30 |

Core Retail Sales (MoM) |

Mar |

0.3% |

-0.3% |

!! |

|

CA |

13:30 |

Retail Sales (MoM) |

Mar |

-0.1% |

-0.1% |

!! |

|

CH |

14:00 |

FDI |

-- |

-- |

-26.10% |

! |

|

US |

14:35 |

Fed Waller Speaks |

-- |

-- |

-- |

!!! |

|

US |

15:00 |

Michigan 1-Year Inflation Expectations |

May |

3.5% |

3.2% |

!! |

|

US |

15:00 |

Michigan 5-Year Inflation Expectations |

May |

3.1% |

3.0% |

!! |

|

US |

15:00 |

Michigan Consumer Expectations |

May |

66.5 |

76.0 |

!! |

|

US |

15:00 |

Michigan Consumer Sentiment |

May |

67.4 |

77.2 |

!! |

|

US |

15:00 |

Michigan Current Conditions |

May |

68.8 |

79.0 |

! |

|

US |

15:30 |

Atlanta Fed GDPNow |

Q2 |

3.6% |

3.6% |

!! |

Source: Bloomberg