Tech market sell-off reinforces liquidation of JPY-funded carry trades

JPY: US tech stock sell-off reinforces liquidation of short JPY positions

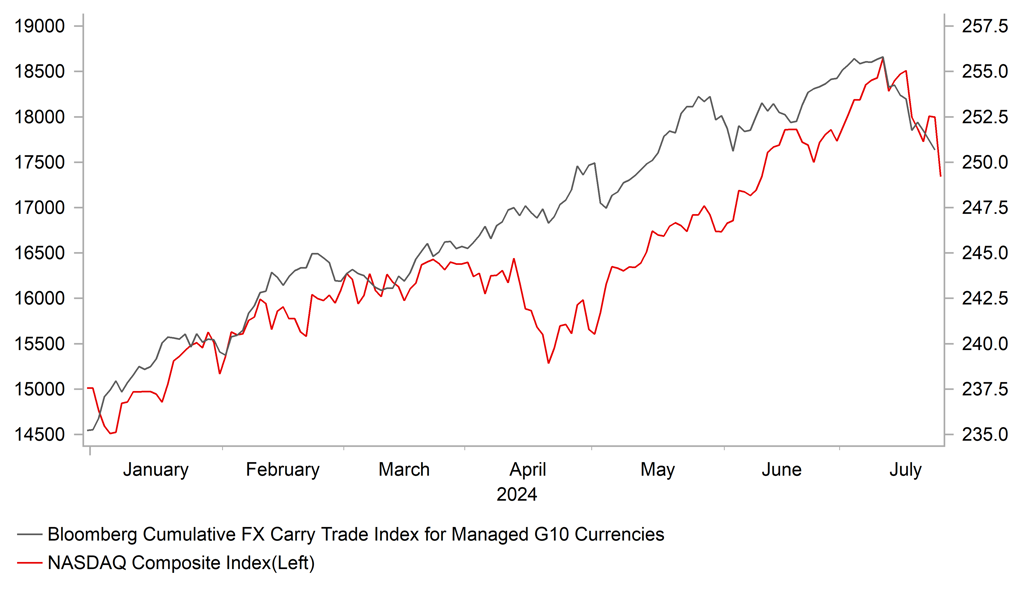

The yen has continued to strengthen sharply during the Asian trading session resulting in USD/JPY falling to an intra-day low of 152.23. The pair has now fallen by almost 10 big figures from the high recorded on 3rd July. The next important support level is provided by the 200-day moving which comes in at around 151.50. The 200-day moving average was last broken at the end of last year/start of this year but only temporarily before USD/JPY then rose to fresh highs. The yen’s gains have accelerated this week amidst more risk-off trading conditions that have triggered a further liquidation of elevated yen funded carry trade positions. The other traditional safe haven currency of the Swiss franc has also outperformed alongside the yen resulting EUR/CHF falling back towards the 0.9500-level.The deterioration investor risk sentiment was again evident overnight with the US equity markets suffering their largest one day loss since 2022. It was driven by a correction lower for US tech stocks. The Nasdaq 100 index fell by a further -3.7% overnight extending losses since the 11th July high to just over 7%. Tesla dropped even more sharply by 12% yesterday after reporting another quarter of disappointing profit and postponing a highly anticipated unveiling of autonomous taxis. The broad-based reversal of crowded trades is spilling over into the FX market over the summer period.

The other main development overnight was the surprise decision from the PBoC to lower rates again for the second time this week. The PBoC unexpectedly lowered the one-year medium-term lending facility by 20bps to 2.30%. It was the first reduction in almost a year. It quickly follows the 10bps reduction in the 7-day reverse repo rate at the start of this week. In addition, the PBoC provided CNY200 billion of MLF today which was the biggest injection of funds since January. According to Bloomberg, banks have had little appetite for the MLF funds in recent months as a decline in market rates meant it became cheaper for them to borrow from each other than from the PBoC via the program. A bigger cut to the MLF rate helps bring it closer to market borrowing costs. Overall, the policy action highlights that domestic policymakers have become more concerned over slowing growth momentum in China and are now taking action to meet their GDP target for this year of around 5%. The renminbi has initially strengthened against the US dollar rather than weakened following the reduction in interest rates. A number of factors could help explain the price action: i) could reflect more investor optimism that decisive policy action will be taken to boost growth, ii) it could be driven state support to sell US dollars, iii) it could be due to spill-over from the unwind of carry trades and/or iv) it is driven more by the drop in US yields which have fallen by more those in China. It does not change our view though that the current combination of disappointing growth momentum, lower rates and the increased threat of higher tariffs being imposed on China is an unfavourable set up for the renminbi.

REVERSAL UNDERWAY FOR CROWDED TRADES

Source: Bloomberg, Macrobond & MUFG GMR

USD/CAD: Risk-off trading & dovish BoC policy update lift USD/CAD

More risk-off trading has continued to weigh on the high beta G10 commodity currencies. The Norwegian krone has weakened by -3.2% against the USD so far this month, the New Zealand dollar by -2.7%, the Australian dollar by -1.3% and the Canadian dollar by -0.9%. It has helped to lift USD/CAD closer to the year to date high of 1.3846 from 16th April. At the same time, the Canadian dollar was undermined by the BoC’s decision to deliver back to back rate cuts yesterday when they lowered their policy rate by a further 0.25 point to 4.50%. While the rate cut was almost fully priced in ahead of the meeting, the accompanying policy guidance also left the door open to further rate cuts weighing on the Canadian dollar. The BoC indicated that it is now more focused on downside risks with more excess supply in the economy. The case for lower rates was supported by the downgrade to the BoC’s core inflation forecasts that were lowered by 0.1 point for 2025 and 2026. The BoC looked through the recent stronger inflation prints and continued to describe broad inflationary pressures as easing. More specifically the BoC noted that their “preferred measures of core inflation have been below 3% for several months and the breadth of price increases across components of the CPI is now near its historical norm”. The BoC expects broad price pressures to continue to ease and inflation to move closer to their 2% target. In these circumstances, we expect the BoC to keep lowering their policy rate closer to their estimate of the neutral range between 2.25% and 3.25% in the year ahead.

The BoC does not appear concerned yet about continuing to lower rates ahead of the Fed which is placing upward pressure on USD/CAD. However, room for policy divergence to widen further between the BoC and Fed in the near-term is becoming more limited. We are becoming more confident that the Fed will soon join the BoC in cutting rates at the September FOMC meeting. Former New York Fed President William Dudley attracted some market attention yesterday when he called on the Fed to begin cutting rates as soon as this month in response to the rising unemployment rate and recent softer inflation prints although he doesn’t think they will act so soon.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

GE |

09:00 |

German Ifo Business Climate Index |

Jul |

88.9 |

88.6 |

!! |

|

EC |

09:00 |

M3 Money Supply (YoY) |

Jun |

1.9% |

1.6% |

! |

|

EC |

11:00 |

Eurogroup Meetings |

-- |

-- |

-- |

!! |

|

US |

13:30 |

Durable Goods Orders (MoM) |

Jun |

0.3% |

0.1% |

!! |

|

US |

13:30 |

GDP (QoQ) |

Q2 |

2.0% |

1.4% |

!!! |

|

US |

13:30 |

Initial Jobless Claims |

-- |

237K |

243K |

!!! |

|

US |

21:30 |

Fed's Balance Sheet |

-- |

-- |

7,208B |

!! |

Source: Bloomberg