USD remains close to year-to-date high ahead of latest US inflation update

USD: Fed policy reaction function & AI stock performance in focus

The major foreign exchange rates have remained relatively stable overnight with the US dollar continuing to trade close to year-to-day highs. US Treasury Secretary Scott Bessent was asked yesterday about the Fed’s latest hawkish policy update under new Chair Kevin Warsh. He told CNBC that “he came out tough, talking about the inflation”, and indicated that he was confident that Kevin Warsh “will take the best path to satisfy both the inflation mandate and growth mandate”. When asked whether he’s discussed with President Trump that it’s not the right time to cut rates, he stated that President Trump “has said both in public and privately that he has every confidence in Kevin Warsh”. However, he is confident that that the Us economy will accelerate “on a non-inflationary basis for the rest of the year”. “Now that we are, I believe, on the other side of this conflict, gas prices will come down, inflation will come back to target”. The price of oil has continued to fall this week, and has almost fully given back all of the gains since the conflict began in February. It is one of the reasons why we still don’t expect the Fed to back up tough talk on inflation by hiking rates hikes this year. Admittedly, the lack of clarity over the Fed’s new policy reaction function under new Chair Warsh who does not want to provide forward guidance gives us less confidence over projecting the outlook for Fed policy at the current juncture. In contrast, the US rate market has taken the opposite view that the Fed will back up tough talk on inflation by hiking rates this year. If the Fed is serious about restoring price stability, a significant tightening of monetary policy will be required so it makes sense that more hikes have been priced in recently encouraging a stronger US dollar. We expect the US dollar to continue to trade at stronger levels until it is either challenged by incoming economic data showing slowing inflation and/or any indications from the Fed that they will not follow through with rate hikes. The release today of the latest US PCE deflator report for May will provide an update on inflation pressures. Please see the below topic for more details over how the FX market is likely to react to the report.

The other main development overnight was the release of strong earnings update from Micron Technology. The largest US maker of computer memory chips announced that revenue in the fiscal fourth quarter will be approximately USD50 billion coming in well above analysts’ estimate of USD43.2 billion. Micron also announced it has secured 16 strategic customer agreement which average three years in length. Micron and its peers in the memory space such as Samsung Electronics and SK Hynix have become major beneficiaries of the AI infrastructure build out. The strong earnings update from Micron has helped South Korean stocks to rebound overnight after the heavy sell-off at the start of this week and will provide a boost for investor sentiment in AI/tech stocks more broadly. The Kospi equity index has risen by around 6% overnight and has now almost fully reversed the outsized sell-off on Tuesday. However, spillovers into the foreign exchange market this week have been muted.

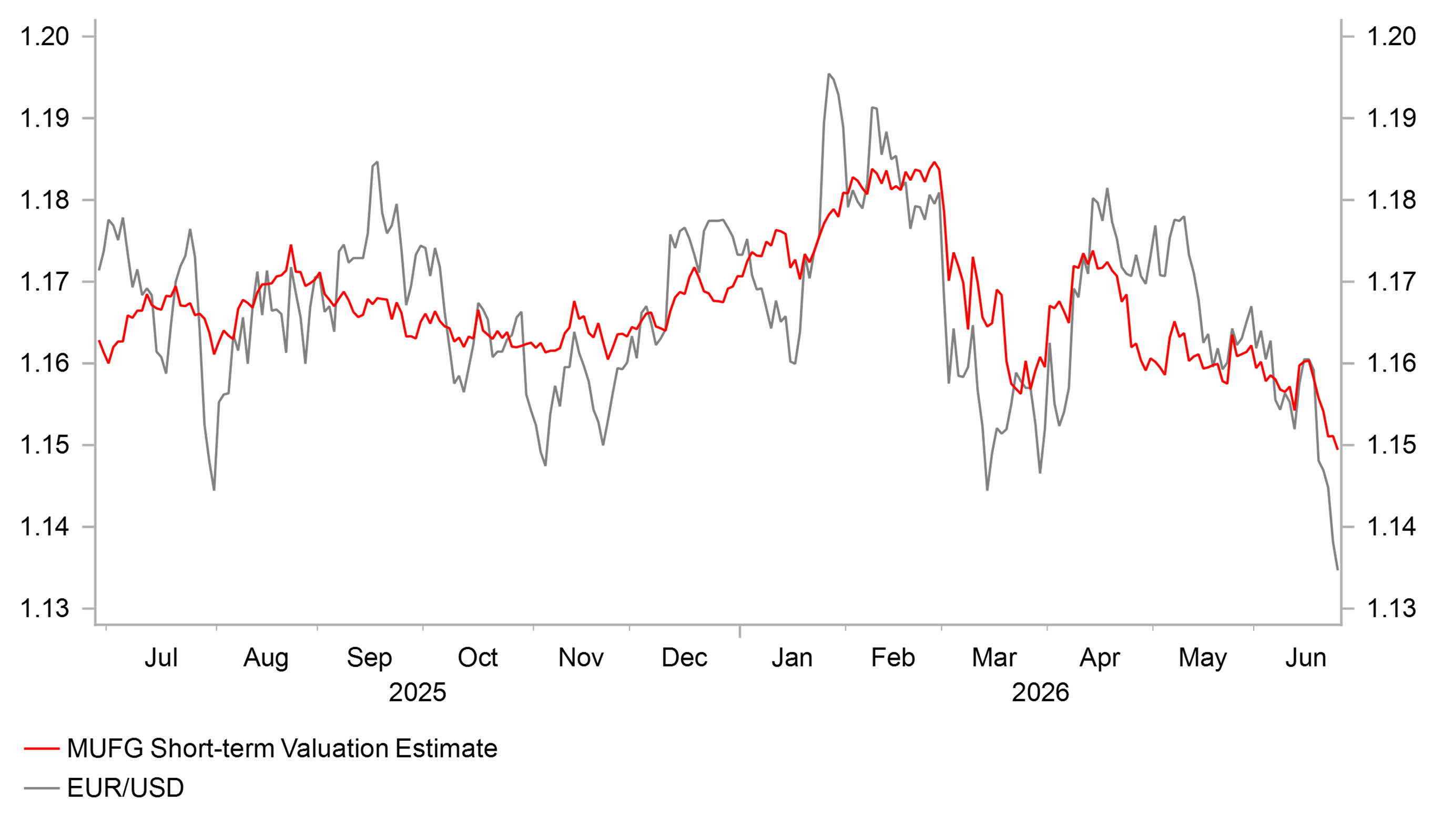

IS USD ANTICIPATING A BIGGER FED POLICY SHIFT OR OVERSHOOTING?

Source: Bloomberg, Macrobond & MUFG Research

USD: How FX reacts to PCE surprises

FX markets are historically sensitive to PCE releases, and this sensitivity is amplified in the current environment where the Fed remains firmly focused on inflation persistence. The latest Summary of Economic Projections (SEP) reinforced both a higher inflation trajectory and a more hawkish policy path, underscoring the importance of incoming data surprises. As the Fed’s preferred inflation gauge, the core PCE is a key driver of front-end US yields and the US dollar.

To examine this relationship, we conduct an event-driven price action analysis, comparing actual (unrevised) PCE releases against Bloomberg consensus expectations for releases after January 2022 to present. While several components of the PCE release are effectively known ahead of time, there are still meaningful sources of uncertainty. The core PCE MoM is likely to print above core CPI MoM (+0.21%), with the Bloomberg consensus of +0.35% appearing well-anchored to known features.

However, residual uncertainty persists due to BEA-specific methodological adjustments, including seasonal factors, FISIM imputation, and healthcare deflators. These are not directly observable ahead of the release and have historically driven surprises of ±5–10bp relative to pre-release estimates.

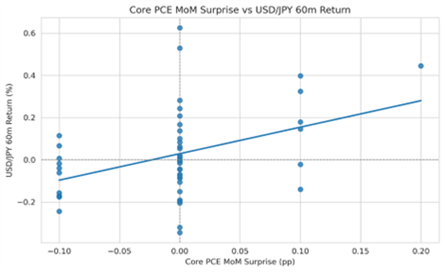

For USD/JPY, the directional response is both intuitive and statistically consistent. Downside surprises lead to USD/JPY declines, reflecting softer inflation and reduced expectations for Fed tightening, while upside surprises drive USD/JPY higher as front-end rates reprice more hawkishly. Our analysis identifies this reaction is built gradually, with the clearest signal emerging within the first 60 minutes post-release, suggesting decisive repricing process. Running the same framework on EUR/USD identifies a consistent directional pattern, confirming that the observed moves reflect a broad USD macro repricing. Finally, we note that the FX response function is front-loaded. While intraday horizons (15–60 minutes) exhibit clear and systematic patterns, the relationship becomes increasingly noisy later in the day and the following day as broader macro drivers and positioning dominate price action.

USD/JPY PERFORMANCE AFTER US CORE PCE DEFLATOR RELEASES

Source: Bloomberg, Macrobond & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EC | 09:00 | ECB Publishes Economic Bulletin | !! | |||

UK | 11:00 | CBI Total Dist. Reported Sales | Jun | -- | - 35.0 | !! |

EC | 11:00 | ECB's Lane Speaks | !! | |||

US | 13:30 | Personal Spending | May | 0.6% | 0.5% | !! |

US | 13:30 | Core PCE Price Index MoM | May | 0.3% | 0.2% | !!! |

US | 13:30 | GDP Annualized QoQ | 1Q T | 1.6% | 1.6% | !!! |

US | 13:30 | Initial Jobless Claims | 225k | 226k | !! | |

US | 13:30 | Durable Goods Orders | May P | - 5.0% | 8.0% | !! |

US | 16:00 | Kansas City Fed Manf. Activity | Jun | 6.0 | 8.0 | !! |

US | 20:40 | Fed's Williams Gives Keynote Remarks | !!! |

Source: Bloomberg & Investing.com