Non-dollar factors driving FX with FOMC minutes as expected

USD: Fed minutes signal gradual rate cuts approach

The US dollar is within narrowing trading range across much of G10 with the exception of JPY (see below) and NZD, which have both led the way in terms of performance. The RBNZ announced a 50bp rate cut today but there had been some modest pricing indicating a risk of an even larger cut and with the RBNZ sticking to 50bps, NZD has bounced higher. The 2-year NZ government bond is 5bps higher today. The fact that RBNZ Governor Orr has signalled the prospect of another 50bp rate cut in February has failed to undermine the currency given this too was nearly fully priced. Around 95bps of cuts was priced in the OIS market yesterday. The forward guidance on rates by the RBNZ today also wasn’t as aggressive as some market participants were expecting with the average OCR rate falling to 3.83% by mid-year 2025.

But the RBNZ has consistently under-estimated the speed in which inflation returns to target and has therefore under-estimated the scope in which it can ease its monetary stance. That risk remains and hence investors could quickly turn sceptical of this RBNZ guidance leaving NZD vulnerable to renewed depreciation. The broader global risks related to Trump and trade tariffs also point to downside risks ahead so we are not convinced that this rebound in NZD will be sustained.

While the rest of G10 (bar JPY) has seen modest moves, the minutes from the FOMC certainly helped in the NZD/USD move higher. The markets appear to have been braced for the risk of a more hawkish minutes given the fact that front-end yields in the US have declined since the release of the minutes. The 2-year UST bond yield has declined by 7bps from the release of the minutes. The key message from the minutes – that the FOMC can continue to gradually lower the fed funds toward a neutral level if economic conditions remain broadly as they are and inflation continues to ease slowly – has helped strengthen expectations that the FOMC will cut rates again at the December FOMC meeting.

Despite some signs of a softening dollar there are also plenty of reasons to believe further dollar strength still lies ahead. President-elect Trump announced yesterday that Jamieson Greer as the US Trade Representative. Greer is a protégé of Robert LIghthizer and is a strong supporter of trade tariffs, as you would expect. Lighthizer no doubt will likely play a less formal advisory role and with Greer and Howard Lutnick we can safely assume a pro-trade tariff team will be in place to likely commence Trump’s presidency with executive orders that puts in place tariffs very quickly. We continue to expect Trump’s approach to trade tariffs to be very different to his first term in office with a more aggressive stance evident, possibly from day one.

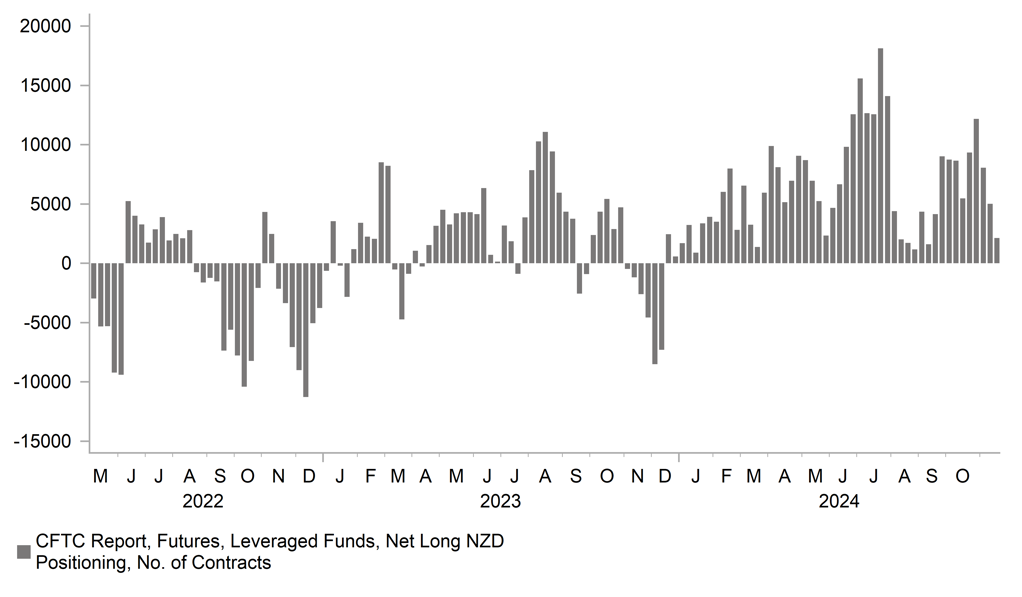

LONG NZD POSITIONING BY LEVERAGED FUNDS HAS BEEN PARED BACK

Source: Bloomberg, Macrobond & MUFG GMR

JPY: BoJ rate hike expectations providing support

The yen is creeping up the G10 performance table is now the top performing G10 currency in the month of November highlighting the limited impact the Trump optimism is having on weakening the yen further. The US dollar strengthened across G10 yesterday but the yen still managed to outperform the dollar with some notable moves lower in yen crosses. The moves are certainly reminiscent of your typical risk-off type trading you’d expect to see which is consistent with the general decline in global equities yesterday (outside the US) as fears of trade tariffs increased. Still, there was no decline in front-end US yields suggesting there was more to the move than simply risk-off.

It is worth mentioning though that the better performance now for the yen may also merely reflect the bigger sell-off ahead of the election. The ‘Trump trade’ very much came back into market focus in October and in that month, the yen was the second worst performing G10 currency, weakening by 5.5%. The euro was the third best performing, weakening by 2.2% versus the dollar. Now in November, the euro is the worst performing. There is also the added risk of intervention in Japan and there has been clear comments from the MoF over the threat of intervention which seems very plausible at levels over 155.00 on the approach of the key 160-level around which the MoF intervened before.

But the economic backdrop is also improving in Japan and that is fuelling expectations of a rate hike in December by the BoJ. We originally expected a December rate hike but then moved the timing to January. However, if market pricing continues to drift in the direction of a hike in December, the BoJ may well deliver. The OIS market now implies a 65% probability of a 25bp hike on 19th December, the highest probability since before the market turmoil in July/Aug that then killed expectations of more BoJ hikes this year. The quick agreement by the LDP-led minority government with the DPP on a fiscal stimulus package has reinforced expectations of a rate hike.

The PPI services data was also released yesterday and may have helped reinforce yen demand given it also prompted increased speculation of a December rate hike. In a newly produced index that the BoJ first published in June (see chart above) PPI services amongst companies with a high labour cost ratio saw an acceleration to 3.3% YoY which was the highest level (when sales tax increase periods are excluded) since April 1992. This is the type of data that the BoJ can cite of the impact of higher wages on inflation – that virtuous circle between wages and inflation – basically being confirmed. PM Ishiba yesterday confirmed that he is continuing to communicate with businesses in Japan on the importance of increasing wages.

We would be reluctant to suggest the yen can continue to strengthen from here versus the dollar. Tariffs on Japan imports to the US remains a risk and higher US yields will limit USD/JPY downside moves. But the JPY price action and the increased prospects of a December rate hike will ensure the yen performs better relative to non-dollar G10.

JAPAN SERVICES PPI YOY – SERVICES WITH HIGH LABOUR COST RATIO

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

SZ |

09:00 |

ZEW Expectations |

Nov |

-- |

-7.7 |

! |

|

GE |

09:30 |

GfK German Consumer Climate |

Dec |

-18.8 |

-18.3 |

!! |

|

US |

13:30 |

Core PCE Prices |

Q3 |

2.20% |

2.80% |

!!! |

|

US |

13:30 |

Durable Goods Orders (MoM) |

Oct |

-0.8% |

0.0% |

!! |

|

US |

13:30 |

Goods Orders Non Def Ex Air (MoM) |

Oct |

0.5% |

0.2% |

!! |

|

US |

13:30 |

GDP (QoQ) |

Q3 |

2.8% |

3.0% |

!!! |

|

US |

13:30 |

GDP Price Index (QoQ) |

Q3 |

1.8% |

2.5% |

!! |

|

US |

13:30 |

Goods Trade Balance |

Oct |

-101.60B |

-108.23B |

! |

|

US |

13:30 |

Initial Jobless Claims |

-- |

220K |

213K |

!!! |

|

US |

13:30 |

Personal Income (MoM) |

Oct |

0.3% |

0.3% |

! |

|

US |

13:30 |

Personal Spending (MoM) |

Oct |

0.4% |

0.5% |

!! |

|

US |

14:45 |

Chicago PMI |

-- |

44.9 |

41.6 |

!! |

|

US |

15:00 |

Core PCE Price Index (MoM) |

Oct |

0.3% |

0.3% |

!!! |

|

US |

15:00 |

Core PCE Price Index (YoY) |

Oct |

-- |

2.7% |

!!! |

|

US |

15:00 |

PCE Price index (YoY) |

Oct |

-- |

2.1% |

!! |

|

US |

15:00 |

PCE price index (MoM) |

Oct |

0.2% |

0.2% |

!! |

|

US |

15:00 |

Pending Home Sales (MoM) |

Oct |

-2.1% |

7.4% |

! |

|

US |

15:00 |

Real Personal Consumption (MoM) |

Oct |

-- |

0.4% |

!! |

Source: Bloomberg