Is France political risk set to fuel renewed volatility?

EUR: Potential for downside move remains

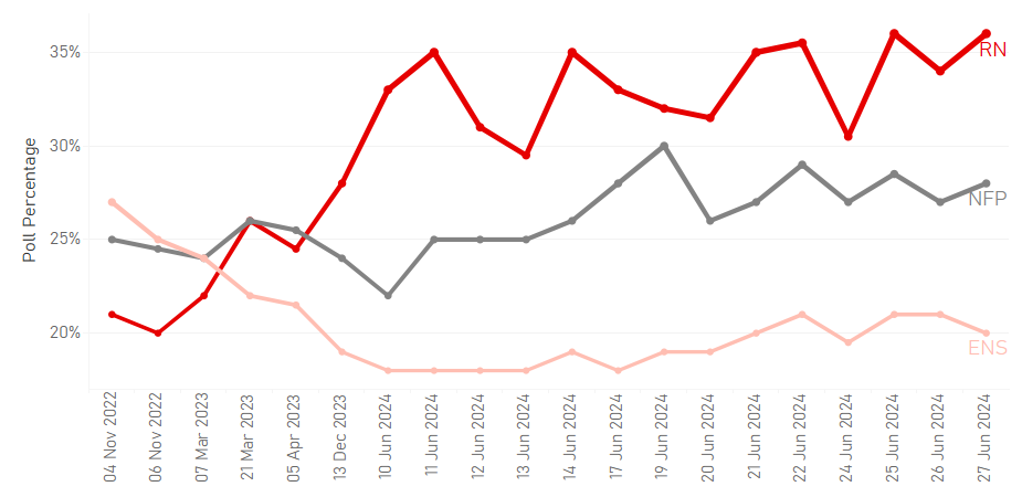

After initially dropping by two big figures in the six trading days following the announcement of snap elections in France, EUR/USD has stabilised since around the 1.0700-level but next week could be a week of renewed volatility depending on the result of the first round of elections on Sunday. We initially estimated around a 1.0% risk premium was possibly priced into EUR now and based on short-term price action against variables like spreads, this remains a reasonable estimate. The first round of the election on Sunday will certainly give us a sense of true support for the right and left parties compared to the polls we have gauged support from so far. For a candidate to win a constituency (577 seats) he or she has to win an outright majority that is also greater than 25% of all eligible voters. For example, a candidate that wins 52% of the vote but because of a low turnout only wins 24% of the total eligible to vote would have to run in the second round. First round wins are therefore rare – there were just five in 2022. Eligibility to go to the second round is to achieve 12.5% of all eligible voters so if turnout is say 48% (first round turnout in 2022) then the vote threshold of actual votes cast would be a bit over the 25% mark (over double the 12.5% total eligible voter threshold). In past elections, RN has had difficulty getting a win in the second round because centrist parties have been able to align to work against the RN. This time that is likely be more difficult with a large number of constituencies in the second round offering an choice between RN and the far-left alliance (New Popular Front).

So on Monday we will know exactly how squeezed out the centrists candidates were in round one and the greater that squeeze is the greater the chance of an outright majority in round two for RN or perhaps the New Popular Front.

Based on the polling we believe there are perhaps four plausible scenarios : 1) RN wins the most seats but falls short of an outright majority (45%); 2) RN wins an outright majority (25%); 3) NPF wins the largest number of seats but falls short of an outright majority (20%); 4) there is no clear winner and we have complete paralysis with no obvious root to a working government (10%).

These are initial scenarios evident in the immediate aftermath of the second round election on 7th July. In other words, scenario 4) could eventually shift and a government is formed but initially it is not obvious. We have also raised the probability of an RN outright majority based on the interviews from Marine Le Pen and Jordan Bardella that certainly point to a willingness of RN to be pragmatic and possibly park some of their initial more contentious policies for a period of time. The tone from RN certainly suggests the flippant spending and large fiscal deficits touted in 2022 are unlikely which would potentially contain the market fallout in scenario 2). Based on RN communications it seems the worst scenario would be scenario 3) and certainly from a bond market perspective this would fuel the widest OAT/Bund spread move. Scenario 4) is not particularly positive either but the market move might be contained on the hope of an eventual path to a governing coalition can be found.

For next week, the larger the number of consistencies that has resulted in the failure of centrists candidates making the final ballot, the greater the negative reaction might be. A surprise outperformance for NPF would also likely fuel greater OAT and EUR selling. Obviously if RN and NPF were to do worse than expected at the expense of Macron’s Ensemble or Les Republicains, we will likely see some spread narrowing on Monday and some modest EUR gains. With the EUR risk premium relatively modest strong RN & NPF performances will likely see EUR/USD close to the 1.0500-level.

OPINION POLLING FOR TOP THREE FRENCH POLITICAL ALLIANCES

Source: Wikipedia; various online polling data; as of 27th June 2024

USD: PCE inflation data ahead of a busy week

EUR/USD bounced yesterday with the data releases from the US again pointing to evidence that the labour market might not be as strong as implied by the non-farm payroll data. The continued claims reading increased for the eighth consecutive week and gains in the last three weeks have been more notable with the level now the highest since December 2021. The 2-year UST note yield dropped by 5bps with the weaker consumer spending data in the revised Q1 GDP report also adding downward pressure to yields.

But the dollar has recovered after a moderate sell-off in response to the data and drop in yields with the US presidential debate providing some additional support after a poor performance by President Biden has increased the probability further of a Trump victory in November. The topic of China was raised with Trump incorrectly claiming the US trade deficit with China was at a record and that tariffs would “force them to pay us a lot of money”.

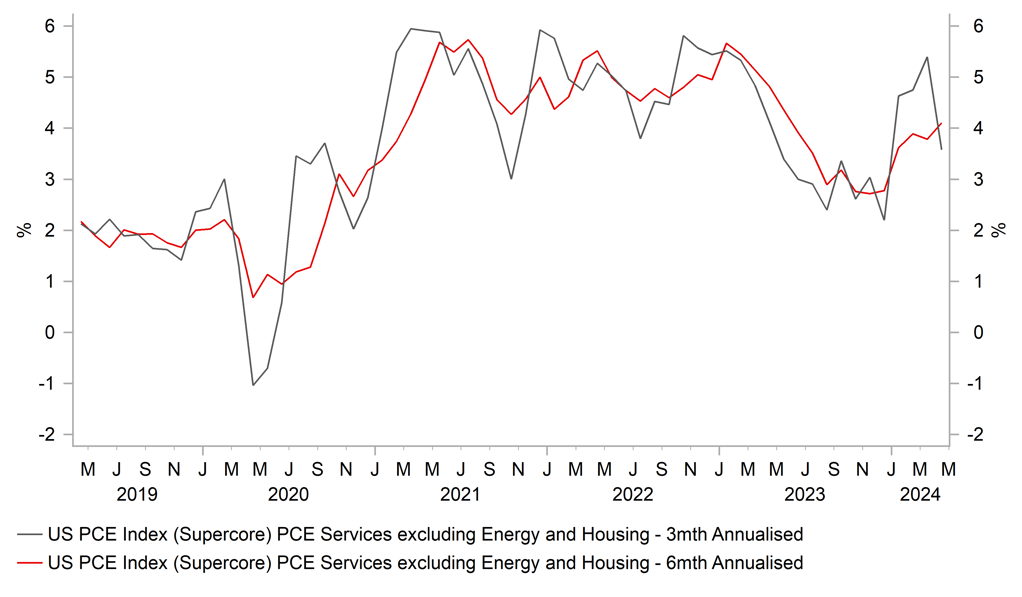

Today is month-end and quarter-end and hence flows can be unpredictable. No doubt with the French election at the weekend, there is unlikely to be much impetus to buy EUR/USD. The PCE inflation data will be the key release today ahead of the more important series of data next week. We already know some of the components for the PCE inflation (in the PPI data) and hence it unusual for the PCE inflation to deviate notably from the consensus (Core PCE 0.1%). Any dollar sell-off at this stage with the election uncertainty would at least need the PCE ‘supercore’ MoM reading to reveal a further slowdown after the April reading of 0.27%, which was down from 0.42% in March.

US ‘SUPERCORE’ PCE INFLATION SET TO DECELERATE FURTHER

Source: Bloomberg & Macrobond

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

GE |

08:55 |

German Unemployment Change |

Jun |

14K |

25K |

!! |

|

GE |

08:55 |

German Unemployment Rate |

Jun |

5.9% |

5.9% |

!! |

|

IT |

09:00 |

Italian Industrial Sales (MoM) |

Apr |

-- |

-2.90% |

! |

|

IT |

10:00 |

Italian HICP (MoM) |

Jun |

0.2% |

0.2% |

! |

|

IT |

10:00 |

Italian HICP (YoY) |

Jun |

0.9% |

0.8% |

! |

|

US |

11:40 |

FOMC Member Barkin Speaks |

-- |

-- |

-- |

!! |

|

US |

13:30 |

Core PCE Price Index (YoY) |

May |

2.6% |

2.8% |

!!!! |

|

US |

13:30 |

Core PCE Price Index (MoM) |

May |

0.1% |

0.2% |

!!!!! |

|

US |

13:30 |

PCE Price index (YoY) |

May |

2.6% |

2.7% |

!! |

|

US |

13:30 |

PCE price index (MoM) |

May |

0.0% |

0.3% |

!!! |

|

US |

13:30 |

Personal Income (MoM) |

May |

0.4% |

0.3% |

! |

|

US |

13:30 |

Personal Spending (MoM) |

May |

0.3% |

0.2% |

!! |

|

CA |

13:30 |

GDP (MoM) |

Apr |

0.3% |

0.0% |

!! |

|

US |

14:45 |

Chicago PMI |

Jun |

39.7 |

35.4 |

!! |

|

US |

15:00 |

Michigan 1-Year Inflation Expectations |

Jun |

3.3% |

3.3% |

!!! |

|

US |

15:00 |

Michigan 5-Year Inflation Expectations |

Jun |

3.1% |

3.0% |

!!! |

|

US |

15:00 |

Michigan Consumer Expectations |

Jun |

67.6 |

68.8 |

!! |

|

US |

15:00 |

Michigan Consumer Sentiment |

Jun |

65.6 |

69.1 |

!! |

|

US |

15:00 |

Michigan Current Conditions |

Jun |

62.5 |

69.6 |

! |

|

US |

17:00 |

FOMC Member Bowman Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg