Risk-off returns with JPY outperforming

JPY: High inflation & risk-off will help yen

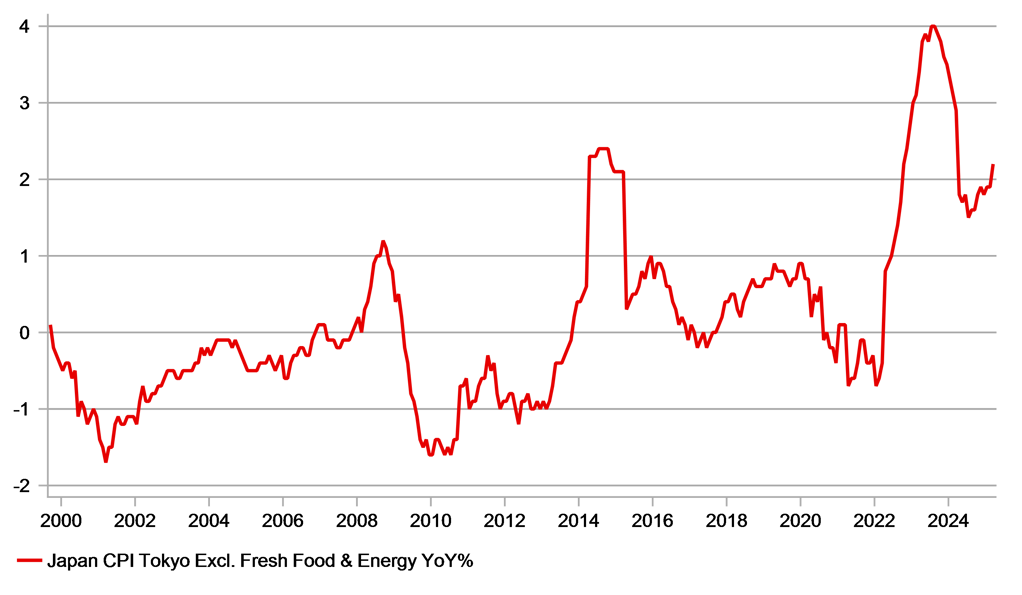

Foreign exchange moves are reasonably contained so far this morning but there are signs of increased risk aversion amongst global investors following the auto tariff announcements by President Trump on Wednesday and ahead of the reciprocal tariff announcements next week. The Topix index declined by just over 2% today and auto tariff concerns were more evident today than yesterday. Toyota Corp. fell 4.5% today after a drop of just 2% yesterday. Today’s drop was the largest since September last year. The yen is the top performing G10 currency so far today although the gain is a modest 0.4% with US yields down, but only modestly. The yen could be helped further from here though given the inflation data released today reinforces the prospect of the BoJ hiking rates further, in our view at the July BoJ meeting. A hike at that meeting is currently priced at about 80%. Tokyo core annual CPI jumped from 2.2% to 2.4% while the core-core rate jumped from 1.9% to 2.2% - both readings were expected to remain unchanged. Overall food prices slowed but remain elevated and while fresh food prices slowed, non-fresh food prices jumped from 5.0% to 5.6%, fuelled by a further gain in rice prices. With food prices elevated, the cost of living crisis remains a political issue that will lead to increased government opposition to a further weakness of the yen. Services inflation also picked up while crucially rental inflation is picking up notably and tends to be more sticky than other components which will strengthen the BoJ’s belief that inflation is becoming sustainable. Rents increased 1.1% on an annual basis, the biggest increase since October 1994, no doubt helped by rising wage growth.

The impact on lifting the yen from the strong inflation data was likely curtailed by the release of the initial summary of the BoJ meeting that took place on 18th-19th March. The details showed some emerging concerns that could result in a more cautious approach to further rate hikes. Nonetheless there were other comments that suggested there may be a need for assertive action even in circumstances of rising uncertainties. Certainly, inflation data like today’s and the recent ‘shunto’ wage estimate points to the need for assertive action. We see scope for yen selling at levels over 150.00 as more limited especially given data that indicates continued building inflation pressures.

TOKYO CORE-CORE CPI HAS REACCELERATED BACK ABOVE THE BOJ’S 2.0% GOAL WITH FOOD AND RENTAL INFLATION FIRM

Source: Bloomberg, Macrobond & MUFG GMR

CAD: Optimism over tariff impact best reflected in CAD

While there are signs of increased risk aversion today, the overall financial market reaction to the 25% global tariff on autos and auto parts continues to be relatively muted with most G10 currencies still stronger against the dollar since Trump’s announcement. The yen and the Canadian dollar were the two worst performing G10 currencies yesterday with both key auto producers into the US market. And as highlighted above, there is also a growing view that the actions from Trump this week and again on 2nd April, may curtail the appetite within the BoJ for additional rate hikes.

For the Canadian dollar, while it underperformed yesterday, the performance continues to be resilient that must surely be questioned. Can the Canadian dollar avoid a sharper depreciation given the elevated risks to the Canadian economy from increased trade tariffs from the country where exports account for around 80% of total exports? It appears there is still optimism that Trump will prove constrained given the interlinkages between the two economies. Yesterday, media in Canada reported that Ontario Premier Doug Ford had held a call with Commerce Secretary Howard Lutnick that would ultimately lead to the US watering down tariffs against Canada.

That optimism is also evident by the OIS market pricing on rate cuts from the Bank of Canada through the remainder of the year. The market expects 42bps of cuts compared to 63bps of cuts by the Fed. Of course the BoC has already cut by more than the Fed explaining this divergence but nonetheless, if tariffs do remain in place for longer the economic impact will require more cuts than implied by market pricing.

The Bank of Canada in January published its own economic impact analysis based on a scenario of a 25% increase in tariffs on all imported Canadian goods into the US and a retaliation by Canada doing the same for all US imported goods to Canada. The BoC estimated a 2.5ppt drop in GDP in year one and a 1.5ppt drop in year relative to the baseline of no tariffs. Inflation would be higher given the scale of retaliation but not initially due to excess supply and falling commodity prices and the BoC has stated that its focus would be more on the GDP hit than the medium term inflation risks and hence implies more active rate cuts than what is priced now.

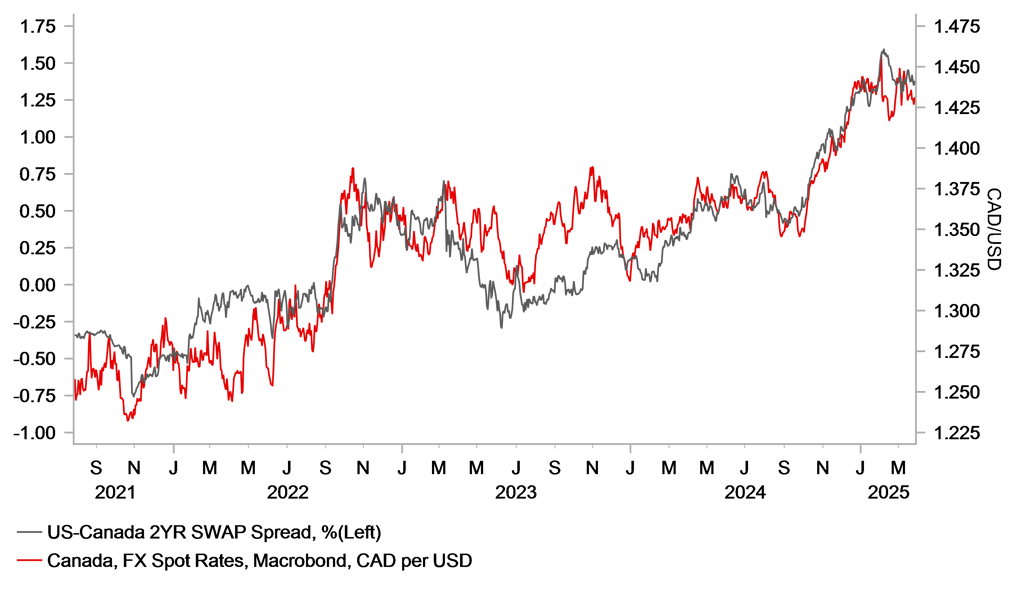

The two-year US-CA swap spread co-movement with USD/CAD is very tight and if the market optimism over trade tariffs fade we can expect a renewed widening of the spread that should see USD/CAD adjust higher back toward the 1.5000-level. Yesterday there were reports that for the first time since being sworn in as Prime Minister, Mark Carney had spoken to President Trump. However, this was quickly denied. How this relationship evolves would be important in determining risks of a trade war escalation. An election takes place in Canada on 28th April and the Liberal Party’s support in the polls has surged on Carney’s tougher rhetoric that suggests Carney will be wary of looking weak ahead of the election.

USD/CAD IS CLOSELY TRACKING MOVES IN THE US-CA 2-YEAR SPREAD WHICH ASSUMES MORE MODEST BOC EASING THIS YEAR THAN FED

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

08:30 |

ECB's De Guindos Speaks |

-- |

-- |

-- |

!! |

|

IT |

09:00 |

Italian Business Confidence |

Mar |

87.5 |

87.0 |

! |

|

IT |

09:00 |

Italian Consumer Confidence |

Mar |

-- |

98.8 |

! |

|

IT |

10:00 |

Italian Industrial Sales (MoM) |

Jan |

-- |

-2.70% |

! |

|

EC |

10:00 |

Business and Consumer Survey |

Mar |

97.0 |

96.3 |

! |

|

EC |

10:00 |

Consumer Confidence |

Mar |

-14.5 |

-14.5 |

! |

|

EC |

10:00 |

Services Sentiment |

Mar |

6.7 |

6.2 |

! |

|

EC |

10:00 |

Industrial Sentiment |

Mar |

-10.5 |

-11.4 |

! |

|

US |

12:30 |

PCE Price index (YoY) |

Feb |

2.5% |

2.5% |

!!! |

|

US |

12:30 |

PCE price index (MoM) |

Feb |

0.3% |

0.3% |

!!! |

|

US |

12:30 |

Core PCE Price Index (MoM) |

Feb |

0.3% |

0.3% |

!!!! |

|

US |

12:30 |

Core PCE Price Index (YoY) |

Feb |

2.7% |

2.6% |

!!!! |

|

US |

12:30 |

Personal Income (MoM) |

Feb |

0.4% |

0.9% |

! |

|

US |

12:30 |

Personal Spending (MoM) |

Feb |

0.5% |

-0.2% |

!! |

|

CA |

12:30 |

GDP (MoM) |

Jan |

0.2% |

0.2% |

!! |

|

US |

14:00 |

Michigan 1-Yr Inflation Expectations |

Mar |

4.9% |

4.9% |

!! |

|

US |

14:00 |

Michigan 5-Yr Inflation Expectations |

Mar |

3.9% |

3.9% |

!! |

|

US |

14:00 |

Michigan Consumer Expectations |

Mar |

54.2 |

54.2 |

!! |

|

US |

14:00 |

Michigan Consumer Sentiment |

Mar |

57.9 |

57.9 |

!! |

|

US |

14:00 |

Michigan Current Conditions |

Mar |

63.5 |

63.5 |

! |

|

US |

19:45 |

FOMC Member Bostic Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg