USD upside risks as Middle East risks pick up again

USD: Concerns grow over renewed military conflict

The growing confidence amongst investors that a peace deal would soon be reached has taken a hit but the reversal in the financial markets has been very limited so far. After Brent crude oil prices dropped by over 15% from the high at the beginning of last week, the bounce today so far has amounted to 3% - so the reaction to the reports of renewed military attacks from both Iran and the US has had limited impact so far. The US have called their actions defensive, attacking a drone launch site and downing drones. This was followed by Iran’s attack on a US base. The US has also announced additional sanctions on Iran in an attempt to curtail Iran’s ability to profit from ships transiting through the Strait of Hormuz. Kuwait also reported drone and missile activity. President Trump has also stated that he doesn’t care about the mid-term elections and that higher gasoline prices would not pressure him to make a bad deal with Iran.

The AAA daily national average price of a gallon of gasoline hit a new high on 20th May and has advanced by over 50% since the conflict began. Trump’s statement reflects his confidence that rising energy prices are not impacting his popularity after his endorsed candidate in the Senate Republican primary in Texas (Ken Paxton) defeated the sitting Senator John Cornyn on Tuesday. However, the result prompted the Cook Report to alter its prediction for Texas from ‘Likely’ to ‘Lean’ Republican implying the Democrat candidate James Talarico has a better chance winning in November. The Economist’s Trump Approval rating index as of 24th May stands at -24, the worst reading of his second term in office to-date and far worse than at this stage in his first term or in President Biden’s term. Trump likely does care about his approval rating, and the Republicans certainly do care about the mid-terms so the pressure on Trump to do a deal remains intense.

But the consequence of re-escalation into conflict would be severe. And the inflation risks are building which will likely result in a greater number of FOMC officials expressing concerns over inflation rather than growth. The surge in equities, the AI-driven optimism and the relative stability in the labour market leaves inflation risks front and focus. Minneapolis Fed President Kashkari warned earlier that inflation was “much too high” and that the longer inflation stays high the more the Fed may have to respond. Chicago Fed President Goolsbee has just stated that inflation has been above target for years and now heading in the wrong direction.

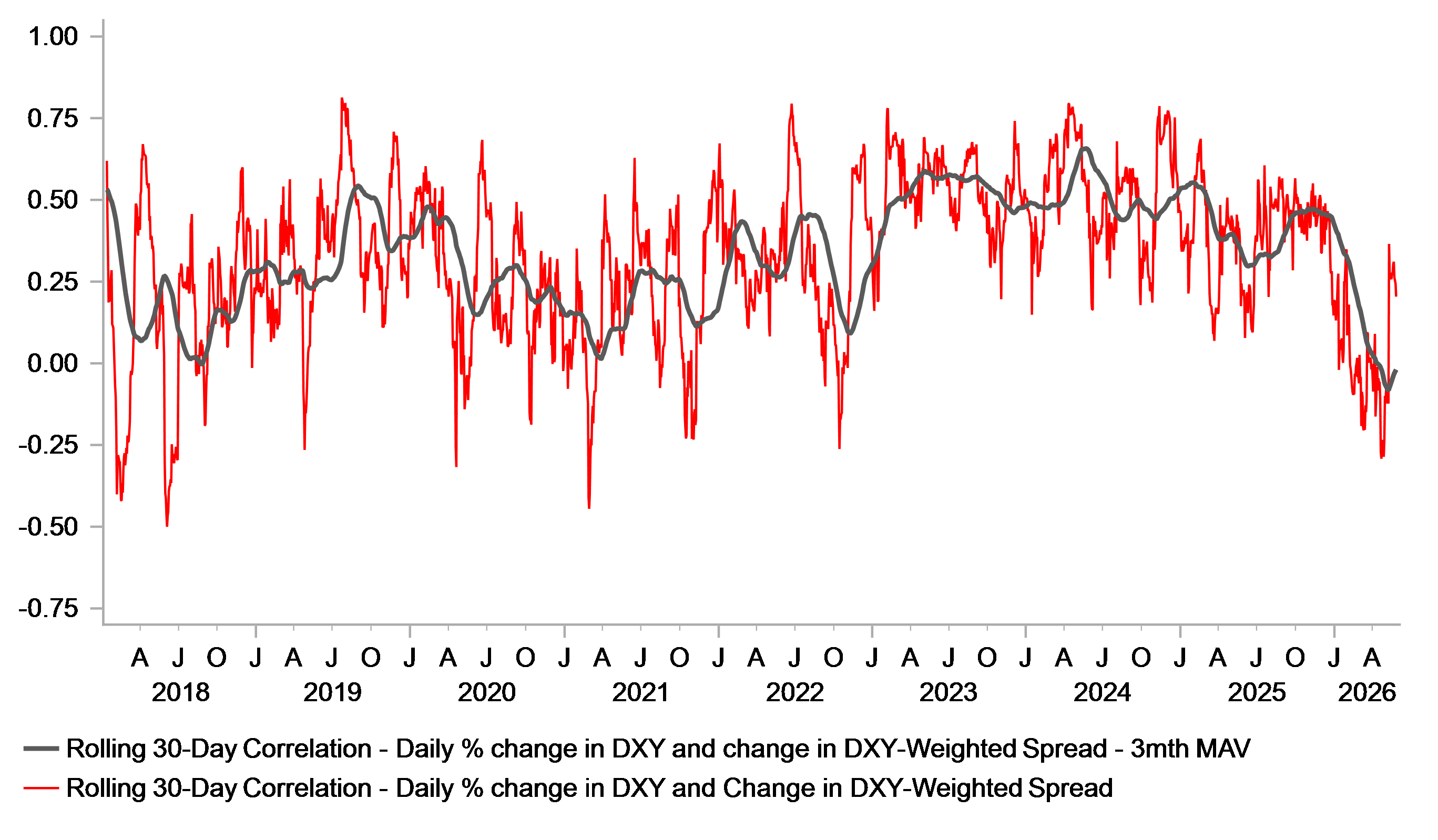

Of course, it is difficult to predict short-term developments in the Middle East and we could suddenly see prospects of a peace deal revived but if that doesn’t happen then US yields will see a renewed move higher and with yield spreads and FX correlations strengthening once again, the FX response will be further dollar strength.

RENEWED SIGNS OF RATE SPREAD/FX CORRELATION STRENGTHENING

Source: Bloomberg, Macrobond & MUFG Research

AUD/NZD: Popular trade unravels

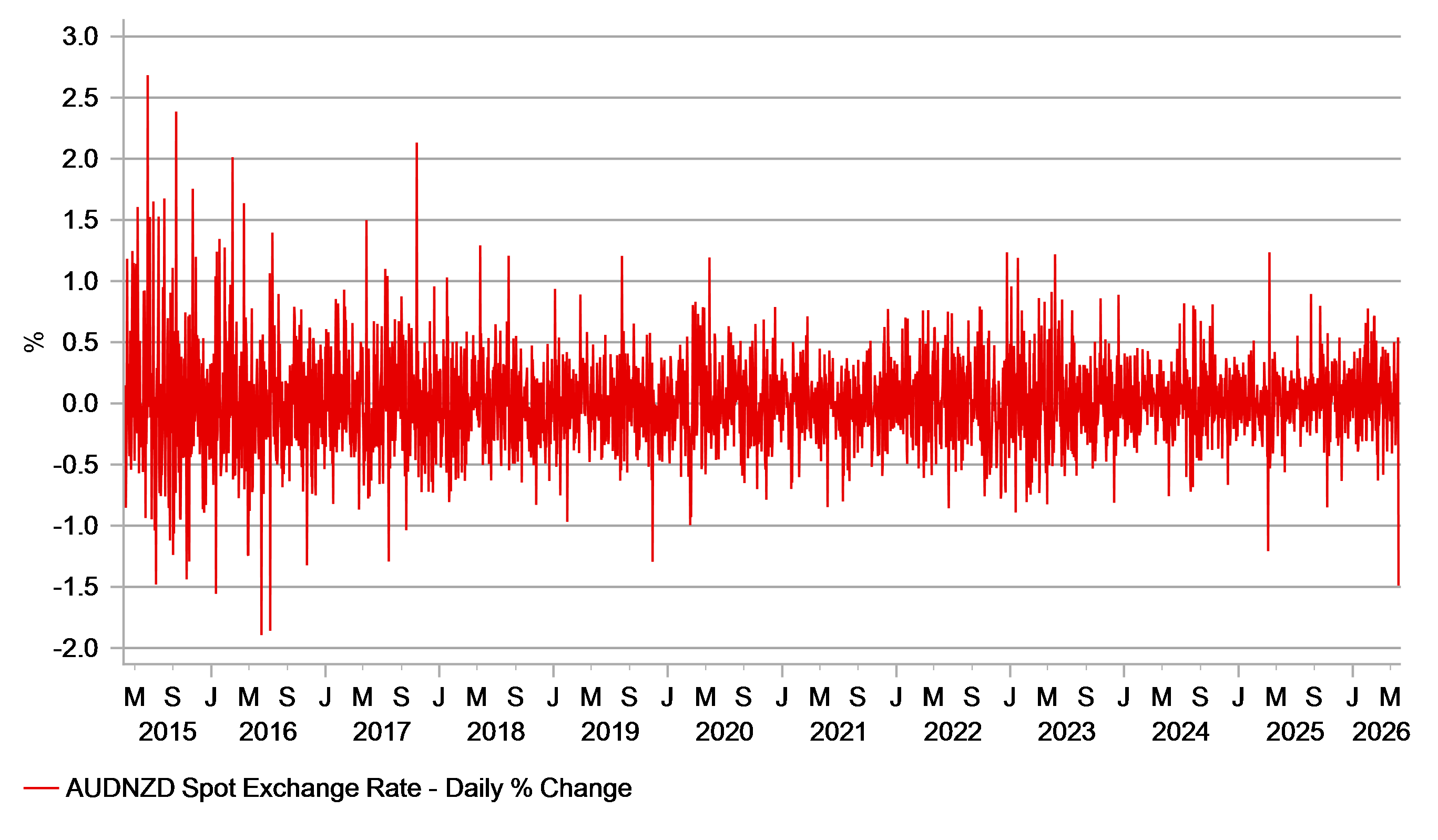

We covered the Australian dollar in the FX Weekly (here) that we released on Monday with the key message that the strong gains for the Australian dollar may be coming to end and that if rate spreads as a driver of FX was returning as a more dominant driver then there were potential headwinds ahead for AUD. That was evident yesterday – the 1.5% drop in AUD/NZD was in fact the largest one-day decline since 2016. For approaching a year now, the fundamental backdrop for AUD/NZD clearly favoured the upside. From the closing level at the end of June last year, AUD/NZD advanced by 13.75% to the closing high on Tuesday – a very sizeable move in a little short of eleven months. The closing high on Tuesday was the highest close since April 2013. The far more pro-active monetary policy approach of the RBNZ contrasted to a more measured approach by the RBA – both hiked rates of course after the Russia/Ukraine energy price shock took hold – but the RBNZ hiked by 525bps compared to 425bps by the RBA. That 100bps of extra tightening did a lot more damage to the New Zealand economy and last year, from August, policy diverged notably – the RBNZ continued to cut while the RBA remained on hold before starting to hike this year. Since June last year, the AU-NZ 2-year swap spread has surged from 25bps to a high of 160bps in April.

The RBNZ meeting yesterday potentially marked a turn in that spread, which is likely to see some of that near 14% gain in AUD/NZD reverse. The RBNZ made clear that a hike was coming and the split 3-3 vote that kept the policy rate unchanged at 2.25% (Governor Breman’s vote to hold swung the decision) was accompanied with a communication of hikes to come. We see a hike at the next meeting in July, which is not yet fully priced at 20bps. By September market pricing shows 40bps of tightening and we see a good chance now of back-to-back hikes given the messaging at the meeting this week. The RBNZ sees inflation peaking at 4.3% in Q3 and with inflation moving to a level over the 1%-3% target range, back-to-back hikes is very feasible. Governor Breman stated yesterday that the OCR is “likely to increase at coming meetings” – a clear signal.

Some investors remain sceptical given the mixed economic conditions. That’s a valid argument and the 110bps of hikes by March 2027 may not be delivered but getting to a more neutral stance over the short-term is a reasonable near-term objective for the RBNZ. With the pre-emptive nature of the RBA policy approach allowing a longer period of pause, a further extension lower in AUD/NZD seems likely.

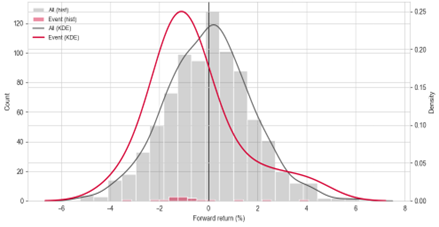

Our empirical analysis highlights that downside moves in AUD/NZD incur different implications depending on whether they are confirmed by rate differential compression. Historically, when large declines in AUD/NZD (greater than 1 std) have coincided with a meaningful tightening in the AU-NZ 2yr spread, the move persisted with 4-week forward returns averaging -0.6%. This is important in the current context, if the recent move lower in AUD/NZD reflects a turning point in rate spreads, the historical narrative would suggest that this is the beginning of a broader corrective phase rather than a short-term positioning adjustment.

AUD/NZD DROP YESTERDAY WAS THE LARGEST SINCE JULY 2016

Source: Bloomberg, Macrobond & MUFG Research

4-WEEK RETURN DISTRIBUTION FOLLOWING AUD/NZD TAILS + SPREAD TIGHTENING

Source: Bloomberg, Macrobond & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 13:30 | Core PCE Price Index (MoM) | (Apr) | 0.3% | 0.3% | !!! |

US | 13:30 | Core PCE Price Index (YoY) | (Apr) | 3.3% | 3.2% | !!! |

US | 13:30 | GDP (QoQ) | (Q1) | 2.0% | 0.5% | !!! |

US | 13:30 | Initial Jobless Claims | - | 211K | 209K | !!! |

CA | 13:30 | Current Account | (Q1) | -3.9B | -0.7B | !! |

US | 13:30 | PCE Price index (YoY) | (Apr) | 3.8% | 3.5% | !! |

US | 13:30 | PCE price index (MoM) | (Apr) | 0.5% | 0.7% | !! |

US | 13:30 | GDP Price Index (QoQ) | (Q1) | 3.6% | 3.6% | !! |

US | 13:30 | Durable Goods Orders (MoM) | (Apr) | 4.0% | 0.8% | !! |

US | 13:30 | Core Durable Goods Orders (MoM) | (Apr) | 0.5% | 0.9% | !! |

US | 13:30 | Continuing Jobless Claims | - | 1,780K | 1,782K | !! |

US | 13:55 | FOMC Member Williams Speaks | - | - | - | !! |

CA | 16:00 | BOC Press Conference | - | - | - | !! |

US | 16:30 | Atlanta Fed GDPNow | (Q2) | 4.3% | 4.3% | !! |

EU | 16:45 | ECB's Schnabel Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com