USD continues to rebound ahead of tomorrow’s FOMC meeting

USD: Higher bar for the Fed to deliver a dovish policy surprise

The US dollar has continued to rebound at the start of this week ahead of tomorrow’s FOMC meeting. After hitting a low of 103.65 on 17th July, the dollar index has risen back above 104.50 at the start of this week. In contrast, US yields at the short end of the curve have fallen to fresh lows in recent weeks. The 2-year US Treasury yield hit a low last week at 4.34% compared to the close on 17th July at 4.44%. The price action highlights that the recent rebound for the US dollar has not been driven by the hawkish repricing of Fed policy expectations ahead of tomorrow’s FOMC meeting. Market participants remain confident that the Fed will be more active in cutting rates in the year ahead. The US rate market is currently pricing in around 150bps of cuts by the end of July of next year, and around 28bps of cuts by September indicating a small risk that the Fed could start to cut rates by delivering a larger 50bps cut. With so many rate cuts already priced in, it provides a higher hurdle for the Fed to deliver a dovish policy surprise tomorrow.

Current pricing is consistent with a soft landing and US inflation moving closer to 2.0% thereby allowing the Fed to lower their policy rate back towards their estimate of the neutral rate for economy which is currently just under 3%. The release at the end of last week of the latest US PCE deflator report for June supported that view revealing that softer core inflation for the second consecutive month coming in at +0.18%M/M in June following an increase of just +0.13%M/M in May. We expect the Fed to acknowledge the recent improvement in the inflation data which should give them more confidence to begin cutting rates at their following policy meeting in September although it is not clear they will commit to take such action as early as at tomorrow’s FOMC meeting. The Fed’s annual Jackson Hole symposium is scheduled to take place between 22nd and 24th August which could be used to deliver a stronger signal that the Fed plans to start cutting rates in September.

For US rates to keep adjusting lower in the near-term, it will likely require further evidence of softening growth momentum in the US especially in the labour market. If the US rate market started to become more fearful of a harder landing, it would increase the likelihood of the Fed cutting rates even more aggressively than currently priced. However, the Fed is unlikely to be over concerned by the risk of harder landing for the US economy at tomorrow’s FOMC meeting. The US economy slowed in the 1H of this year when it expanded by around 2.0% following growth of just over 4.0% in the 2H of last year although that is still above the Fed’s long-term estimate of the potential growth rate for the US economy. One area of concern has been the grind higher for the unemployment rate since the middle of last year but that is partly driven by an improvement in labour supply. Market participants will be watching closely to see if the nonfarm payroll report for July released on Friday provides any further evidence of weakening labour demand which will be required to trigger a reversal of the US dollar’s recent rebound.

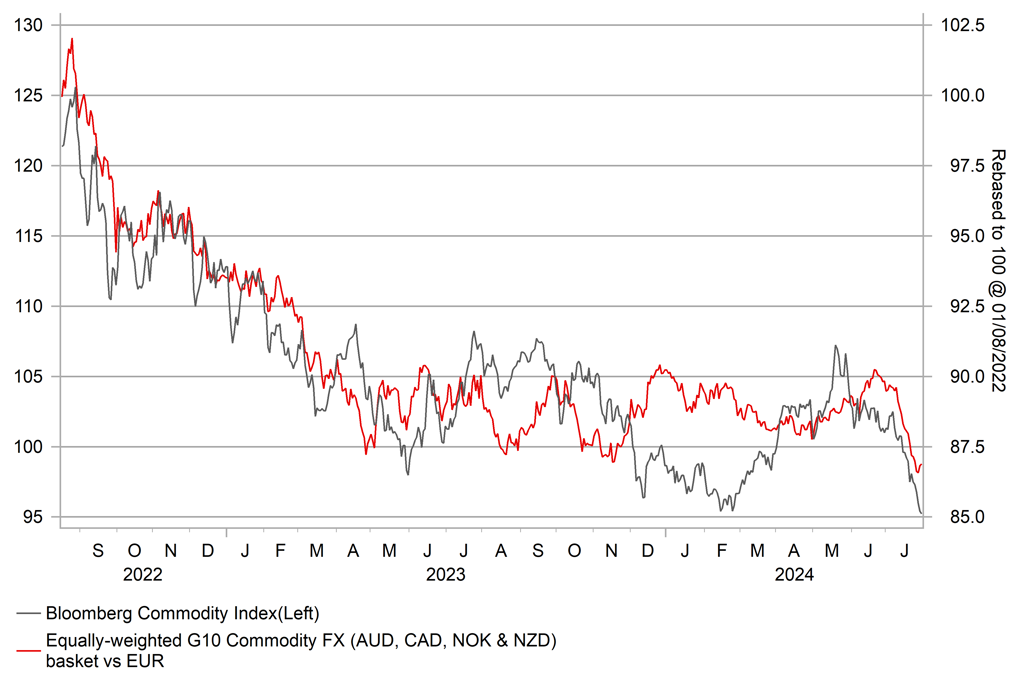

GLOBAL GROWTH CONCERNS WEIGHING ON COMMODITY CURRENCIES

Source: Bloomberg, Macrobond & MUFG GMR

EUR: Slowing growth momentum outside of the US providing support for USD

The euro has continued to weaken against the US dollar at the start of this week and has fallen back towards support from the 200-day moving average at around 1.0820. One of the reasons why the US dollar has rebounded in recent weeks has been the emergence of softening growth momentum outside of the US. After economic growth surprised to the upside in China and Europe at the start of this year, growth momentum has since slowed by the middle of this year. The decisions taken last week by policymakers in China to cut rates indicated that there is more concern that growth will struggle to meet the government’s GDP target for this year of around 5% without corrective policy action. The annual rate of GDP had already slowed to 4.7% in Q2 down from 5.3% in Q1.

At the same time, the release of the latest PMI surveys from the euro-zone signalled that business confidence deteriorated for the second consecutive month in July. The composite PMI reading of 50.1 in July compares to the average of 51.1 in Q2 and 49.1 in Q1. It does cast some doubts on the consensus forecast for the euro-zone economy to keep recovering in the 2H of this year. According to Bloomberg, the consensus forecast for euro-zone GDP for Q3 is currently estimated at 0.3%Q/Q which is similar to the pace of growth recorded on average during 1H of this year. The upward revision this morning to GDP growth in France for Q2 and Q1 both by +0.1 point to 0.3% Q/Q respectively is welcome news in light of recent negative political risks. Global growth concerns have contributed to the sharp fall in Bloomberg’s commodity price index this month which fell to a year to date low yesterday. In the FX market, the G10 commodity currencies have underperformed this month as well.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

IT |

09:00 |

Italian GDP (QoQ) |

Q2 |

0.2% |

0.3% |

! |

|

EC |

10:00 |

Business Climate |

Jul |

-- |

-0.46 |

! |

|

EC |

10:00 |

GDP (QoQ) |

Q2 |

0.2% |

0.3% |

!! |

|

GE |

13:00 |

German CPI (YoY) |

Jul |

2.2% |

2.2% |

!! |

|

US |

14:00 |

S&P/CS HPI Composite - 20 s.a. (MoM) |

May |

-- |

0.4% |

! |

|

US |

15:00 |

JOLTs Job Openings |

Jun |

8.020M |

8.140M |

!!! |

Source: Bloomberg