Yen outperforms as growth fears build ahead of “Liberation Day”

USD/JPY: Yen boosted by building fears over tariff disruption to global growth

The yen has been the best performing currency at the start of this week encouraged by more risk-off trading conditions ahead of the much anticipated announcement this week of President Trump’s plans for “reciprocal tariffs”. It quickly follows on from last week’s announcement to put in place 25% tariffs on imports of autos and certain auto parts (click here). The heightened risk of disruption to global trade and policy uncertainty have been weighing on global equity markets over the past week. The Nikkei 225 index has fallen sharply overnight by around 4% hitting its lowest level since September, and is on track for the worst quarter since Q1 2020. Bloomberg has reported overnight that President Trump plans to start his reciprocal tariff push with “all countries” after he stated “you’d start with all countries, so let’s see what happens”. He denied earlier reports for a more targeted approach that could impact 10 or 15 countries who are deemed the worst offenders. Treasury Secretary Bessent had indicated earlier this month that coming action on tariffs would focus mainly on the “dirty 15” who account for “a huge amount of our trading volumes”. President Trump attempted to provide some reassurance though that “we’re going to be much nicer than they were to us, but it’s substantial money for the country”.

At the same time, President Trump has threatened over the weekend to impose “secondary tariffs” on buyers of Russian oil if President Putin refuses a ceasefire with Ukraine although he remains hopeful that a deal can still be done. He has expressed anger at President Putin for casting doubt on Ukrainian President Zelenskiy’s legitimacy as a negotiating partner. A similar threat of “secondary tariffs” was also made to Iran alongside “bombing” until it signs a deal that renounces nuclear weapons. The initial impact on the price of oil has been muted at the start of this week with the Brent continuing to trade between USD70 and USD75/barrel where it has spent most of the last seven months.

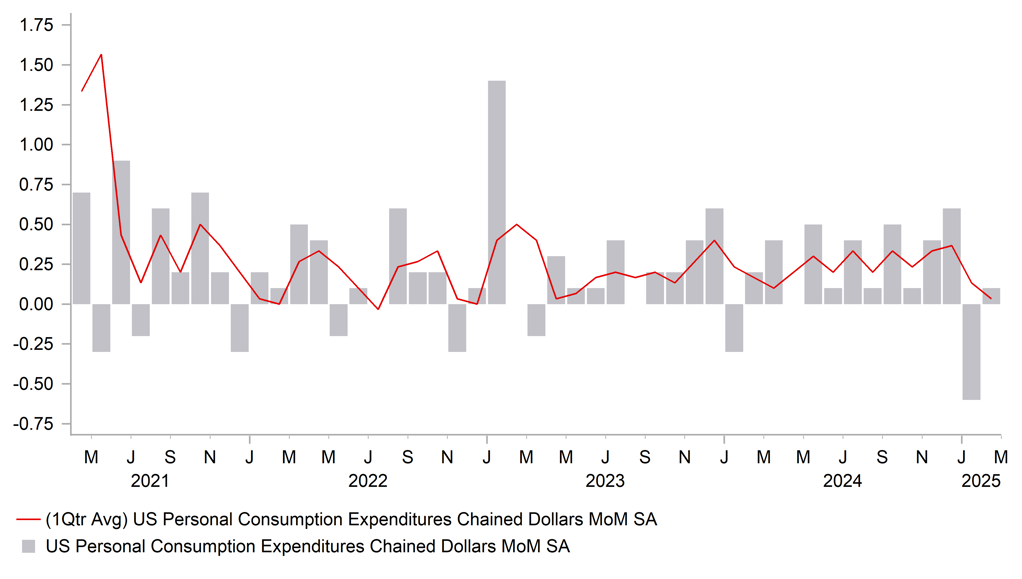

More risk-off trading conditions reflect greater investor concern over the negative economic fallout from President Trump’s tariff plans and heightened policy uncertainty. It is encouraging market participants to price in more rate cuts from major central banks. The US rate market has moved to fully price in a third 25bps rate cut from the Fed by the end of this year with just over 40bps over cuts now priced in by the July FOMC meeting. Market expectations for deeper and more front-loaded Fed easing were encouraged at the end of last week by the release of weak personal spending data for February. The report revealed that real personal spending increased by just 0.1%M/M in February following a bigger than expected contraction of -0.6%M/M in January. Weak household consumption at the start of this year combined with the recent sharp drop in consumer confidence measures is adding to concerns over the risk of a more sustained US slowdown. Market participants and the Fed will be watching the release of the latest nonfarm payrolls report for March on Friday to see if US employment growth has continued to slow as well. The Fed needs to see evidence of a loosening labour market (rising unemployment rate) to resume rate cuts. The ongoing drop in US yields remains a headwind for the US dollar against other major currencies amidst more risk-off trading conditions as global growth fears build.

SLOWDOWN FOR US CONSUMER AT START OF THIS YEAR

Source: Bloomberg, Macrobond & MUFG GMR

SEK: Has SEK strength overshot improvement in fundamentals?

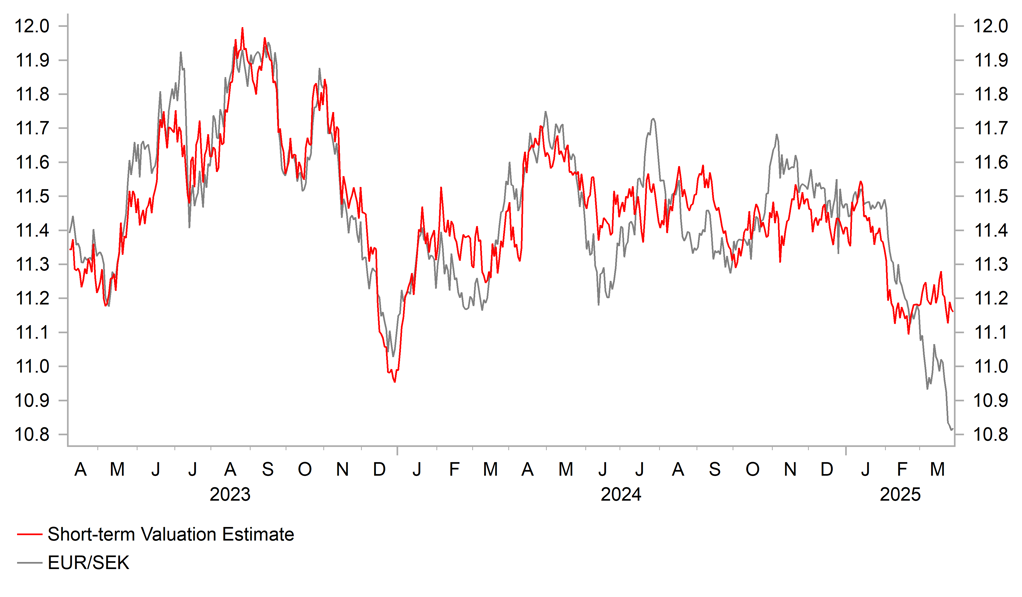

The top performing G10 currencies at the start of this year have been the European currencies of the SEK (+10.9% YTD vs. USD), NOK (+8.5%) and EUR (+4.7%) alongside the JPY (+5.6%). The outsized gains for European currencies reflect the sharp improvement in investor sentiment towards the region. It would represent the largest quarterly gain for the SEK (vs. USD) since Q3 2010 when the global economy initially recovered robustly from the Global Financial Crisis by 5.2% in 2010. More recently the SEK staged a similar strong rebound during the 2H 2020 when the global economy was recovering robustly initially from the negative COVID shock.

German Chancellor-in-waiting Friedrich Merz’s quick decision to pass legislation to finance a significant loosening in fiscal policy over the next decade or so has proven to be a game changer for the growth outlook for European economies. It could potentially result in government spending on defence and public infrastructure increasing by over EUR1.0 trillion supporting a stronger economic recovery in Germany in the coming years. At the same time, the Swedish government has announced plans last week to spend an extra SEK300 billion on defence during the next decade. The “loan-financed investment” plans to lift defence spending to 3.5% of GDP by 2030 compared to the previous target of 2.6% set last spring. The ruling coalition and its cooperation partners the Sweden Democrats agree that the change in policy is “urgent” and the “current target is not enough”. Defence spending in Sweden has already been increasing in recent years rising to 2.1% of GDP in 2024 up from 1.7% in 2023. Additional government spending on defence would support the stronger economic recovery already underway in Sweden. Economic growth picked up more strongly than expected during the 2H of last year when GDP expanded by an annualized rate of 2.8%. Stronger growth and the pick-up in inflation at the start of this year has given the Riksbank more confidence to signal an end to their rate cut cycle after lowering the policy rate in total by 1.75 points to 2.25%.

The main downside risks for the SEK that could trigger a setback after recent outsized gains would be the emergence of evidence revealing that heightened policy uncertainty and tariff disruption at the start of President Trump’s second term is having a bigger dampening impact on global growth. Sweden is a small and open economy (exports account for around 55% of GDP) which makes the SEK sensitive to global trade developments. The announcement last week of US plans to implement 25% tariffs on imports of autos and certain auto parts will add to those downside risks going forward especially the longer those tariffs remain in place. This week’s US “reciprocal tariffs” plan could further increase the risk of a more disruptive global trade war. Sweden would be negatively impacted both directly and indirectly by tariffs imposed on the EU. Please see our latest FX Weekly (click here) for more details.

SEK STRENGTH RUNNING AHEAD OF FUNDAMENTALS

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

UK |

09:30 |

M3 Money Supply |

Feb |

-- |

3,125.9B |

! |

|

IT |

10:00 |

Italian CPI (YoY) |

Mar |

-- |

1.6% |

! |

|

GE |

13:00 |

German CPI (YoY) |

Mar |

-- |

2.3% |

!! |

|

US |

14:45 |

Chicago PMI |

Mar |

45.5 |

45.5 |

!! |

|

US |

15:30 |

Dallas Fed Mfg Business Index |

Mar |

-- |

-8.3 |

! |

|

AU |

23:00 |

Manufacturing PMI |

Mar |

52.6 |

50.4 |

! |

Source: Bloomberg