Safe haven currencies continue to benefit from global growth fears

USD: Intensifying growth fears trigger pick-up in FX market volatility

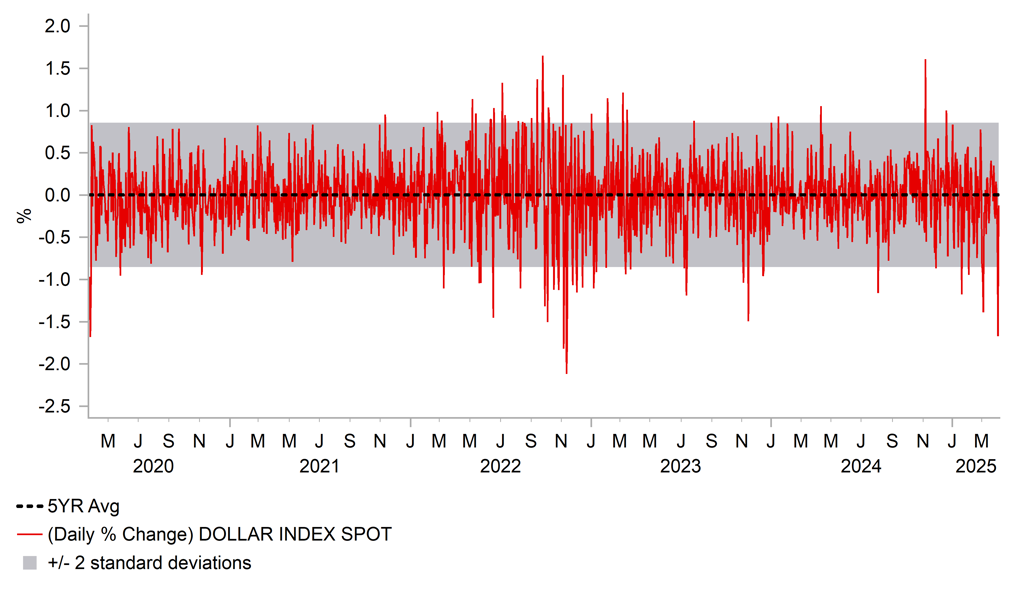

The US dollar has continued to trade at weaker levels overnight after yesterday’s sharp sell-off in response to President Trump’s plans for “reciprocal tariffs”. The dollar index declined by 1.7% yesterday on a closing price basis which was the largest daily sell-off since November 2022. The US dollar’s performance overnight has been more mixed. It has continued to weaken against Asian currencies with the biggest losses recorded against the South Korean won (-1.1%) and Taiwan dollar (-1.0%). However, it has rebounded against the more high beta G10 commodity currencies of the Australian (-1.3% vs. USD) and New Zealand dollars (-1.2% vs. USD). Both currencies have been undermined by intensifying fears over a slowdown in global growth. Bloomberg’s commodity price index has fallen sharply by almost 3% over the couple of trading days with an even bigger sell-off for the price of oil (-7.2%) which was reinforced by the surprise decision yesterday from OPEC+ members to increase output faster than previously announced. Output will be increased by three times the planned amount in May in what delegates described as a deliberate effort to drive down prices to punish the group’s cheats. Heightened concerns over a sharper slowdown in global growth have also been evident by the deepening sell-off in global equity markets. The S&P 500 and Nasdaq equity indices both declined sharply by around 5% and 6% respectively yesterday extending the move below the peaks from earlier this year to around 12.3% and 17.8%. It is the biggest correction lower for US equity markets since between late 2021 and 2022. The continued reversal of US exceptionalism trades has been contributing to broad-based US dollar weakness despite more risk-averse trading conditions when the US dollar tends to outperform alongside other traditional safe haven currencies of the yen and the Swiss franc.

At the same time market participants are currently placing more weight on the downside risks to growth in the US from President Trump’s tariff hikes than the hit to growth outside of the US. It has been estimated that the tariff hikes, if implemented as planned and remain in place, could potentially raise revenues for the US government of around USD400 billion per year although that is clearly highly uncertain. The tariffs are likely to be watered down over time and demand for imports could fall more than expected resulting in lower collected tariff revenues are just two factors that could lower the impact. However, at face value it highlights the scale of the tax hike set to hit the US economy accounting for just over 1% of GDP of fiscal tightening. Importantly in terms of sequencing the fiscal tightening is being put in place alongside DOGE’s recent efforts to cut back the size of the state, and before President Trump’s plans for tax cuts and deregulation that should provide support for growth further down the line. Heightened investor concerns over the outlook for US growth in the near-term have encouraged US rate market participants price in more active easing from the Fed this year with a further 100bps of cuts now priced in by year end. For the Fed to cut rates even as inflation picks up in response to tariff hikes in the coming months, it will need to see clear evidence that the labour market is loosening more than expected. The release yesterday of the weaker ISM services employment sub-component and the pick-up in Challenger job cuts in the government sector have added to expectations that US employment could slow further in today’s nonfarm payrolls report before even the full impact of tariffs becomes evident in the coming months.

The disruptive impact for the US economy and global growth could yet be curtailed if President Trump decides to water down his tariff plans. Under his current plans the US trade-weighted average tariff rate is expected to rise up towards 25%. It would be the highest level since the Smoot-Hawley tariff Act was introduced in 1930 and subsequent global trade war that contributed to the Great Depression. One would hope that those lessons would have been learnt and will not be repeated. In comments made overnight President Trump said he was open to reducing his tariffs if other countries were able to offer something “phenomenal”. He added that “the tariffs give us great power to negotiate”, and that “every country has called us”. On the other hand though he also indicated that further sectoral tariffs on semiconductors and pharmaceuticals will be announced in the “near future”.

The risk of a more disruptive trade war would escalate further if other major trading partners who have a stronger bargaining positions such as the EU and China decide to retaliate. Trump administration officials have warned that they are prepared to raise tariffs further in response. Bloomberg reported yesterday that France and Germany are pushing for a more robust reaction to US President Trump’s tariff measures advocating for a forceful retaliation that could strengthen the EU’s negotiating position. French President Macron reportedly believes that the EU should be ready to respond with options such as targeting US tech and services including applying a digital services tax on US companied by the end of April. He also wants to make sure the EU responds with all its instruments to defend EU interests. Bloomberg has previously reported that the EU could consider deploying the bloc’s anti-coercion instrument. EU trade ministers are due to meet on 7th April to discuss the US measures and the EU’s response. Retaliation and/or measures to support growth from other countries would continue to play into US dollar weakness until global growth fears dominate.

SHARP INITIAL SELL-OFF FOR USD IN RESPONSE TO TRUMP’S TARIFFS

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

09:00 |

ECB's De Guindos Speaks |

-- |

-- |

-- |

!! |

|

UK |

09:30 |

Construction PMI |

Mar |

46.3 |

44.6 |

!!! |

|

US |

13:30 |

Average Hourly Earnings (MoM) |

Mar |

0.3% |

0.3% |

!!! |

|

US |

13:30 |

Nonfarm Payrolls |

Mar |

137K |

151K |

!!! |

|

US |

13:30 |

Unemployment Rate |

Mar |

4.1% |

4.1% |

!!! |

|

CA |

13:30 |

Employment Change |

Mar |

10.4K |

1.1K |

!! |

|

CA |

13:30 |

Unemployment Rate |

Mar |

6.7% |

6.6% |

!! |

|

US |

16:25 |

Fed Chair Powell Speaks |

-- |

-- |

-- |

!!! |

|

US |

17:45 |

Fed Waller Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg