USD is staging modest rebound ahead of NFP report

AUD: RBA rate hike expectations scaled back after policy update

The US dollar has been staging a modest rebound since late last month helping to lift the dollar index back above the 200-day moving average at around 103.60 after hitting a low of 102.72 on 29th November. US dollar strength was most evident overnight against the Australian dollar which has declined by around -0.7%. The AUD/USD rate has similarly fallen back towards its 200-day moving average that comes in at around 0.6580 after failing to sustain the break back above the 0.6600-level. The US dollar has benefitted at the start of this week from the scaling back of Fed rate cut expectations. The implied yield on the December 2024 Fed fund futures contract increased by 8bps yesterday. There were no fundamental triggers for the hawkish repricing. the price action marks a correction after the sharp move lower in yields last week when the implied yield on the December 2024 Fed fund futures contract fell by 48bps. At the same time, the Australian dollar has been undermined overnight by the scaling back of expectations for further RBA rate hikes.

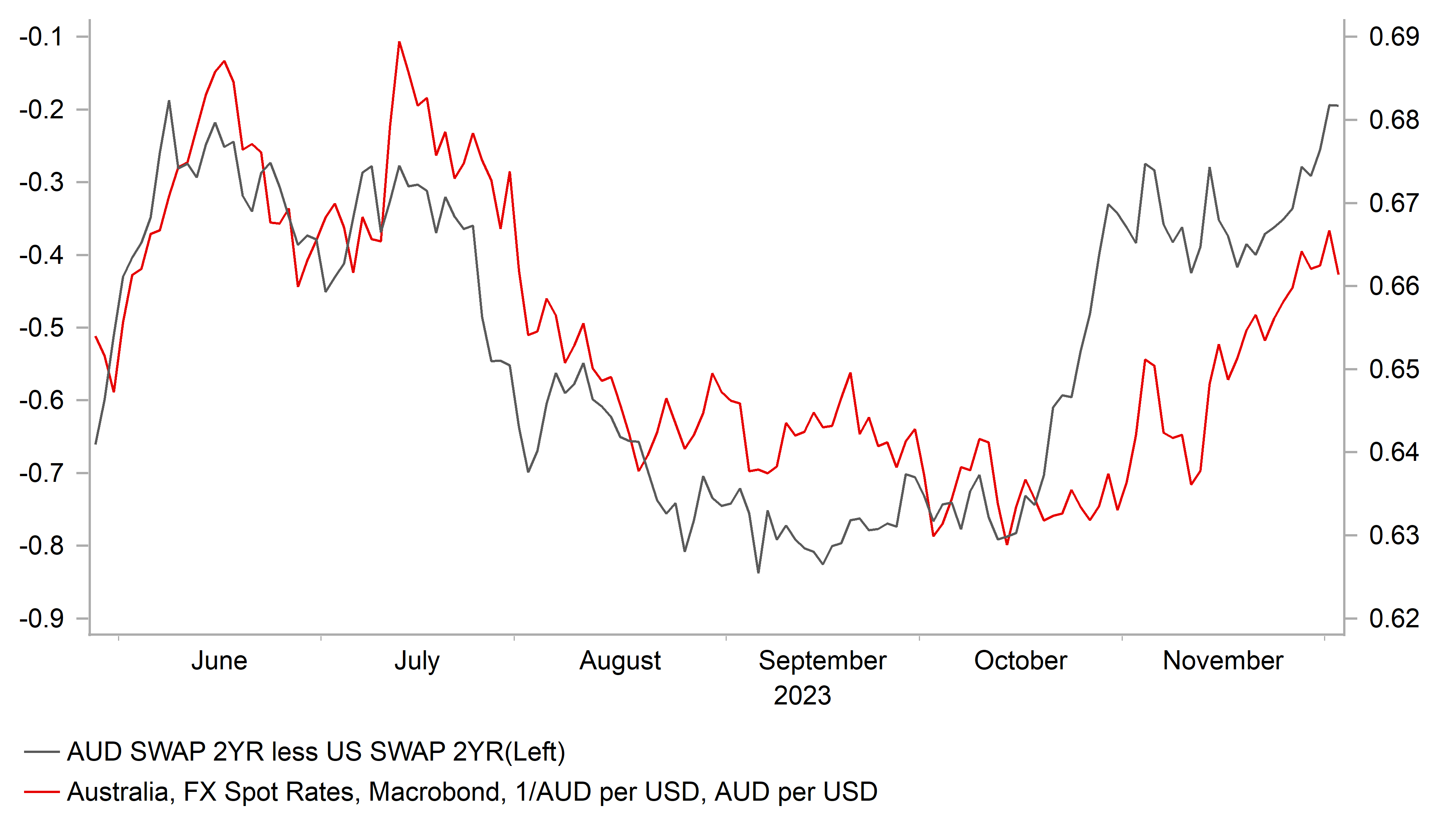

The RBA decided to leave their policy rate unchanged as expected at 4.35% following the 25bps hike delivered in November. However, the tone of the policy statement is less hawkish than expected in light of recent comments from RBA Governor Bullock and the upward revisions to the RBA’s growth and inflation forecasts delivered at the November policy meeting. The RBA noted that “the monthly CPI indicator for October suggested that inflation is continuing to moderate, driven by the good sector” but there was no updated information of services inflation since the November policy meeting. The relatively dovish description was also applied to the wage growth that “is not expected to increase much further and remains consistent with the inflation target”. As a result, the RBA repeated that “whether further tightening of monetary policy is required to ensure that inflation returns to target in a reasonable timeframe will depend upon the data and evolving assessment of risks”. It leaves the RBA in data dependency mode when setting policy, and their bias to hike rates further appears to be softening further. Still in contrast to other G10 central banks, the RBA is expected to be the least active in cutting rates next year with only 25bps of cuts priced in by the end of next year. Short-term yield spreads have been moving in favour of the Australian dollar since the middle of October.

SHORT-TERM YIELD SPREADS HAD BEEN MOVING IN FAVOUR OF AUD

Source: Bloomberg, Macrobond & MUFG GMR

EM FX: Boost for EM FX from falling US yields has started to fade

Emerging market currencies have continued to lose upward momentum against the USD over the past week even as US yields have fallen to fresh lows. While the CLP (+1.8% vs. USD) and the Asian currencies of the MYR (+0.5%), TWD (+0.5%), and THB (+0.5%) strengthened against the USD last week, there was more widespread weakness amongst other emerging market currencies. The worst performing currency was the RUB (-2.2% vs. USD) followed by the CZK (-1.4%, RON (-0.9%), HUF (-0.8%), ZAR (-0.7%), MXN (-0.7%) and PLN (-0.6%).

Emerging market currencies on the whole are currently finding it more challenging to extend their strong gains recorded during most of November. US yields have moved sharply lower again last week on the back of dovish comments from Fed Governor Waller who indicated that rate cuts could be considered in 3-5 months if inflation continues to slow. It has encouraged the US rate market to fully price in the first Fed rate cut by May and around 125bps cuts in total for next year. Yet the USD has proven more resilient. With the US rate market already priced for earlier and deeper Fed rate cuts, those expectations will now need to be backed up by further evidence of slowing US inflation and softening demand. The main test in the week ahead will be the release of the latest nonfarm payrolls report for November. Private employment growth has already slowed significantly this year which alongside an improvement in labour supply is giving the Fed more confidence the labour market is becoming better aligned. There is a risk that US yields and the USD could attempt to stage a relief rally if private employment growth exceeds the average over the last five months of around 140k.

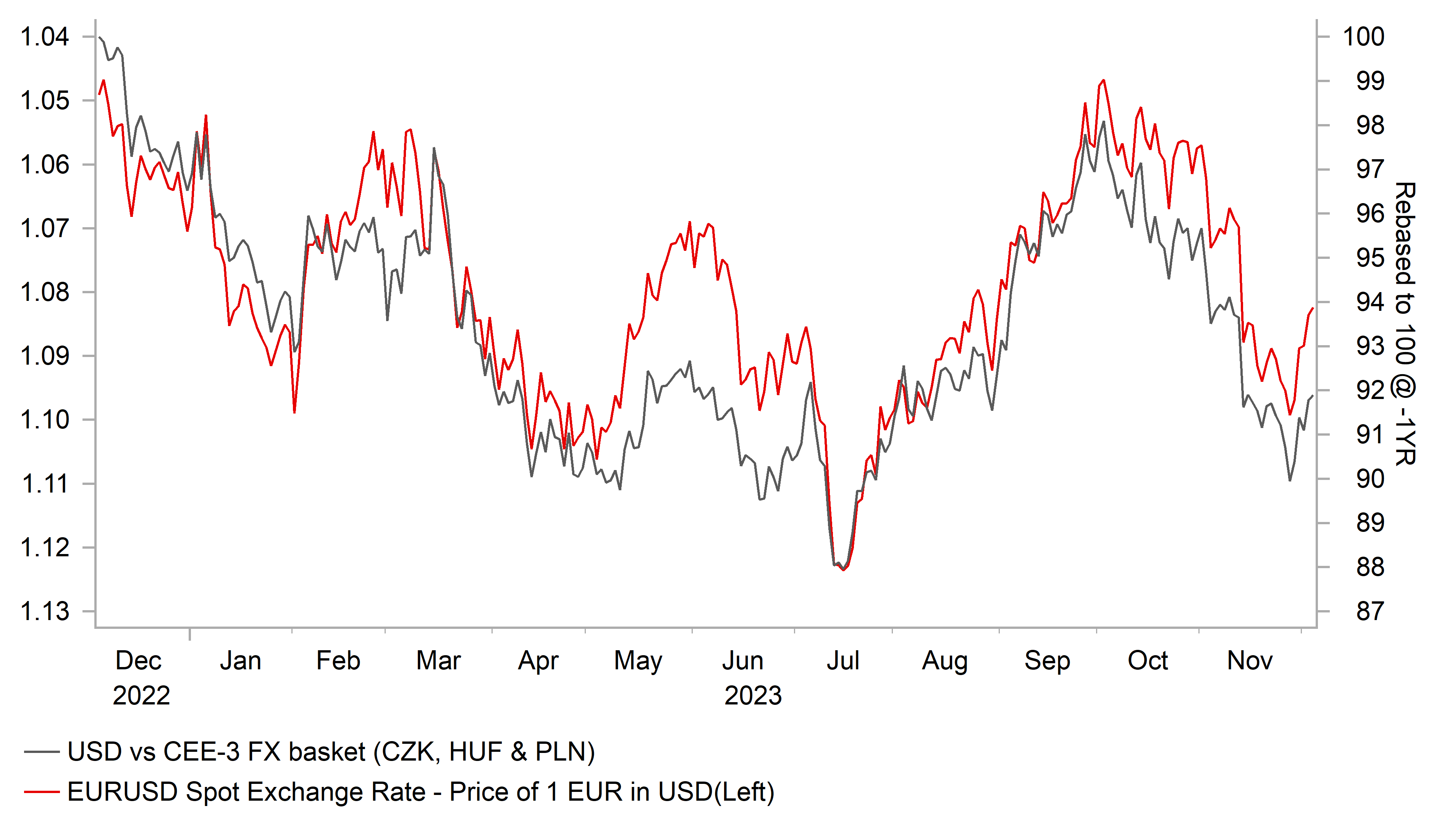

The Central European currencies of the CZK, HUF and PLN have underperformed alongside the EUR which has been the worst performing G10 currency over the past week. There has been building evidence that inflation is now falling more quickly than expected in Europe as the impact from last year’s energy price shock continues to ease. The release of the latest CPI report from Hungary will be released on Friday followed by the Czech CPI report at start of next week on Monday, and weaker prints could reinforce expectations for deeper rate cuts from the CNB and NBH. The NBP has temporarily paused their rate hike cycle after the October election citing policy uncertainty, and will holds their latest policy meeting tomorrow. One EMEA currency that has performed better over the past week has been the TRY. While USD/TRY has been more stable, it has been notable that forward rates have fallen. The one-year USD/TRY forward rate has declined from around the 40.000-level to around 38.800 supported by the TRY’s improving carry.

EUROPEAN FX UNDERMINED BY SLOWING INFLATION

Source: Bloomberg, Macrobond & MUFG GMR

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

09:00 |

Services PMI |

Nov |

48.2 |

47.8 |

!! |

|

UK |

09:30 |

Services PMI |

Nov |

50.5 |

49.5 |

!!! |

|

EC |

10:00 |

PPI (MoM) |

Oct |

0.2% |

0.5% |

! |

|

US |

14:45 |

Services PMI |

Nov |

50.8 |

50.6 |

!!! |

|

US |

15:00 |

ISM Non-Manufacturing Business Activity |

Nov |

-- |

54.1 |

! |

|

US |

15:00 |

JOLTs Job Openings |

Oct |

9.300M |

9.553M |

!!! |

Source: Bloomberg