FX Outlook through geopolitical disorder - April 2026

Scenario analysis

Three short-term scenarios to how conflict unfolds

Energy impact

- Post-shale period higher oil means stronger dollar

- …crude oil surges to surpass 2022 shock

- …crude oil surges but equity vol contained

- …rates surge more in Europe but equity vol contained

- …but US rates market was very different then

Ceasefire impact

…how quickly will SoH traffic pick up?

Energy impact

Ceasefire reversal trades from March to April

US Inflation

Energy impact should be less in the US

EZ Inflation

Under still high oil EZ CPI could jump to 3.5%

UK Inflation

Under still high oil UK CPI could jump to 3.9%

Energy impact

Nat gas price rise still modest but refined fuels higher

Fed dual targets

- Labour market mixed signals after NFP rebound

- Tariffs and now energy upside risks to CPI

Fed division

Energy shock could intensify divisions within FOMC

FOMC in 2026

A divided FOMC does not help USD sentiment

ECB policy

Energy shock is a dilemma for the ECB

Energy impact

- Japan is an energy-import heavy country

- Inflation will lower real yields in Japan

BoJ policy

R* range set to be entered this year – a JPY positive step

JGB flows

If foreigners keep buying JPY downside risks contained

FX policy

MoF will be under pressure from US to intervene

Japan & yields

Higher yields at home could impact flows over time

FX positioning

Positioning changes indicate USD buying

USD debasement

- When conflict risks subside, USD doubts to return

- 1st week of war cost US $11.3bn – more fiscal risks

Valuation

- US dollar remains over-valued

- China is well sheltered for now

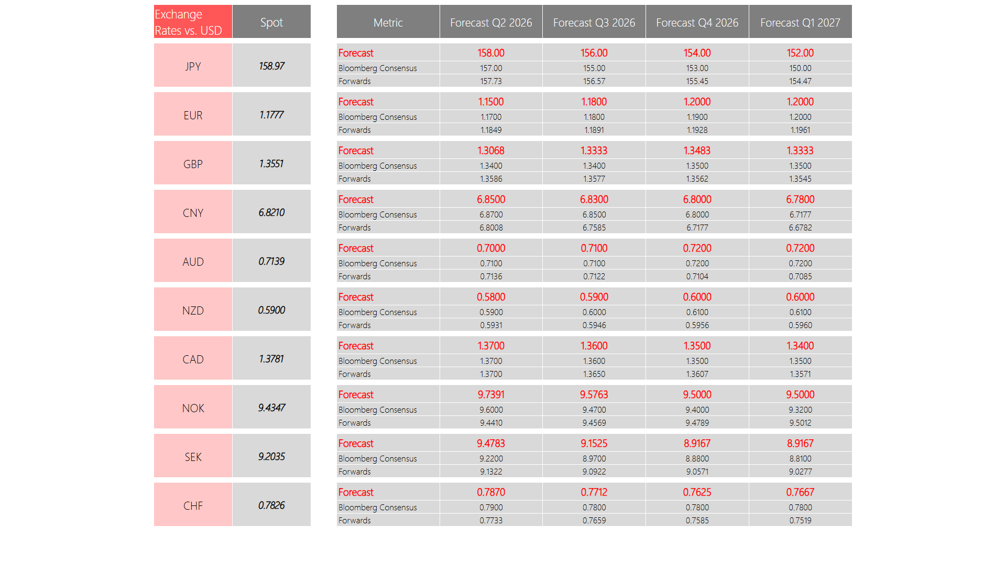

Forecast Table

Source: Bloomberg, Macrobond & MUFG Research (GMR) as of 2026; Spot Rates 15th April 2026