To read the full report, please download PDF.

Sharp rebound for USD from YTD lows

FX View:

This week the US dollar has staged a sharp rebound after the dollar index failed to break below support at the 100.00-level. It has been the biggest reversal of the bearish USD trend that has been in place since July. The bearish trend for the USD has been challenged over the past week by a number of fundamental drivers. Firstly, heightened geopolitical risks in the Middle East have provided support for the USD. Market participants will be watching closely in the week ahead to see how Israel chooses to retaliate against Iran. Secondly, market expectations for policy divergence between the Fed and other major central banks have narrowed. The much stronger NFP report for September has solidified market expectations for a smaller 25bps Fed rate cut in November. At the same time, rate markets in the euro-zone, UK and Japan have priced in more dovish policy responses from the ECB, BoE and BoJ. The developments should further discourage USD selling ahead of the US election with the chance of a Trump (USD positive) win still looming large.

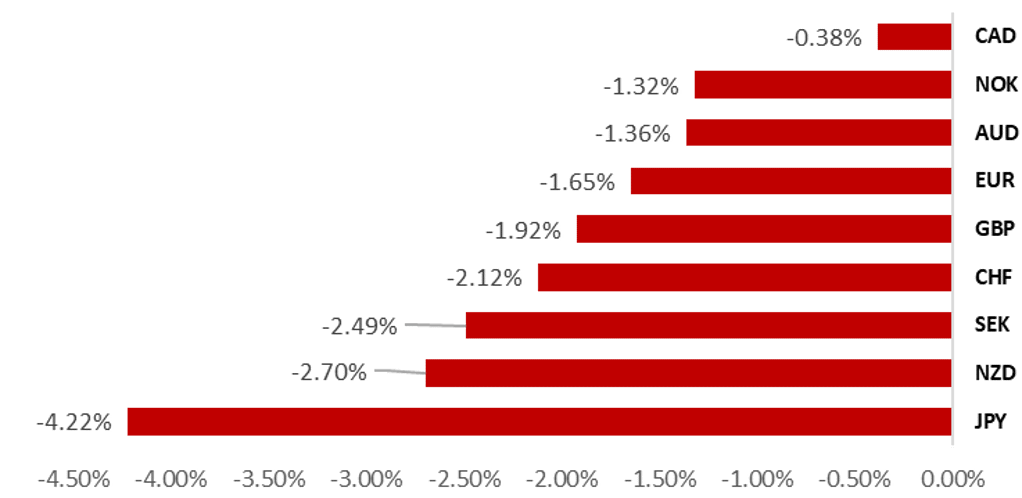

USD BOUNCES BACK AS G10 OIL FX OUTPERFORMS

Source: Bloomberg, 15:15 BST, 4th October 2024 (Weekly % Change vs. USD)

Trade Ideas:

We are cutting our short AUD/USD trade idea to reflect the risk of a further escalation in Middle East geopolitical tensions in the week ahead.

IMM Positioning:

Our two-year rolling z-scores signal revealed that short BRL and long GBP positions were the most stretched amongst Leveraged Funds. Positioning helps to explain the sharp GBP sell-off this week.

Dynamic structural impact of oil shocks on FX baskets:

Investigating the spill-over effect of the Russia oil supply shock across G10, LATAM and ASIA FX baskets, we highlight aggregate supply shocks are overwhelmingly dollar positive events where the bulk of the price action occurs in the following month. We also highlight price action across the baskets is sustained up to 6 months. For G10 FX: In the event of a global oil supply shock we would expect NZD, NOK and JPY to be the most vulnerable G10 currencies.

FX Views

USD: Muddying the waters

The USD has staged a strong rebound over the past week after falling to year to date lows at the end of last month. It has resulted in the dollar index rising back up to the 102.50-level from a year to date low of 100.16 recorded on 27th September. It is the second time that the dollar index has fallen back towards support at the 100.00-level in recent years. On the last occasion in July 2023, the dollar index tested but failed to break below the 100.00-level before staging a strong rebound (+7.8%) in the following three months. The USD rebound over the past week is the biggest reversal of the bearish trend that has been in place since July. Over the summer the USD had weakened sharply in anticipation of the Fed starting their easing cycle with larger 50bps cut in September. In last week’s report (click here), we also outlined how the package of easing measures announced by Chinese policymakers has created an additional headwind for the USD heading into year-end by boosting investor optimism over the outlook for global growth. Market participants are now eagerly awaiting plans for fiscal stimulus and evidence of stronger growth in the coming months.

However, developments over the past week have highlighted why we remained cautious over forecasting further USD downside in our latest monthly FX Outlook report (click here). The flare up in tensions in the Middle East have helped to encourage a stronger USD. Market participants have moved to price in a higher geopolitical risk premium into the price of oil to reflect heightened concerns that oil supplies could be negatively impacted by the escalating conflict in the region. Investors remain on edge waiting to see how Israel retaliates to Iran’s missile strikes in the week ahead. The escalating conflict in the region poses upside risks for the USD through a number of potential channels including: i) safe haven demand, ii) a bigger negative terms of trade shock for Europe and Asia than for the US, iii) discouraging the Fed from speeding up the pace of rate cuts in the near-term by initially creating more concern over upside inflation risks, and iv) playing into the re-election campaign for former President Trump whose proposals for higher trade tariffs and looser fiscal policy are likely to prove supportive for the USD if implemented. Our base case scenario is that upside risks for the USD from heightened geopolitical tensions in the Middle East should ease but we are more concerned over the risk of a further significant escalation now (click here).

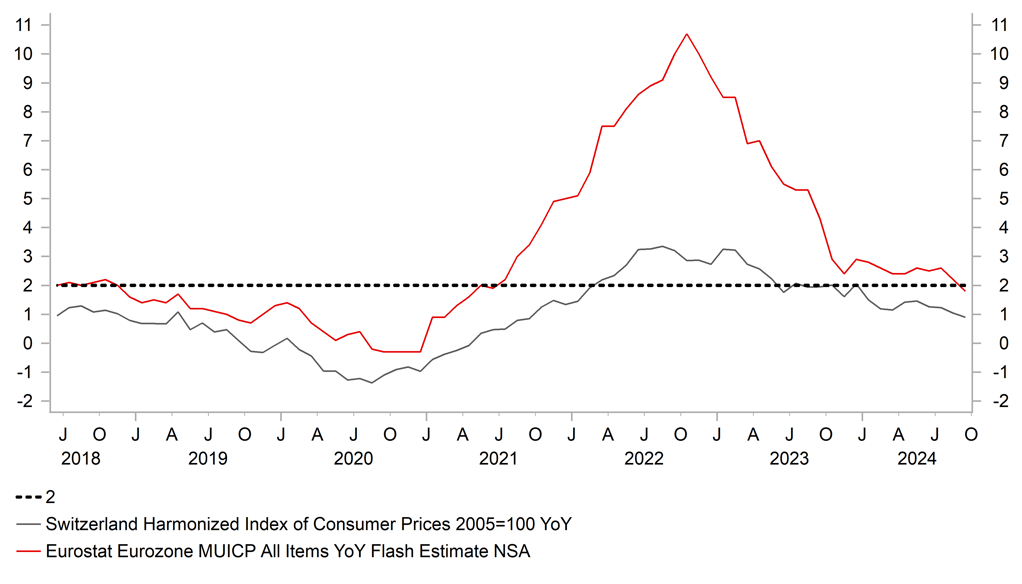

At the same time, the USD has derived support as well from the dovish repricing of monetary policy expectations for European central banks. Inflation data released in the euro-zone and Switzerland surprised significantly to the downside in September. Headline inflation in the euro-zone fell back the ECB’s target to 1.8% in September, and in Switzerland it fell even further below the SNB’s target to just 0.9% in September. The much weaker inflation readings has been quickly followed by dovish comments from ECB officials including President Lagarde and the normally hawkish Executive Board member Schnabel expressing more confidence that inflation is moving back in line with their target and providing a green light to speed up the pace of easing by delivering a back-back rate cut later this month. The euro-zone rate market has subsequently moved to fully price in 25bps rate cuts at the two remaining policy meetings this year, and every meeting during the 1H of next year which would lower the policy rate back towards more neutral levels closer to 2.00%. Another downside inflation surprise in Switzerland supports our view that the SNB should have delivered larger 50bps cut at last month’s policy meeting. Pressure continues to build on the SNB to keep cutting rates and/or intervene to weaken the CHF. The SNB will be concerned that a further significant escalation of tensions in the Middle East will encourage a sharply stronger CHF without intervention to dampen upside.

USD SUPPORTED BY HEIGHTENED GEOPOLITICAL RISKS

Source: Bloomberg, Macrobond & MUFG Research

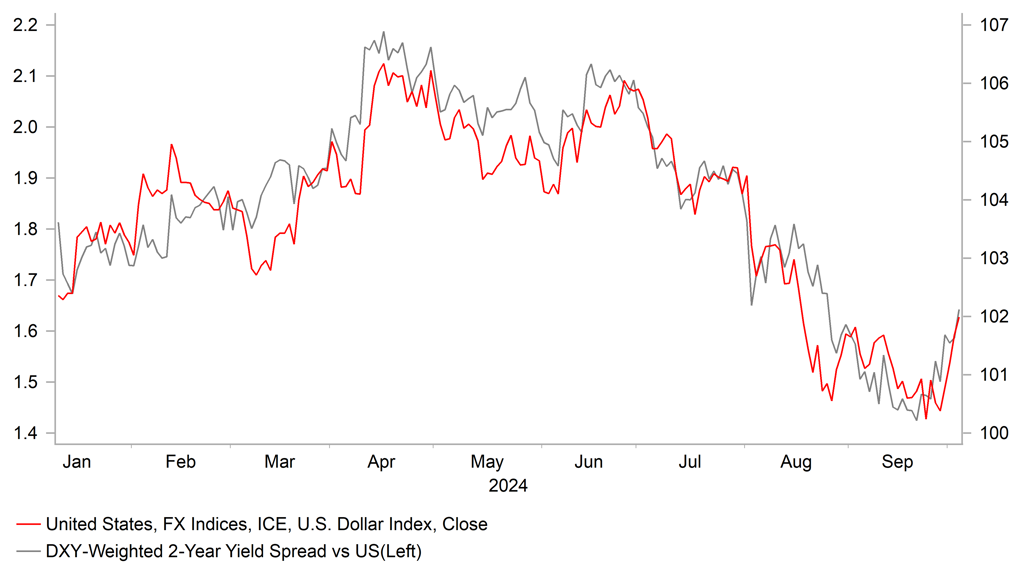

YIELD SPREADS MOVE BACK IN FAVOUR OF USD

Source: Bloomberg, Macrobond & MUFG GMR

The biggest dovish surprise for market expectations in Europe in recent days were the comments from BoE Governor Bailey who indicated that the BoE is considering joining the Fed and ECB by speeding up the pace of rate cuts if there is further positive progress for inflation. It follows the BoE’s almost unanimous decision to leave rates on hold last month that had failed to provide any strong signal that they were moving closer to speeding up the pace of rate cuts. Long GBP positions had been built up further following the September MPC meeting which helps to explain why there was such a sharp GBP sell-off in response to Governor Bailey’s dovish comments this week. The comments support our forecast for the BoE to deliver back-to-back rate cuts in November and December although we acknowledge it is far from a done deal. Comments today from BoE Chief Economist Pill remained more cautious over the need for faster and deeper rate cuts, and Governor Bailey has had a tendency to display more dovish views. A faster pace of BoE rate cuts would take some of the shine off the GBP which is still best performing G10 currency this year.

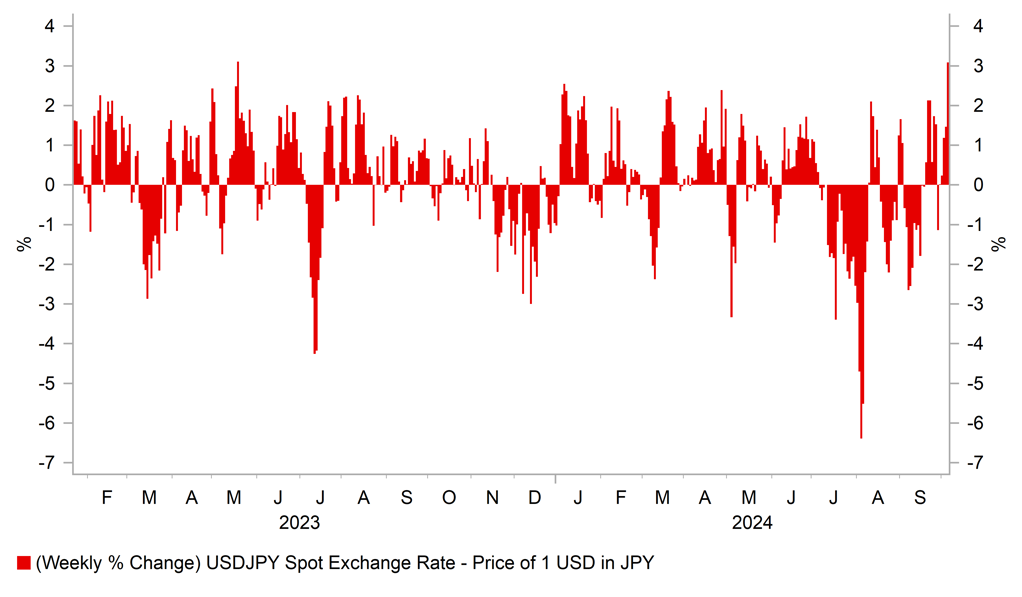

The USD has staged the biggest rebound over the past week against the JPY amongst G10 currencies. The JPY has been undermined by heightened political uncertainty in Japan following last week’s LDP election. Comments from new Prime Minister Ishiba have cast some doubt on market expectations that he was a status quo candidate who would support a continuation of policies delivered under the former Prime Minster Kishida. Initial comments from new Prime Minister Ishiba have created the impression that he is less supportive for further BoJ policy normalization now that he is in power.

He stated that Japan’s economy is “not in a condition for the central bank to raise rates again”. While his top spokesperson Yoshimasa Hayashi has since attempted to downplay the importance of those comments by stating that Prime Minister Ishiba didn’t make any specific policy request to Governor Ueda when they met for the first time this week and emphasized that the specifics of monetary policy are up to the BoJ, the initial comment has created the impression that the BoJ will be under more political pressure to slowdown the pace of rate hikes. It poses risks to our forecast for another BoJ rate hike as soon as in December although the risk of adelay to further hikes was already signalled by Governor Ueda at the BoJ’s last policy meeting in September when he stated that they have more time now given that the stronger yen and financial market instability over the summer had helped to ease upside inflation risks. From that perspective, the comments from new Prime Minster Ishiba could just be reiterating the BoJ’s updated policy stance as he attempts to further stabilize financial market conditions ahead of the snap election called for 27th October. He has already started to put together plans for additional fiscal stimulus to boost public support including cash handouts for low income households. We are not convinced that a significant shift will take place in BoJ policy under Prime Minster Ishiba. Additional fiscal stimulus could even encourage the BoJ to hike rates further by supporting Japan’s economy and giving them more confidence higher inflation will be sustained.

Finally, the release today of the much stronger nonfarm payrolls report for September has triggered a sharp move higher for US yields and reinforced the USD’s upward momentum. The report revealed that the US economy added 254k jobs in September. The strongest month of employment growth since March. Employment growth in prior months was also revised higher by 72k. After incorporating the revisions, the report still reveals that employment growth has slowed over the last six months to an average of 166k jobs/month compared to 240k in the previous six month period. At this stage we are more inclined to view the significant pick-up in employment growth in September as a one-off as it is not backed up by other labour market measures of hiring. The low response rate (62%) of the survey in September also casts some doubt on whether the strength evident in the report will be sustained.

It would be a bigger deal if stronger employment growth was repeated in the coming months. For the Fed it should not prevent them from cutting rates further this year although the likelihood of another larger 50bps cut in November has clearly diminished. The nonfarm payrolls report adds to the recent run of stronger US economic data releases. The US economic surprise index has risen back into positive territory this month and to highest level since April.

INFLATION CONTINUES TO SLOW IN EUROPE

Source: Bloomberg, Macrobond & MUFG Research

BIGGEST WEEKLY USD/JPY INCREASE SINCE MAY 2023

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Ccy |

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EUR |

10/07/2024 |

07:00 |

Germany Factory Orders MoM |

Aug |

-- |

2.9% |

!! |

|

NOK |

10/07/2024 |

07:00 |

Industrial Production MoM |

Aug |

-- |

-3.8% |

!! |

|

NOK |

10/07/2024 |

07:00 |

2025 Budget Plan |

!! |

|||

|

EUR |

10/07/2024 |

08:45 |

ECB's Lane Speaks |

!!! |

|||

|

EUR |

10/07/2024 |

09:30 |

Sentix Investor Confidence |

Oct |

-- |

- 15.4 |

!! |

|

JPY |

10/08/2024 |

00:30 |

Labor Cash Earnings YoY |

Aug |

3.2% |

3.6% |

!!! |

|

JPY |

10/08/2024 |

00:50 |

BoP Current Account Adjusted |

Aug |

¥2407.7b |

¥2802.9b |

!! |

|

AUD |

10/08/2024 |

01:30 |

RBA Minutes of Sept. Meeting |

!! |

|||

|

AUD |

10/08/2024 |

01:30 |

NAB Business Confidence |

Sep |

-- |

- 4.0 |

!! |

|

SEK |

10/08/2024 |

07:00 |

CPI YoY |

Sep P |

-- |

1.9% |

!!! |

|

USD |

10/08/2024 |

11:00 |

NFIB Small Business Optimism |

Sep |

-- |

91.2 |

!! |

|

USD |

10/08/2024 |

13:30 |

Trade Balance |

Aug |

-$72.5b |

-$78.8b |

!! |

|

NZD |

10/09/2024 |

02:00 |

RBNZ Official Cash Rate |

4.75% |

5.25% |

!!! |

|

|

EUR |

10/09/2024 |

07:00 |

Germany Trade Balance SA |

Aug |

-- |

16.8b |

!! |

|

EUR |

10/09/2024 |

17:00 |

ECB's Villeroy speaks |

!! |

|||

|

EUR |

10/09/2024 |

19:00 |

FOMC Meeting Minutes |

-- |

-- |

!!! |

|

|

GBP |

10/10/2024 |

00:01 |

RICS House Price Balance |

Sep |

-- |

1.0% |

!! |

|

NOK |

10/10/2024 |

07:00 |

CPI YoY |

Sep |

-- |

2.6% |

!!! |

|

SEK |

10/10/2024 |

07:00 |

GDP Indicator SA MoM |

Aug |

-- |

-0.8% |

!! |

|

USD |

10/10/2024 |

13:30 |

CPI MoM |

Sep |

0.1% |

0.2% |

!!! |

|

USD |

10/10/2024 |

13:30 |

CPI Ex Food and Energy MoM |

Sep |

0.2% |

0.3% |

!!! |

|

USD |

10/10/2024 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

USD |

10/10/2024 |

16:00 |

Fed's Williams Speaks |

!!! |

|||

|

CHF |

10/10/2024 |

16:30 |

SNB's Martin Speaks |

!!! |

|||

|

EUR |

10/11/2024 |

07:00 |

Germany CPI YoY |

Sep F |

-- |

1.6% |

!! |

|

GBP |

10/11/2024 |

07:00 |

Monthly GDP (MoM) |

Aug |

-- |

- |

!!! |

|

USD |

10/11/2024 |

13:30 |

PPI Final Demand MoM |

Sep |

0.1% |

0.2% |

!! |

|

CAD |

10/11/2024 |

13:30 |

Net Change in Employment |

Sep |

34.9k |

22.1k |

!!! |

|

USD |

10/11/2024 |

15:00 |

U. of Mich. Sentiment |

Oct P |

-- |

70.1 |

!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- The main economic data release in the week ahead will be the latest US CPI report for September. After picking up in August, the report is expected to reveal core inflation slowed in September. The pick-up in August had limited implications for the outlook for Fed policy as stronger inflation was mainly evident in components that carry less weight in the Fed’s preferred measure of inflation the PCE deflator. The core PCE deflator remained weak at +0.1%M/M in August compared to the stronger +0.3M/M increase in the core CPI reading. We are not expecting the CPI report to significantly alter expectations for another larger 50bps Fed rate cut in November. The size of the rate cut is more likely to depend on the health of the labour market. Comments from Fed officials including New York Fed President Williams will be watched closely in the week ahead to assess their reaction to the nonfarm payrolls report for September.

- The RBNZ holds their latest policy meeting in the week ahead. After starting to cut rates for the first time at their last policy meeting in August, market expectations have been building for the RBNZ to speed up the pace of easing in the week ahead by delivering a larger 50bps cut. The New Zealand rate market is almost fully pricing two 50bps rate cuts from the RBNZ by the end of this year highlighting that anything other than a dovish policy outcome and guidance would disappoint current market expectations. It follows confirmation that New Zealand’s economy contracted again in Q2.

- Market attention will also remain closely focused on developments in the Middle East to see how Israel responds to the missile attacks from Iran. The oil market has moved to price in a higher geopolitical risk premium although it remains relatively modest. A further escalation in tensions from the region would be supportive for the USD and other safe haven currencies, and vice versa.