To read the full report, please download PDF.

USD/JPY divergence in focus in December

FX View:

The non-farm payrolls data from the US this afternoon confirmed a still solid labour market with a 227k increase and a 56k upward revision over the two previous months. The unemployment rate drifted 0.1ppt higher to 4.2%. The report does not look strong enough to derail an FOMC rate cut this month. After that FOMC meeting the BoJ is scheduled to meet less than 12hrs later. The decision is finely balanced but at this stage we expect the BoJ to hike. Wage data this week was certainly consistent with the view of the BoJ that price stability can be achieved. The key events next week will be the US CPI data and the ECB policy meeting on Thursday. We fully expect a 25bp cut and do not expect Lagarde to signal the potential for a 50bp cut at this stage. The positive momentum for the dollar has clearly faded and there is a risk of some further liquidation of long dollar positions that could see a further reversal of dollar strength into year-end.

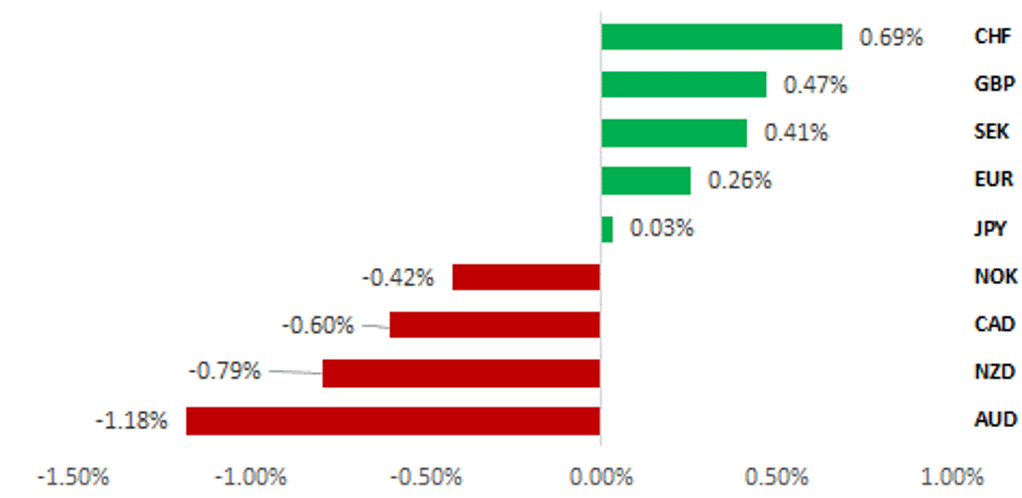

EUROPEAN CURRENCIES REBOUND WHILE COMMODITY-BASED WEAKEN

Source: Bloomberg, 14:00 GMT, 6th December 2024 (Weekly % Change vs. USD)

Trade Ideas:

We are closing our short EUR/USD trade recommendation and adding a new long USD/CAD trade idea.

IMM Positioning:

The latest IMM weekly positioning data covering the week to 19th November revealed that Leveraged Funds modestly scaled back long USD positioning after the significant build-up of long positions around the US election. The biggest long USD positions were held against the CAD, EUR and JPY.

Jingle Bells or Market Spells? The Santa Rally in FX:

While summary statistics seems to observe cyclical fluctuations over the year, our analysis suggests G10 FX does not exhibit seasonality. Applying the Friedman test and Kruskal-Wallis test to monthly returns, our analysis rejects the initial hypothesis suggesting the observed price action might be due to solely seasonal factors, and is more likely influenced by market sentiment, economic data releases and other non-seasonal factors.

FX Views

JPY: BoJ decision is finely balanced

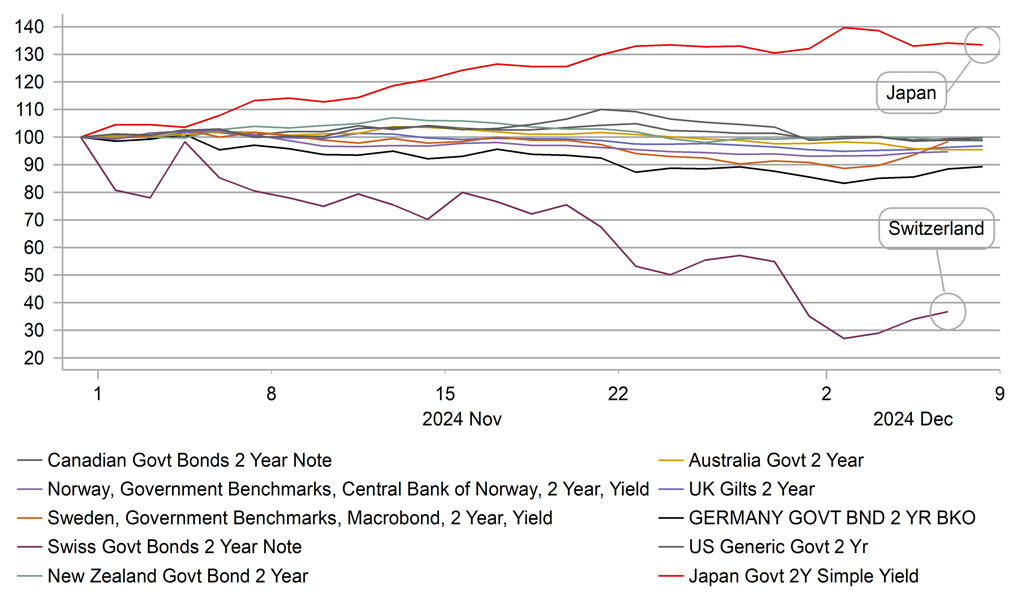

The yen has weakened versus the US dollar this week and is currently the third worst performing G10 currency this week with only NZD and AUD performing worse. The weakness this week follows a strong performance in November – when the yen was the top performing G10 currency, strengthening by 1.5% versus the dollar – the only G10 currency to have gained versus the dollar. The solid performance in November was somewhat surprising given the broad dollar strength in the wake of Trump’s election victory. The increased speculation of a BoJ rate hike in December was a primary factor in this outperformance of the yen in November. That was clear to see in the move in yields we saw in November. The 2-year JGB yield jumped 14bps in November as a BoJ rate hike in December became more plausible. In the US, despite the confirmation of victory, the 2-year UST bond yield closed down 2bps. The declines were even larger in other countries – in the euro-zone the German 2-year yield fell 33bps and in the UK the 2-year Gilt yield fell 21bps. 2-year yields declined in every other G10 country bar New Zealand where yields were unchanged. So the Japan move stood out notably helping fuel the appreciation of the yen.

But the weakness of the yen this week highlights the diminished conviction of a rate hike this month. For sure, the communications this week have not been consistent with a plan to hike and in all likelihood reflects the reality that the BoJ monetary policy board itself remains unsure. The yen performed best on Monday when Governor Ueda spoke and clearly left open the prospect of a rate hike this month without explicitly signalling one. Ueda’s comment that a rate hike was “approaching” certainly points to the BoJ positioning for a hike either this month or in January when the updated forecasts will also be presented. But there was no signal given related to this month explicitly with Ueda stating that it was “impossible” to predict the outcome of the December meeting given the large amount of data to still be released. This suggests to us that there is a high chance that if the data does warrant a hike this month we could well get a signal, possibly via the media ahead of the meeting on 19th December.

G10 2YR YIELDS REBASED FROM START OF NOVEMBER

Source: Bloomberg, Macrobond & MUFG Research

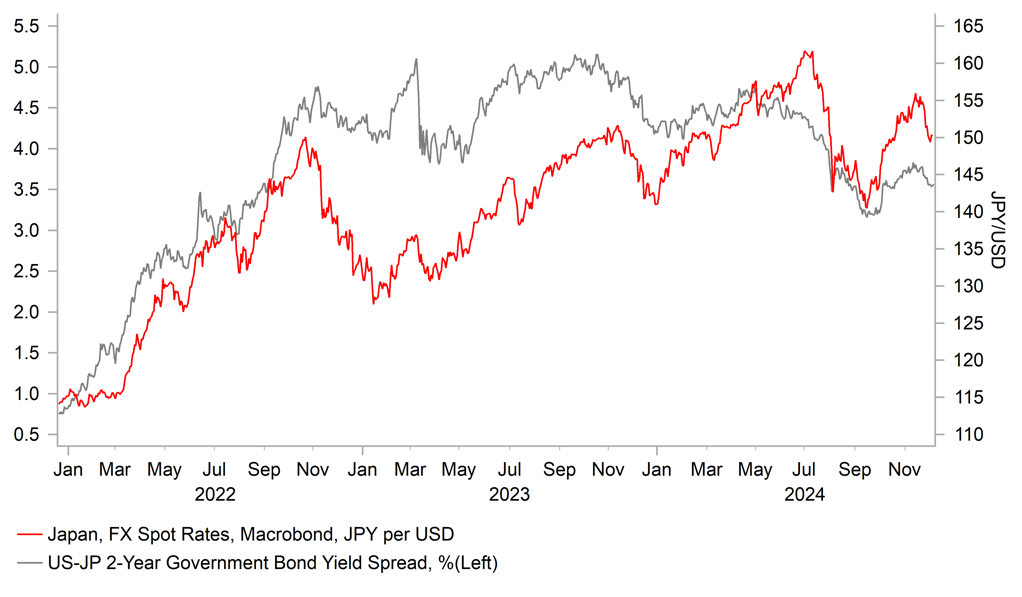

2YR US-JP GOV YIELD SPREAD & USD/JPY

Source: Bloomberg, Macrobond & MUFG GMR

However, media leaks this week only added to the confusion with MNI and JIJI Press reporting on Wednesday that there was a growing reluctance within the BoJ to hike this month. The MNI story suggested FX would be a key factor and only if USD/JPY jumped notably back above the 155-level and toward 160.00 would the BoJ consider hiking at the meeting. The JIJI report suggested the BoJ wanted to assess the impact of Trump’s early stages and what polices might be implemented immediately following inauguration on 20th January. The January BoJ meeting is four days later. Assessing Trump’s trade policies could therefore take longer than January and then the BoJ runs the risk of placing too much emphasis on foreign policy factors rather than focusing on the domestic factors. The updated projections in January also would not incorporate Trump’s possible policy announcements. The non-political foreign and domestic factors themselves will be important with the BoJ’s Tankan report next week following today’s US jobs report. The 227k increase in NFP today was broadly as expected and is consistent with the Fed delivering a 25bp cut this month. The FOMC meeting then takes place less than 12hrs before the BoJ meeting. So the reality is that if the BoJ decides not to hike this month, a hike coming four days after Trump’s inauguration could prove very challenging given it is difficult to predict what happens and what financial market conditions will be like. If the BoJ could not also raise rates in January, then the next meeting is not until 19th March. That time period is certainly not consistent with the comment from Governor Ueda on Monday that the time for the next rate hike was “approaching”. For that reason we see a hike this month as being the least risky moment for a hike if at that point the BoJ still believes the macro variables remain consistent with the achievement of its primary sustainable inflation goal.

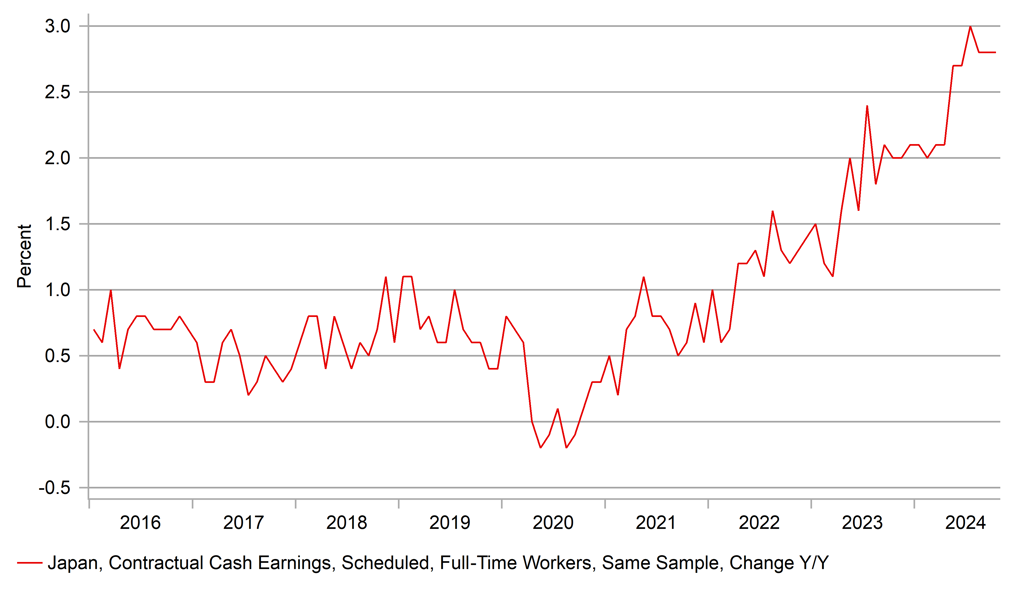

The Tankan next week will provide important additional information for the BoJ on the timing of a hike but the wage data released yesterday was certainly consistent with Governor Ueda’s comment that a rate hike was “approaching in terms of economic data being on track”. Labour cash earnings growth on an annual basis increased from 2.5% to 2.6% in October while looking at the data on a same sample basis that smooths out distortions from survey sample changes saw cash earnings remain at 2.8%, close to the recent high. Governor Ueda has stated before that a reading around 3.0% is consistent with the 2% price stability goal. While there’s a likelihood that the wage negotiated figure for FY25 agreed in the upcoming ‘shunto’ wage negotiations (5.24% this FY) the total should still be historically very high and certainly higher than the FY23 level of 3.6%. Rengo, the largest union federation is seeking “at least 5%”, and the figure will certainly be again well above inflation.

Yields have declined this afternoon in response to the jobs report that was solid but not strong enough to derail a rate cut by the Fed. USD/JPY upside risks may have receded over the very near-term. The wage data this week if followed by a Tankan report that confirms still solid inflation expectations will likely encourage the BoJ to hike in December. That points to scope for USD/JPY to move lower later this month.

‘SAME SAMPLE’ WAGE GROWTH FULL-TIME WORKERS

Source: Bloomberg, Macrobond & MUFG Research

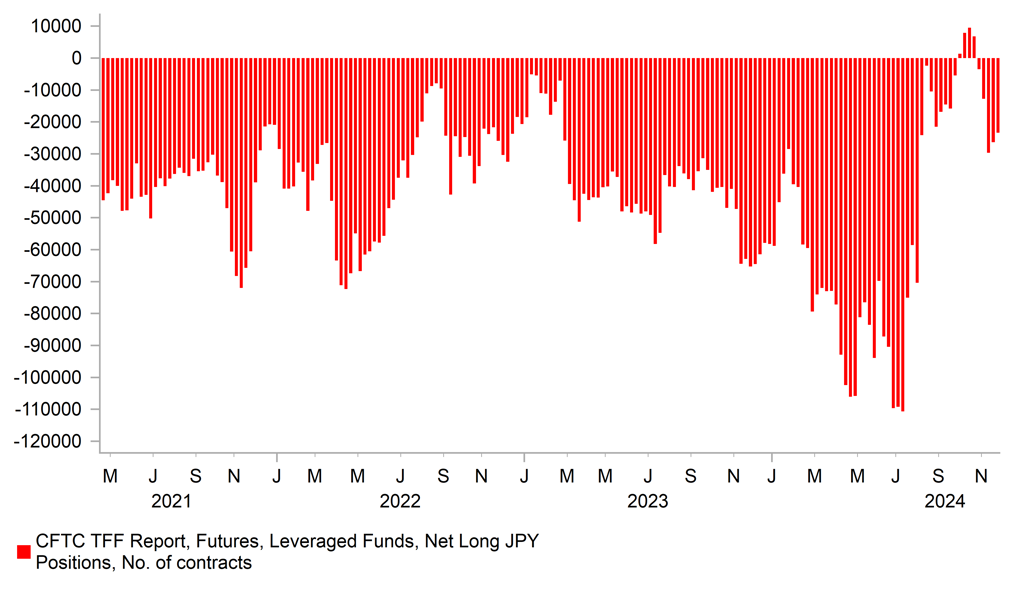

SIGNS OF RENEWED SPECULATIVE YEN SELLING

Source: Bloomberg, Macrobond & MUFG Research

EUR: Consolidating at weaker levels ahead of ECB policy meeting

The EUR has proven more resilient than expected over the past week in the face of heightened political and fiscal policy uncertainty in France. After hitting a low of 1.0335 on 22nd November, EUR/USD has since risen back up to the 1.0600-level. The low point followed the release of the much weaker than expected euro-zone PMI surveys for November which heightened fears over a sharper slowdown for the euro-zone economy and encouraged the euro-zone rate market to more fully price in the possibility of the ECB delivering a larger 50bps rate cut this month. Business confidence was hit hard initially following the US election victory for Donald Trump that has increased the threat of tariff hikes being implemented next year on US imports from the EU. It is likely though that those that fears over downside risks to the growth outlook are exaggerating weakness in economic growth at the end of this year.

The hard economic data has been stronger than the survey data this year with euro-zone GDP growth strengthening further by +0.4% in Q3. It is one reason why euro-zone rate market expectations have recently shifted back in favour of the ECB delivering another smaller 25bps cut in the week ahead. The case for sticking to more gradual 25bps cuts is also supported by sticky services inflation (~4%) and elevated wage growth in the euro-zone. The ECB staff will present updated economic projections at next week’s meeting. We expect only minor changes to the outlook for growth and inflation arguing against a bigger policy move. Forecasts for 2027 will be included for the first time which could provide a better indication of whether the ECB is confident that inflation can be sustained at their target. Recent comments from ECB officials have indicated that they remain comfortable to keep lowering rates back to more neutral levels. It supports our forecast for the ECB to lower the policy rate to 2.00% by the middle of next year. In the press conference, President Lagarde is likely to be asked about downside risks to growth posed by the threat from US trade tariffs and unfavourable political developments in France. However, it is likely premature to expect the ECB to take any policy action based on those risks at the current juncture.

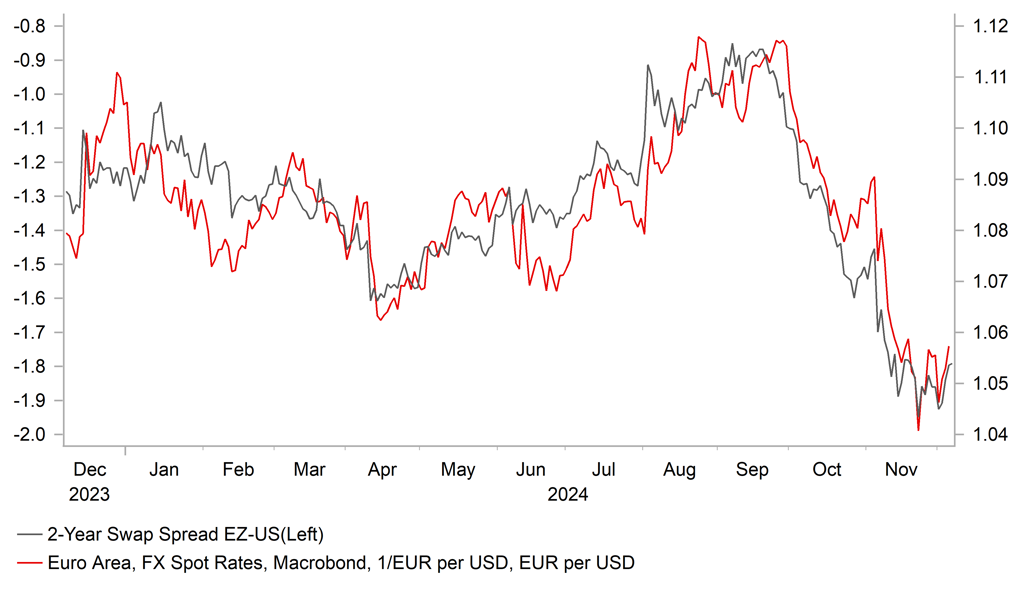

EUR/USD BOTTOMING OUT AFTER SHARP SELL-OFF

Source: Bloomberg, Macrobond & MUFG GMR

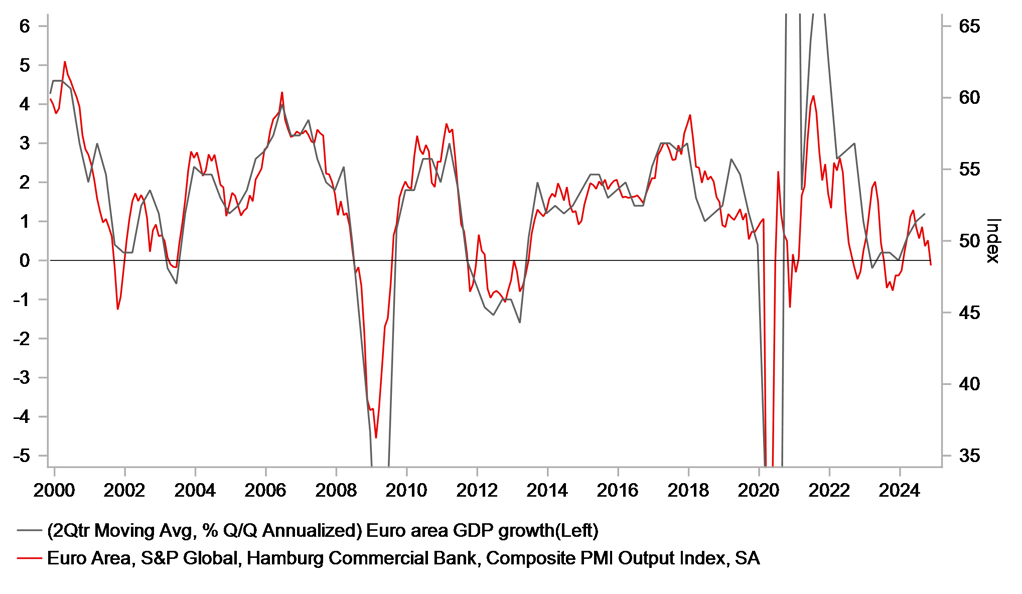

TRADE WAR FEARS ALREADY HITTING CONFIDENCE

Source: Bloomberg, Macrobond & MUFG GMR

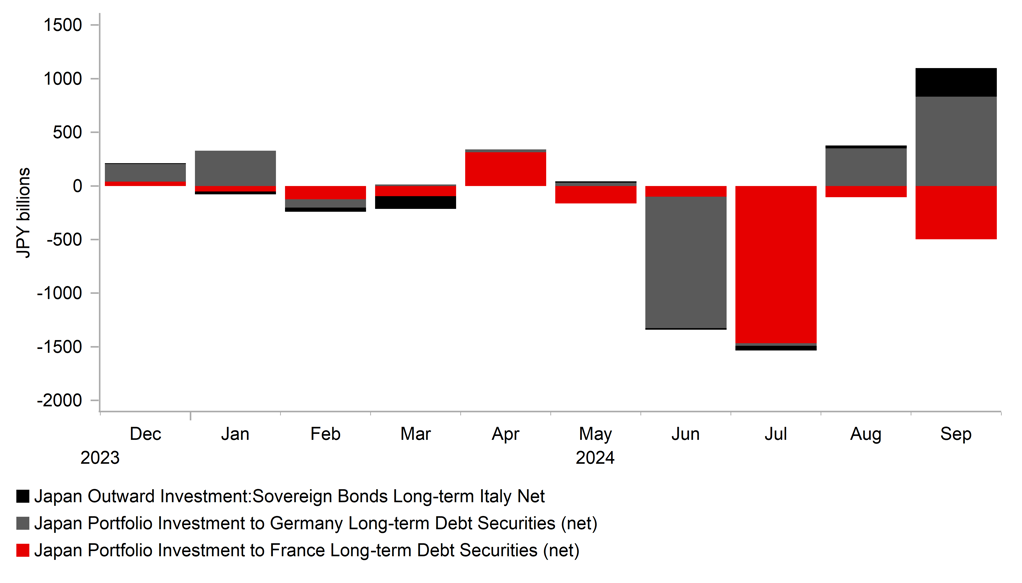

The ECB is currently in the process of scaling back support for euro-zone government bond markets as it continues to implement passive quantitative tightening. The APP portfolio is declining at a measured and predictable pace as the Eurosystem no longer reinvests the principle payments from maturing securities. Similarly, the ECB has clearly indicated that it will soon discontinue reinvestments under PEPP before the end of this year. Even though yield spreads between France and Germany have widened back out to their highest levels since the euro-zone debt crisis in 2012, we are not expecting the ECB to announce any measures to provide more support for French bonds. The higher spread will help to keep pressure on French politicians to implement fiscal tightening measures. Unfortunately, there is no majority in parliament in favour of meaningful consolidation after the government was brought down this week for pushing ahead with plans to lower the budget deficit from around 6% of GDP this year to closer to 5.5% of GDP in 2025, even after the last minute concessions from the government. One reassuring factor so far has been limited negative contagion from the loss of confidence in French government bonds and other assets since the French election in the middle of the year. A development which is helping to dampen downside risks for the euro-zone economy and the euro although one can’t really assume it will always remain that way. Yield spreads been Italian and Spanish bonds over German bonds for example have even narrowed and fallen to multi-year lows indicating they are benefitting initially from a shift away from French bonds. The latest monthly flow data from Japan reveals that Japanese investors have been net sellers of French long-term debt securities for five consecutive months to September totalling a net JPY2.33 trillion. Over the same period, Japanese investors purchased a net total of JPY197 billion of Italian long-term debt securities of which JPY241 billion were purchased in September alone. The latest monthly data for October will be released at the start of next week proving further insight on Japanese investor behaviour.

Overall the developments highlight that there is a higher hurdle now for the EUR to weaken further heading into year end. EUR/USD has already fallen sharply in the run up to and following the US election victory for Donald Trump, and market participants are now left waiting for a fresh trigger for another leg lower. Prior to the run into the US election EUR/USD was trading as high at the 1.1200-level but has since fallen by around 8 big figures in recent months. Without fresh catalysts, it is possible that stretched short EUR positions could be lightened heading into year-end. It would fit as well with the pattern of recent years when the EUR has tended to strengthen in December before reversing those gains at the next calendar year between January and March. Our quantitative analysis has found though that EUR outperformance in December is not a statistically significant seasonal pattern. Potential catalysts for a another leg for EUR/USD heading into year-end include: i) the ECB delivers or signals it is more open to delivering a larger 50bps cut, ii) the Fed skips cutting rates this month, and/or iii) President-elect Trump sends out another post on Truth Social threatening to impose higher tariffs on the EU. In light of these developments we have decided to take profit by closing our short EUR/USD trade idea, and will look for better levels to re-enter at the start of next year

JAPANESE INVESTORS HAVE SOLD FRENCH DEBT

Source: Bloomberg, Macrobond & MUFG GMR

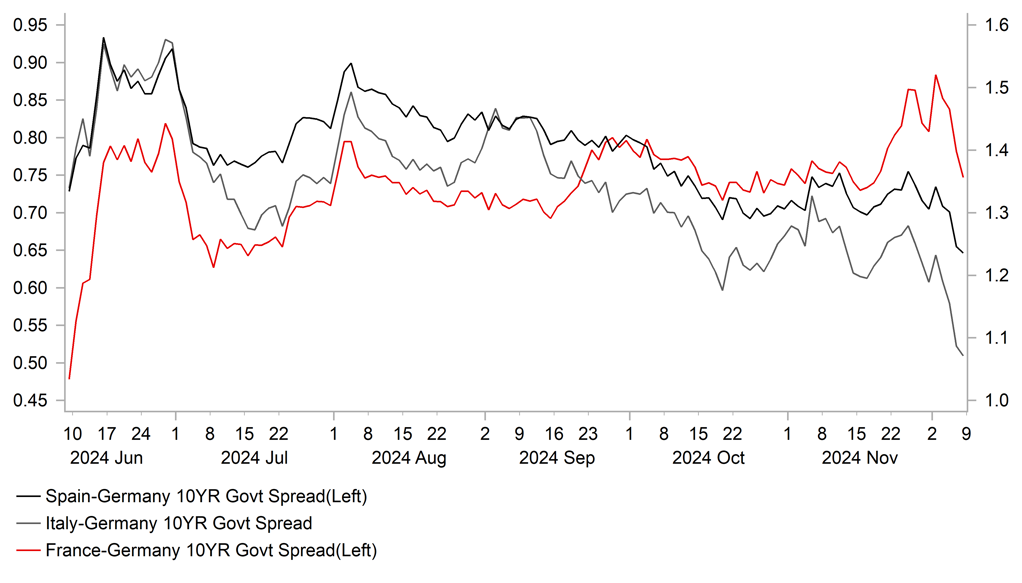

YIELD SPREADS FOR ITALY & SPAIN ARE NARROWING

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Ccy |

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

JPY |

12/08/2024 |

23:50 |

GDP SA QoQ |

3Q F |

0.3% |

0.2% |

!! |

|

EUR |

12/09/2024 |

09:30 |

Sentix Investor Confidence |

Dec |

-- |

- 12.8 |

!! |

|

GBP |

12/09/2024 |

13:00 |

BoE's Ramsden speaks |

|

|

|

!! |

|

AUD |

12/10/2024 |

03:30 |

RBA Cash Rate Target |

|

4.4% |

4.4% |

!!! |

|

NOK |

12/10/2024 |

07:00 |

CPI YoY |

Nov |

-- |

2.6% |

!! |

|

EUR |

12/10/2024 |

07:00 |

Germany CPI YoY |

Nov F |

-- |

2.2% |

!! |

|

SEK |

12/10/2024 |

07:00 |

Industrial Orders MoM |

Oct |

-- |

-3.6% |

!! |

|

USD |

12/10/2024 |

11:00 |

NFIB Small Business Optimism |

Nov |

94.1 |

93.7 |

!! |

|

USD |

12/10/2024 |

13:30 |

Nonfarm Productivity |

3Q F |

2.2% |

2.2% |

!! |

|

USD |

12/10/2024 |

13:30 |

Unit Labor Costs |

3Q F |

1.4% |

1.9% |

!! |

|

USD |

12/11/2024 |

13:30 |

CPI Ex Food and Energy MoM |

Nov |

0.3% |

0.3% |

!!! |

|

CAD |

12/11/2024 |

14:45 |

Bank of Canada Rate Decision |

|

3.3% |

3.8% |

!!! |

|

AUD |

12/12/2024 |

00:30 |

Employment Change |

Nov |

30.0k |

15.9k |

!! |

|

SEK |

12/12/2024 |

07:00 |

CPI YoY |

Nov F |

-- |

1.6% |

!! |

|

CHF |

12/12/2024 |

08:30 |

SNB Policy Rate |

|

0.75% |

1.00% |

!!! |

|

CHF |

12/12/2024 |

09:00 |

SNB's Schlegel Speaks |

|

|

|

!!! |

|

EUR |

12/12/2024 |

13:15 |

ECB Deposit Facility Rate |

|

3.00% |

3.25% |

!!! |

|

USD |

12/12/2024 |

13:30 |

PPI Ex Food and Energy MoM |

Nov |

0.2% |

0.3% |

!! |

|

USD |

12/12/2024 |

13:30 |

Initial Jobless Claims |

|

-- |

-- |

!! |

|

EUR |

12/12/2024 |

13:45 |

Lagarde Press Conference |

|

|

|

!!! |

|

JPY |

12/12/2024 |

23:50 |

Tankan Large Mfg Index |

4Q |

13 |

13 |

!!! |

|

JPY |

12/13/2024 |

04:30 |

Industrial Production MoM |

Oct F |

-- |

3.0% |

!! |

|

GBP |

12/13/2024 |

07:00 |

Monthly GDP (MoM) |

Oct |

-- |

-0.1% |

!!! |

|

EUR |

12/13/2024 |

07:45 |

France CPI YoY |

Nov F |

-- |

1.3% |

!! |

|

EUR |

12/13/2024 |

10:00 |

Industrial Production SA MoM |

Oct |

-- |

-2.0% |

!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- The RBA, BoC, ECB and SNB will all hold their final policy meetings of this year in the week ahead. The RBA is expected to leave rates on hold again at 4.35% where the policy rate has remained throughout 2024. Market participants will be watching closely to see if the RBA sends a stronger signal that they are moving closer to lowering rates at the start of next year. There is currently around a 50:50 probablity priced in for the RBA to cut rates by 25bps at the following policy meeting in February.

- After delivering a larger 50bps cut at their last policy meeting in October, we expect the BoC to deliver another 50bps cut in the week ahead although it’s possible the BoC could decide to slow the pace of easing by delivering a smaller 25bps cut. The BoC has left open the possibility of delivering another 50bps rate cut to lower the policy rate more quickly towards their estimate of the neutral rate between 2.25% and 3.25%.

- The ECB are expected to lower rates further well by delivering another 25bps cut. Recent ECB communication has indicated that they want to lower the policy rate closer to 2.00% but there has been no strong signal that a larger 50bps cut is likely to be delivered as soon as next week. The euro-zone rate market is priced for a 25bps cut next week but is attaching a higher probability of a larger 50bps cut in Q1. Market participants will be waiting to see if the ECB provides any encouragement over the possibility of larger rate cuts next year. Downside risks to growth in the euro-zone from the threat of US trade tariffs and political uncertainty in France will garner more attention in the press conference.

- Similar to the ECB there has been speculation recently that the SNB could deliver a larger 50bps rate cut in the week ahead. A view that is currently priced as more likely than another 25bps cut by the Swiss rate market. It remains to be seen whether the SNB will be willing to deliver a larger rate cut in response to the worsening inflation undershoot when the policy rate is already moving back closer to the zero bound again. We expect the SNB to emphasize as well that it remains prepared to intervene to weaken the CHF if required to address downside risks to their inflation target. The CHF has been more stable in recent months but remains close to year to date highs against the EUR.

- The main economic data releases in the week ahead are the US CPI report for November and Japanese Tankan survey for Q4. Another stronger US PCI report could discourage the Fed from their plans to cut by a further 25bps this month. In contrast, the Tankan survey will be watched closely to assess the outlook for Japan’s economy with the BoJ getting “nearer” to hiking rates again.