To read the full report, please download PDF.

ECB & political risks no recipe for EUR selling

FX View:

This week the US dollar (DXY) has fallen nearly 1.0% with the initial reaction to the US employment report mixed. The data we believe confirms the weakening momentum in the labour market but has left unclear whether the FOMC will cut by 25bps or 50bps. We believe the FOMC should cut by 50bps in order to reduce the risk of falling behind the curve. Next week the ECB meeting will be in focus and we expect the ECB to cut by 25bps, in line with the market consensus. The communications from President Lagarde will likely be similar to before – decisions will be meeting-by-meeting with more work to be done to restore price stability. Next week should also be when we get details of the new government in France under new PM Michel Barnier. We don’t see much to be gained in the near-term by RN supporting any no-confidence motion. These factors and the potential for a 50bp cut from the FOMC will help provide EUR/USD with ongoing support.

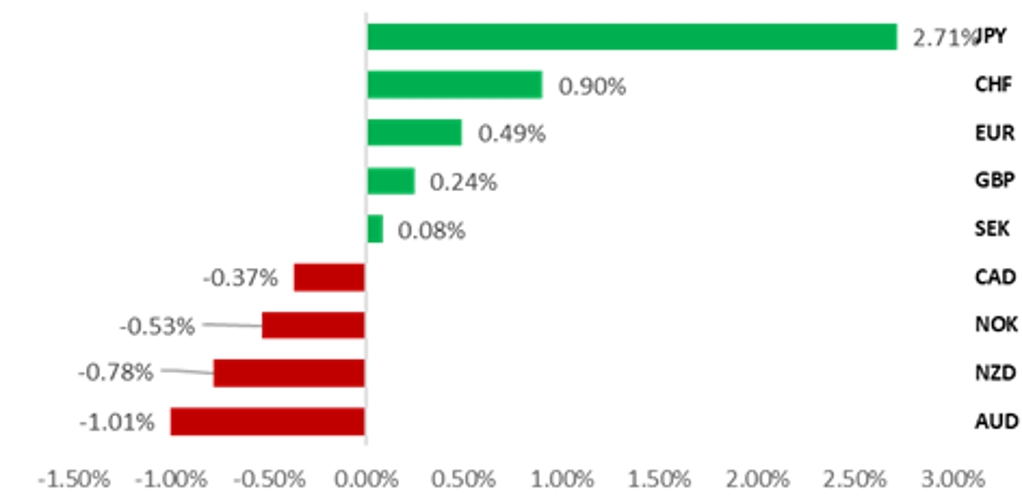

USD SELLING AGAINST OTHER FX MAJORS

Source: Bloomberg, 14:00 BST, 6th September 2024 (Weekly % Change vs. USD)

Trade Ideas:

We are establishing a new short USD/JPY trade idea based on momentum and the fundamental backdrop pointing to further declines.

JPY BoP Flows:

The latest Balance of Payments data continues to confirm a positive external position and also revealed the largest sell-off of German bonds by Japanese investors since 2015. The July data will be released next week and may showing political uncertainty in France undermining demand for bonds further.

The FX implications of pivotal Fed meetings:

Taking a look at EUR/USD and USD/JPY performance after payroll reports ahead of pivotal Fed meetings (2021 -present) we highlight for EUR/USD in the case of a USD negative initial price action after the first 6hrs, we see a sustained follow-through in price action in the periods +3 days and +1 week ahead.

FX Views

EUR: France politics – Next steps ahead & possible risks

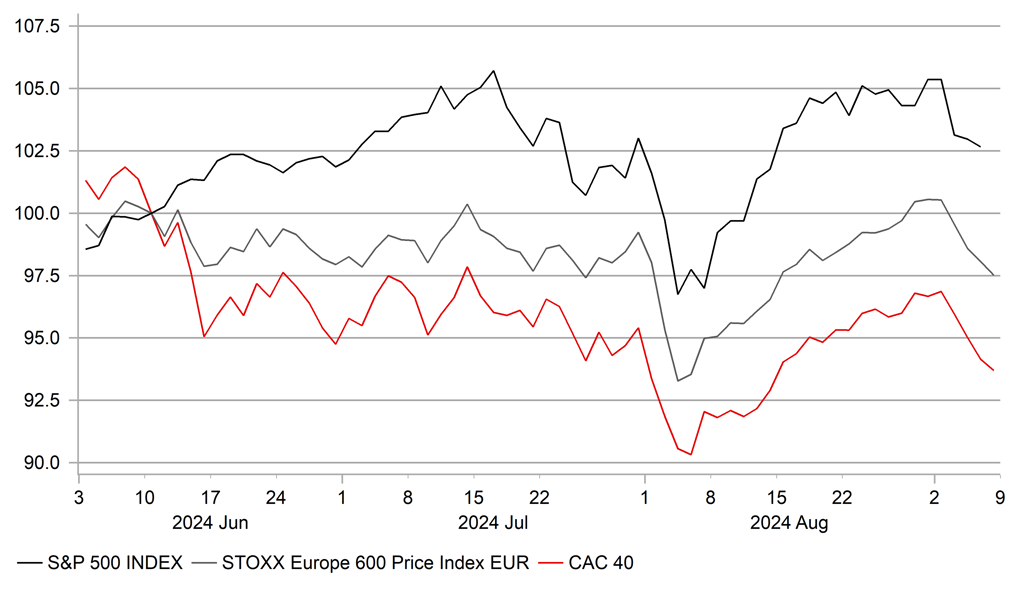

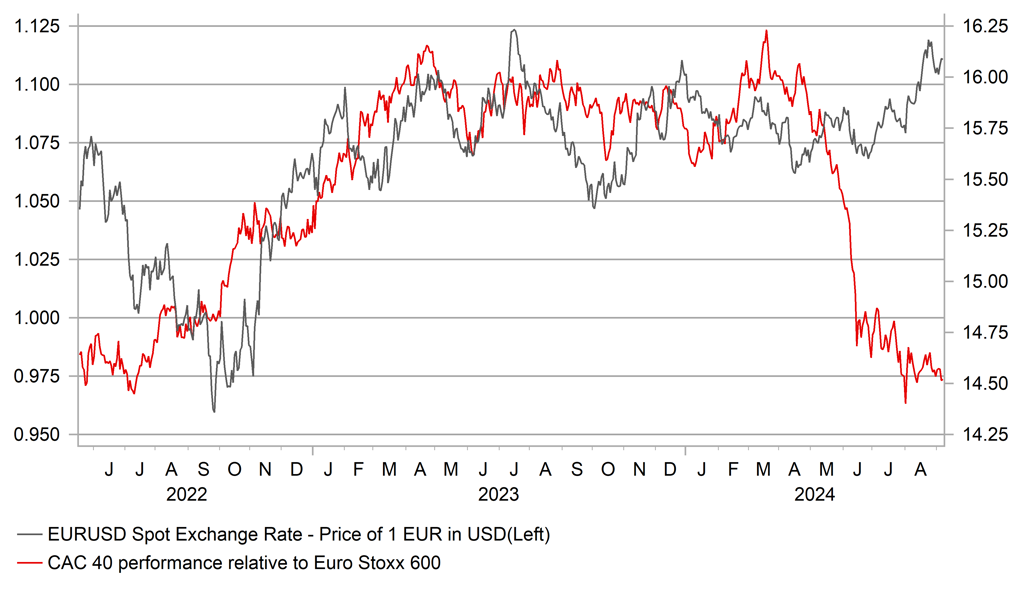

The decision of President Macron to name Michel Barnier as the new Prime Minister of France has been met with near complete indifference by the financial markets with EUR/USD being driven higher by declining yields in the US, and the OAT/Bund spread close to unchanged at marginally narrower levels. This might be explained by the fact that investors don’t have reason to expect any dramatic change in the political landscape in France – France remains in political gridlock and while we have had progress in the naming of a Prime Minister that at least for now looks acceptable for Marine Le Pen’s Rassemblement National (RN), Michel Barnier still has an immense task in breaking this gridlock. So it can be argued that the lack of financial market reaction reflects the scepticism of the new prime minister making much headway in policy implementation that would help improve investor sentiment. The CAC 40 is down 6.3% since the EU parliamentary elections in June compared to a 2.5% drop for the Euro Stoxx 600 and a 2.5% gain for the S&P 500. So what lies ahead now that France has a new prime minister and are there scenarios that could prompt some increased financial market volatility?

The French constitution (Article 8) outlines that the president has the power to appoint members of the government “on the proposal of the prime minister” and hence we can expect Macron and Barnier to choose a cabinet that will have the best chance of gaining support across the main party blocks in the national assembly. Earlier this year former PM Attal announced his senior ministers after two days while in 2022 PM Borne took four days. Given the more difficult task now, it could well take longer than in 2022 but we should still expect details next week. The next possible step could be then to hear more about the policy program of PM Barnier. There is no set time for this but it usually takes the form of a government policy statement to the national assembly and the senate. Former PM Attal gave that speech 21 days after his appointment although for former PM Borne it was 51 days. We’d expect to hear more from Barnier this month given the importance in drawing support, in particular from RN. Marine Le Pen stated this speech would help determine RN’s support for PM Barnier.

Where we do have specific dates when challenges could emerge is firstly on 20th September when France must present to the EU its proposals on bringing down its budget deficit under the Excessive Deficit Procedure that was triggered by the EU in June/July. This date could be extended to 15th October. The second date is 1st October when a budget plan must be presented to the national assembly. France’s budget deficit was 5.5% of GDP in 2023 and is forecast to remain at 5.0% in 2025, above the EU threshold of 3.0%. France’s government debt is projected to rise from 110.6% of GDP in 2023 to 113.8% in 2025, compared to a 60% EU limit. The proposed budget left by PM Attal keeps total spending in 2025 unchanged versus 2024. Under new EU rules, France will be obliged to reduce the deficit by 0.5% per year. The French Treasury estimates spending cuts of EUR 30bn will be required to meet EU requirements. Failure to do this can result in fines although that has never happened. The new EU Commission does not take office until 1st November so any rule breaches would not be formally addressed possibly until 2025. PM Barnier has strong EU links which will prove important in any negotiations with the EU over continued breaches under the Excessive Deficit Procedure.

CAC 40 HAS UNDERPERFORMED SINCE EU ELECTIONS

Source: Bloomberg, Macrobond & MUFG Research

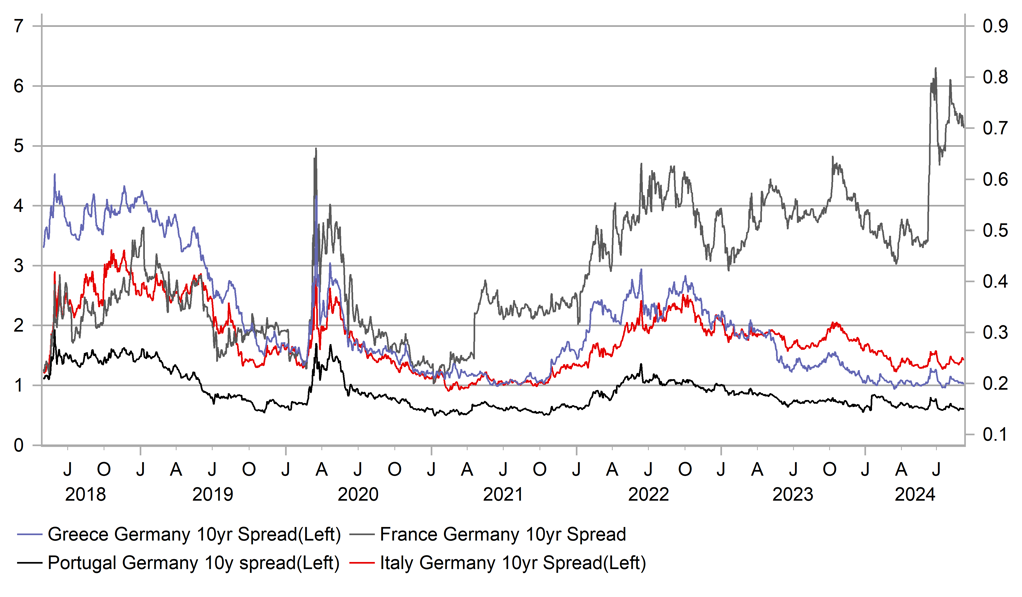

OAT/BUND SPREAD HAS SEEN LIMITED RETRACEMENT

Source: Bloomberg, Macrobond & MUFG GMR

Deficit reduction plans do not appear consistent with either the policy mandates of the party blocks on the left or the right, although RN claimed ahead of the election that it supported bringing the deficit back to the EU 3.0% limit by 2027. Most argue though that their policies to tackle the cost of living crisis would make that goal impossible. Still, there is certainly more scope in aligning with RN on budgetary policies than with the far-left. The budget issue remains the highest risk issue for triggering a no-confidence motion. However, for RN, what would this achieve? Remember, RN’s goal is to prove to the electorate that it can govern in order for Marine Le Pen to gain voters’ trust and win the presidency in 2027. Winning a no-confidence motion will likely only result in Macron seeking another candidate and resuming the process again.

So we see the potential for PM Barnier lasting longer than many assume. An agreed budget may fall short of EU requirements but a disagreement with Brussels may be the preferred option for now over the risk of PM Barnier being removed at this stage. The OAT bond market likely already is priced for France deficits remaining higher for longer given the gridlock and therefore a budget deal that delays the deficit getting back to the 3% limit is unlikely to prompt much negative reaction. The OAT/Bund spread remains 20bps wider than when the political uncertainty began. Indeed, if a no-confidence motion is avoided we could see some moderate spread narrowing.

The euro on a trade-weighted basis fell by 1% as the OAT/Bund spread widened out on Macron’s announcement of an election but the FX impact faded quickly and EUR EER has since advanced 1.5%. A successful no-confidence motion would likely spark some FX impact but we see this as unlikely for now. A more active Fed in cutting rates will be the more dominant impact, helping to support EUR over the coming months.

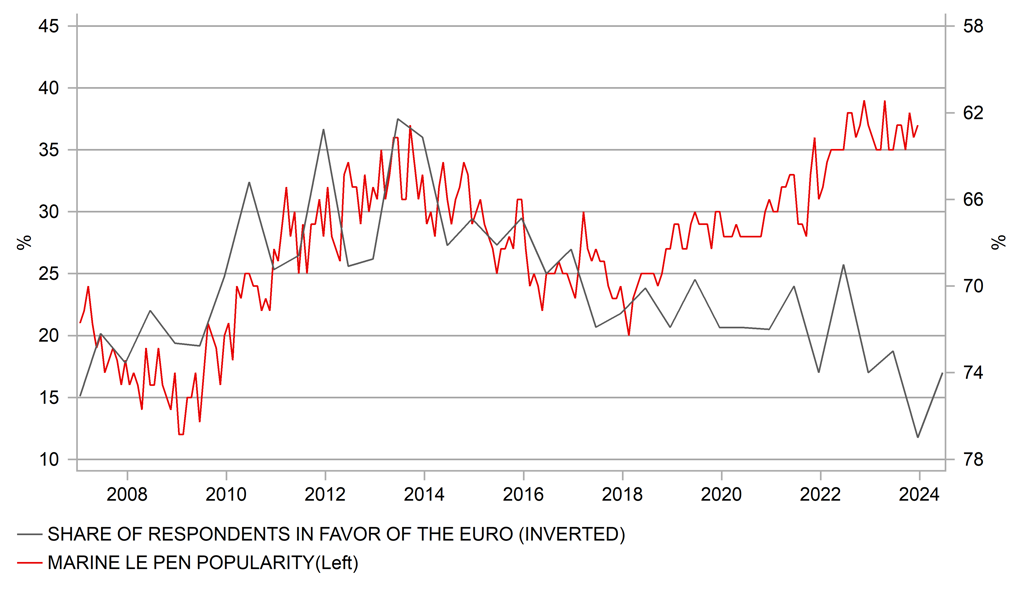

STRONG VOTER SUPPORT – FOR LE PEN & FOR EURO

Source: Macrobond

CAC 40 UNDERPERFORMANCE HAS NO EUR IMPACT

Source: Bloomberg, Macrobond & MUFG GMR

EUR/USD: Fed to play catch up with cautious ECB easing

The EUR has continued to trade at stronger levels against the USD after breaking out above the 1.0500 to 1.1000 trading range in the second half of August. The pair is currently on track to close above the 1.1000-level for the third consecutive week. It is the longest run of higher closes since late July/early August of last year. Recent price action is giving us more confidence that the adjustment higher for EUR/USD will prove more sustainable. In our latest monthly FX Outlook report (click here) we revised higher our forecasts for EUR/USD for the next couple of quarters to indicate that we now expect the pair to continue to trade within a higher range between 1.1000 and 1.1500 heading into year end.

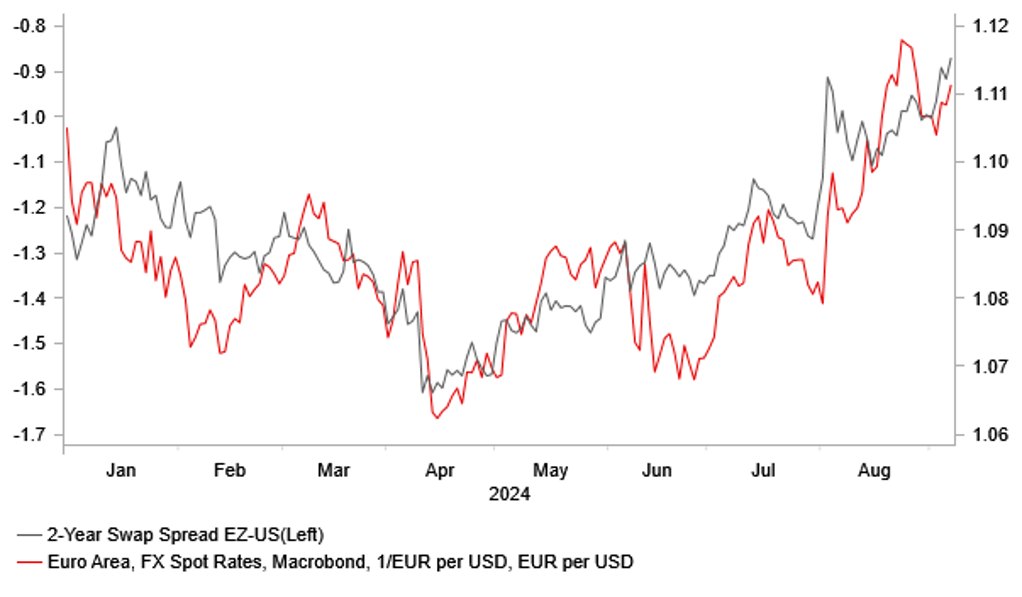

The main driver for the recent adjustment higher for EUR/USD has been building market expectations for more aggressive Fed easing as they plan to start cutting rates later this month. Yields in the US have fallen by more than in the euro-zone over the past month. The two-year US government bond yield has fallen by 28bps compared to only 13bps for the German equivalent. US rate market participants have become more confident that the Fed will play catch up with the ECB by cutting rates at all three remaining FOMC meetings this year by a cumulative total of around 111bps. It reflects expectations as well that at least one larger 50bps cut will be delivered to reflect the risk that the Fed feels it has fallen behind the curve. In contrast, the euro-zone rate market still expects the ECB to remain more cautious when lowering rates. There are only around 63bps of ECB rate cuts priced in by the end of this year.

We expect the ECB to cut rate for the second time in the current easing cycle in the week ahead by 25bps lowering the policy rate to 3.50%. It follows the decision to leave rate on hold at the last meeting in July. The decision to cut rate again next week should be supported by the updated ECB staff forecasts that could be revised modestly lower both for inflation and growth in the euro-zone. The previous ECB staff forecasts from June for inflation were set at 2.5% in 2024, 2.2% in 2025 and 1.9% in 2026, while the GDP forecasts were set at 0.9% in 2024, 1.4% in 2025 and 1.6% in 2026. However, the forecast revisions are unlikely to be sufficient on their own to encourage the ECB to speed up the pace of rate cuts. The ECB will have been encouraged by the release recently of their latest negotiated wage data for the euro-zone that revealed a sharper slowdown to 3.6% in Q2 from 4.7% in Q1. ECB Chief Economist Lane stated the next policy meeting in October, it remains more likely that the ECB will wait until December to deliver the third rate cut in the cycle when they will again have access to updated ECB staff forecasts. We do not expect the ECB to speed up rate cut plans in response to the faster pace of Fed easing. For the ECB to speed up the pace of rate cuts, it will require clearer evidence that inflation is falling back more quickly to their target and euro-zone economy/labour market is much weaker than expected. After returning to modest growth in the first half of this year, we expect the economic recovery to continue through the rest of this year supported by rising real disposable income as the negative energy price shock continues to ease. The disappointing performance of Germany’s economy does though remain one area of concern. Economic growth contracted again in Q2 for the third time out of last five quarters.

EXPECTATIONS FOR FASTER FED CUTS LIFT EUR/USD

Source: Bloomberg, Macrobond & MUFG GMR

REVERSAL OF NEGATIVE ENERGY PRICE SHOCK

Source: Bloomberg, Macrobond & MUFG GMR

In these circumstances, we are not expecting next week’s ECB policy to have a significant impact on the performance of EUR/USD assuming that the ECB’s updated communication remains consistent with further gradual policy easing. President Lagarde would have to signal more strongly that back to back rate cuts could be delivered in October to trigger a bigger dovish repricing for the euro-zone rate market and trigger a deeper pullback for EUR/USD back below support at the 1.1000-level. Without a significant dovish policy surprise from the ECB, the performance EUR/USD is likely to remain driven more by expectations for Fed policy in the near-term.

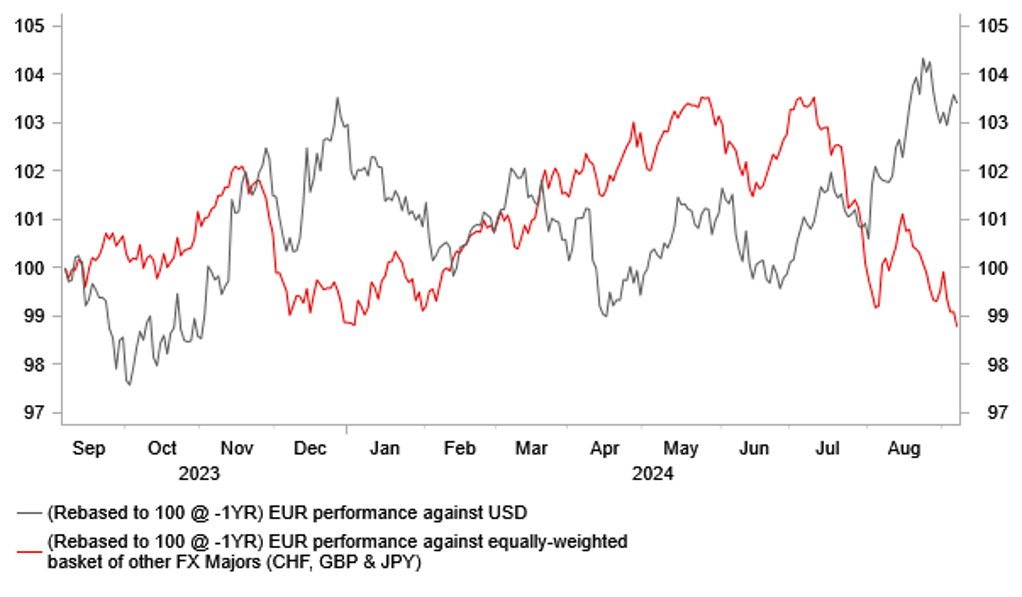

DIVERGING PERFORMANCE OF EUR VS. FX MAJORS

Source: Bloomberg, Macrobond & MUFG GMR

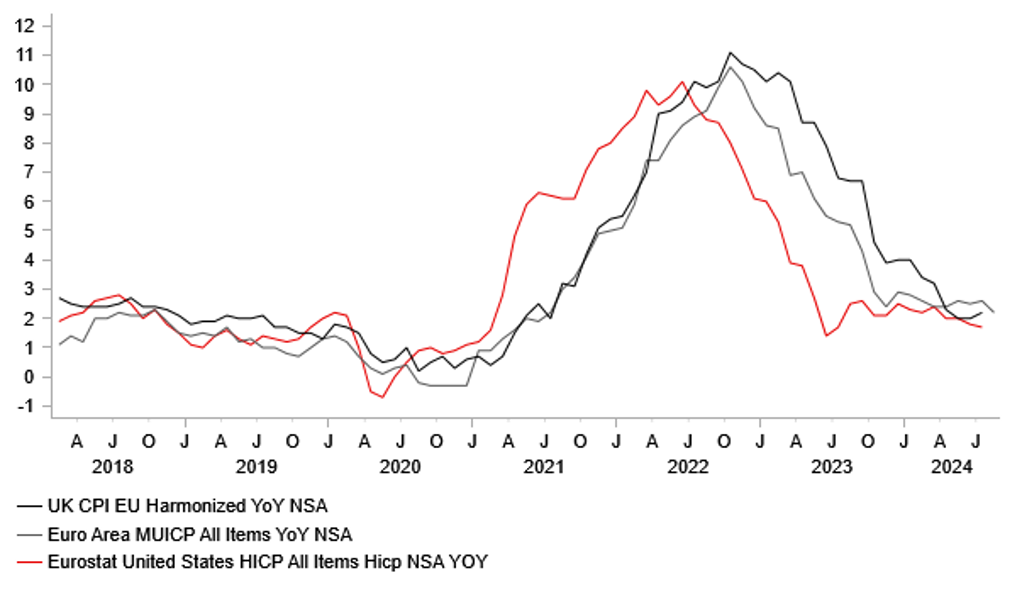

INFLATION IN EUROPE HAS FOLLOWED US WITH A LAG

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Ccy |

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

JPY |

09/09/2024 |

00:50 |

GDP SA QoQ |

2Q F |

0.8% |

0.8% |

!! |

|

JPY |

09/09/2024 |

00:50 |

BoP Current Account Balance |

Jul |

¥2508.1b |

¥1533.5b |

!! |

|

CNY |

09/09/2024 |

02:30 |

CPI YoY |

Aug |

0.7% |

0.5% |

!! |

|

EUR |

09/09/2024 |

09:30 |

Sentix Investor Confidence |

Sep |

-- |

- 13.9 |

!! |

|

CNY |

09/10/2024 |

Tbc |

Exports YoY |

Aug |

6.8% |

7.0% |

!! |

|

CNY |

09/10/2024 |

Tbc |

Imports YoY |

Aug |

2.5% |

7.2% |

!! |

|

NOK |

09/10/2024 |

07:00 |

CPI YoY |

Aug |

-- |

2.8% |

!! |

|

EUR |

09/10/2024 |

07:00 |

Germany CPI YoY |

Aug F |

-- |

1.9% |

!! |

|

SEK |

09/10/2024 |

07:00 |

GDP Indicator SA MoM |

Jul |

-- |

0.9% |

!! |

|

GBP |

09/10/2024 |

07:00 |

Average Weekly Earnings 3M/YoY |

Jul |

-- |

4.5% |

!!! |

|

GBP |

09/10/2024 |

07:00 |

Employment Change 3M/3M |

Jul |

-- |

97k |

!! |

|

USD |

09/10/2024 |

11:00 |

NFIB Small Business Optimism |

Aug |

-- |

93.7 |

!! |

|

CAD |

09/10/2024 |

13:25 |

BoC Governor Macklem speaks |

!! |

|||

|

USD |

09/11/2024 |

02:00 |

Presidential Debate (Harris vs. Trump) |

|

|

|

!!! |

|

GBP |

09/11/2024 |

07:00 |

Monthly GDP (MoM) |

Jul |

-- |

0.0% |

!!! |

|

USD |

09/11/2024 |

13:30 |

CPI MoM |

Aug |

0.2% |

0.2% |

!!! |

|

GBP |

09/12/2024 |

00:01 |

RICS House Price Balance |

Aug |

-- |

- 0.19 |

!! |

|

SEK |

09/12/2024 |

07:00 |

CPI YoY |

Aug |

-- |

2.6% |

!! |

|

EUR |

09/12/2024 |

13:15 |

ECB Deposit Facility Rate |

Sep-12 |

-- |

3.75% |

!!! |

|

USD |

09/12/2024 |

13:30 |

PPI Ex Food and Energy MoM |

Aug |

0.2% |

0.0% |

!! |

|

USD |

09/12/2024 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

EUR |

09/12/2024 |

13:45 |

ECB President Lagarde Press Conference |

!!! |

|||

|

JPY |

09/13/2024 |

05:30 |

Industrial Production MoM |

Jul F |

-- |

2.8% |

!! |

|

EUR |

09/13/2024 |

07:45 |

France CPI YoY |

Aug F |

-- |

1.9% |

!! |

|

EUR |

09/13/2024 |

09:30 |

ECB's Rehn Speaks |

!! |

|||

|

EUR |

09/13/2024 |

10:00 |

Industrial Production SA MoM |

Jul |

-- |

-0.1% |

!! |

|

USD |

09/13/2024 |

13:30 |

Import Price Index MoM |

Aug |

-- |

0.1% |

!! |

|

USD |

09/13/2024 |

15:00 |

U. of Mich. Sentiment |

Sep P |

-- |

67.9 |

!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- The main event in the week ahead will be the ECB’s latest policy meeting. The ECB are expected to lower rates by 25bps to 3.75%. It would be the second rate cut in the current easing cycle after they left rates on hold in July. The euro-zone rate market is already fully pricing in a 25bps rate cut in the week ahead so market participants will be more closely watching the ECB’s updated policy guidance to assess how likely they are to stick to the gradual quarterly pace of easing. The euro-zone rate market is currently pricing in around a 50:50 probability of a third rate cut as soon as at the following meeting in October. While the ECB are unlikely to rule out cutting rates again as soon as next month, we expect the ECB to signal that they are more likely to wait until at least October or December. Assuming that the ECB cuts rates next week, it will have only cut rates at policy meetings alongside updated ECB staff forecasts which at the margin favours December or October for the timing of the third rate cut.

- The first Presidential debate between new Democratic candidate Kamala Harris and Republican candidate Donald Trump is scheduled to take place at 9pm EDT on 10th The Presidential race is closely balanced heading into the first debate.

- The main economic data release in the week ahead will be the release of the US CPI report for August. There has been a clear slowdown in core inflation over the last four months to July compared to in the first three months of this year. Core inflation increased by an annualized rate of around 2.4% over the last four months compared to an annualized rate of 4.8% in Q1. Unless there is a significant upside surprise in the week ahead, the report is unlikely to significantly alter expectations for the Fed to begin cutting rates by 25bps at the September FOMC meeting.

- The other main economic data release in the week ahead will be the latest labour market report from the UK. The report is expected to provide evidence that the pace of wage growth is slowing. The BoE is expecting regular private sector AWE growth to slow further to 4.8% in Q3 from 5.2% in Q2. The labour market report would have to be significantly weaker than expected to encourage UK rate market participants to bring forward the expected timing of the next BoE rate cut from November to September. After a very close vote to begin cutting rates in August, back to back rate cuts in September appears unlikely.