To read the full report, please download PDF.

USD to consolidate at weaker levels

FX View:

The US dollar is finishing the week at weaker levels helped by increased optimism in Europe after a deal was reached in Germany over fiscal spending plans which should mean a successful vote in the Bundestag on Tuesday. That along with a press conference in China on Monday, which is focused on policy support measures to boost consumption should help support global growth optimism and keep the dollar on a weaker footing. However, we have a busy week of central bank meetings next week with the BoJ, FOMC, Riksbank, SNB and BoE all meeting on Wednesday and Thursday. All are expected to remain on hold bar the SNB that should follow the ECB and cut by 25bps. Confirmation of a successful passing of legislation on German fiscal spending is unlikely to have much impact with a positive outcome priced and hence Trump trade policies and dovish/hawkish interpretations from central bank communications will drive the FX markets. But possible China announcements and German developments may help consolidate the dollar at these weaker levels for now.

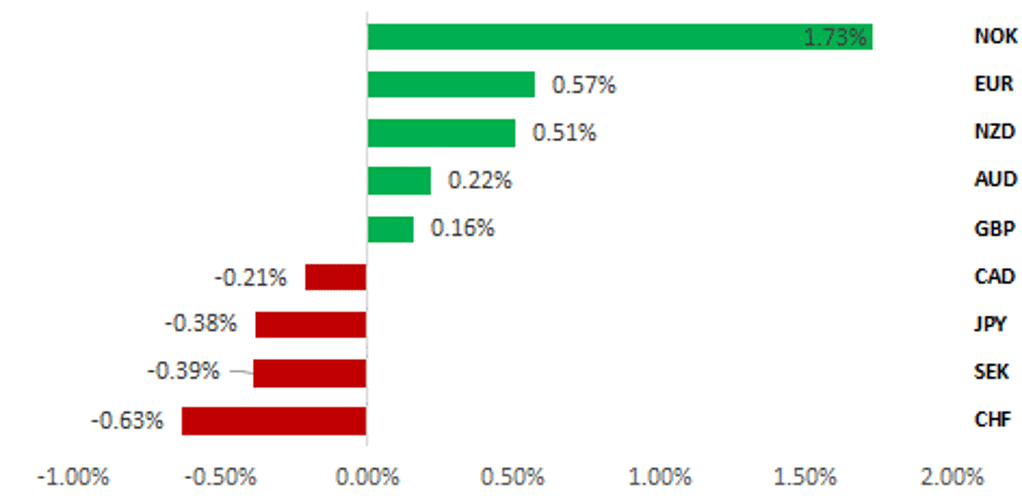

MIXED USD PERFORMANCE BUT LOW-YIELDERS UNDERPERFORM

Source: Bloomberg, 13.35 GMT, 14th March 2025 (Weekly % Change vs. USD

Trade Ideas:

We are maintaining our short EUR/JPY trade idea, and recommending a new long USD/SEK trade idea.

JPY Flows:

The monthly MoF International Transactions in Securities was released last week and revealed a rebound in foreign bond buying with Japan Trusts the biggest buyers. After record buying of foreign equities by Japan Investment Trusts in January, further more modest buying took place in February

Short Term Fair Value Modelling:

This week, we monitor the relationships between spot prices and fair values in our short-term regression models. Recently, our models have identified significant divergences between spot prices and fair values for USD/JPY, GBP/USD, and EUR/USD.

FX Views

JPY: BoJ to confirm on track to hike again

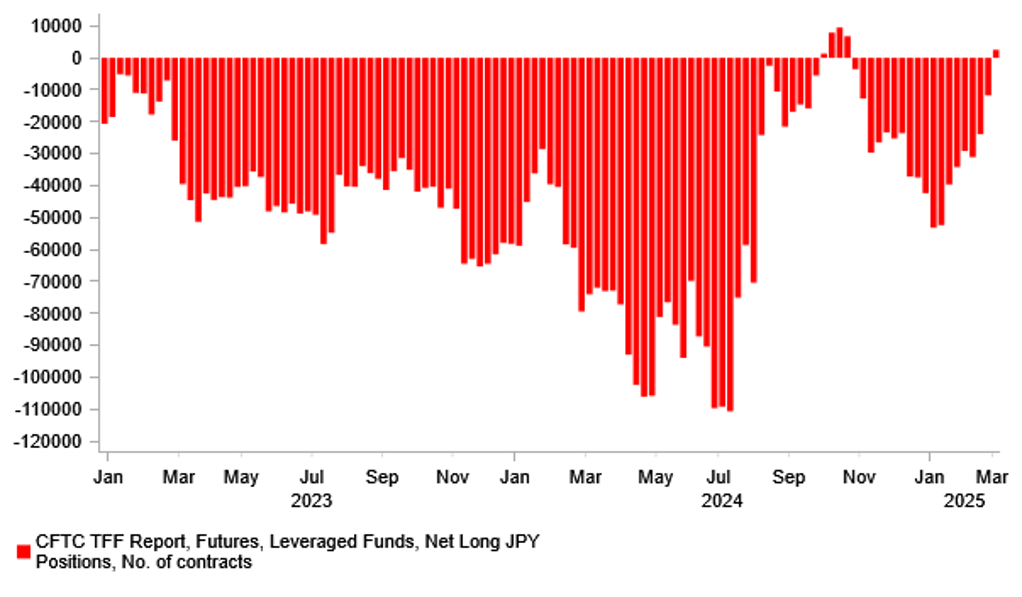

USD/JPY has been on a steady sustained decline since hitting an intra-day high in January (158.87 on 10th) and on Tuesday hit an intra-day low of the year of 146.54, a move close to an 8% drop that looks to have been helped by a notable shift in short-term speculative positioning. The weekly CFTC data shows a swing in January from the largest short JPY positioning amongst Leveraged Funds since July last year to the latest data which shows the first outright long JPY position since October last year. The reversal in that strong downward momentum this week does suggest to us that positioning may have become crowded for now. The yen is the second worst performing G10 currency this week. There is still evidence of co-movement with short-term US yield moves with the 2-year UST bond yield currently up 14bps from the intra-day year-to-date low on Tuesday when USD/JPY also hit the intra-day year-to-date low. Still, USD/JPY is sharply higher today on a day of limited US yield moves and points to a squeeze in long JPY positions into the end of the week. A more favourable turn in risk appetite has also encouraged this JPY sell-off with China set to hold a press conference on Monday focusing on policies to support consumption and the decision of Senate Minority leader Chuck Schumer to support the GOP’s continuing resolution bill to provide a 6mth extension to fund government spending which therefore avoids a potential damaging government shutdown from tonight.

The depreciation of the yen was likely reinforced by the emergence of renewed political risks. The Asahi newspaper reported last night that PM Ishiba had distributed gift vouchers (JPY 100k) to fifteen new LDP members of parliament that runs close to the scandal that hit the LDP previously over campaign funds being passed to factions within the LDP. PM Ishiba today denied any wrongdoing but apologised for any confusion. Public support for PM Ishiba dropped to 40%, the lowest since he took office in October according to a Nikkei poll published last month. One Upper House LDP member has called for PM Ishiba to resign once the budget has been passed.

The key focus for JPY next week will come on Wednesday with the BoJ policy meeting followed later in the day by the FOMC policy announcement. The market is fully priced for no change in policy but recent speeches on the topic of the ‘terminal rate’ means investors will be focused on any signal from Governor Ueda on a potential hint that the terminal rate could be higher. A Bloomberg survey this week (52 respondents) indicated 1.25% as the median level for the terminal rate with a range of 0.50% to 2.50%. But the survey also indicated concerns over the BoJ potentially being too cautious in hiking with 39% seeing a “real risk” of the BoJ falling behind the curve and a further 27% saying it was difficult to tell. 55% believed it was a “high” or “very high” hurdle for the BoJ to buy JGBs if yields increased rapidly. Deputy Governor Uchida in a speech on 5th March stated that the BoJ didn’t know the terminal rate and that it would not be good communication for the BoJ to cite a level anyway. Policy Board Member Hajime Takata in February spoke of the range for the neutral rate being very wide and concluded in a speech that conditions are falling into place that would require the BoJ to return to “policy conduct that is in line with what is seen in normal times”. That speech helped lift market expectations of the terminal rate which has now gone from around 0.90% at the end of 2024 to close to 1.20% now.

LEVERAGED FUNDS TURN LONG JPY

Source: Bloomberg, Macrobond & MUFG GMR

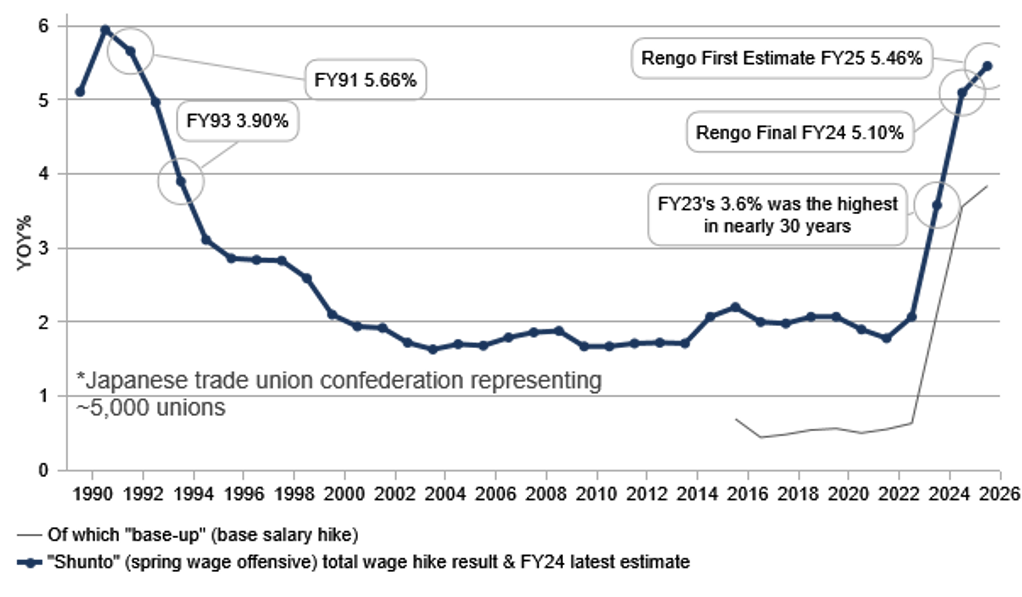

RENGO FY25 FIRST ESTIMATE HIGHEST SINCE FY91

Source: Bloomberg, Macrobond & MUFG GMR

We would expect this adjustment in the pricing of the terminal rate to be maintained following the BoJ meeting. While we doubt Governor Ueda will dwell on the topic of the terminal rate he will likely confirm progress continues to be made in reaching the inflation goal. The Rengo wage announcement today is a very important part of this BoJ view being maintained. The ‘shunto’ wage negotiation by Rengo came in at 5.46% with a base pay of 3.84% above the Bloomberg consensus (5.1% & 3.4%) and will clear Governor Ueda to signal further hikes ahead. We expect the next 25bp hike in July but there is a risk of it coming sooner, in June.

The Nikkei reported this week that the Government Pension Investment Fund would not be changing its asset allocation in conclusion to its latest 5-year review, which means an even 25% split will be maintained across domestic and foreign bonds and equities. There had been speculation given the rise in JGB yields that the GPIF would increase its allocation to JGBs. With GPIF assets now at JPY 260trn (USD 1.7trn) small shifts in allocation would be meaningful. Still, scope remains for increased JGB buying with a +/-7% range from the 25% midpoint.

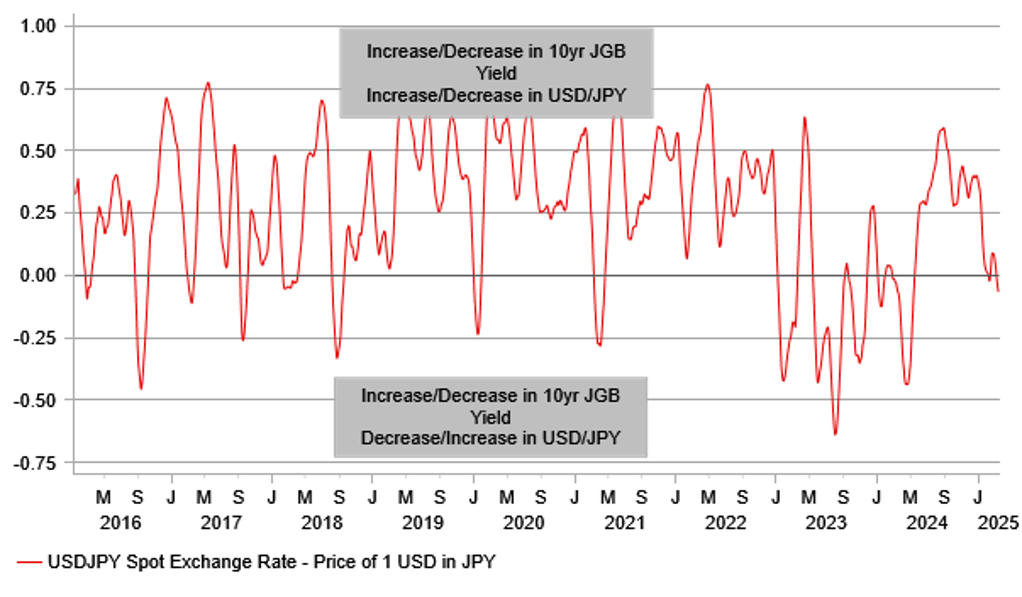

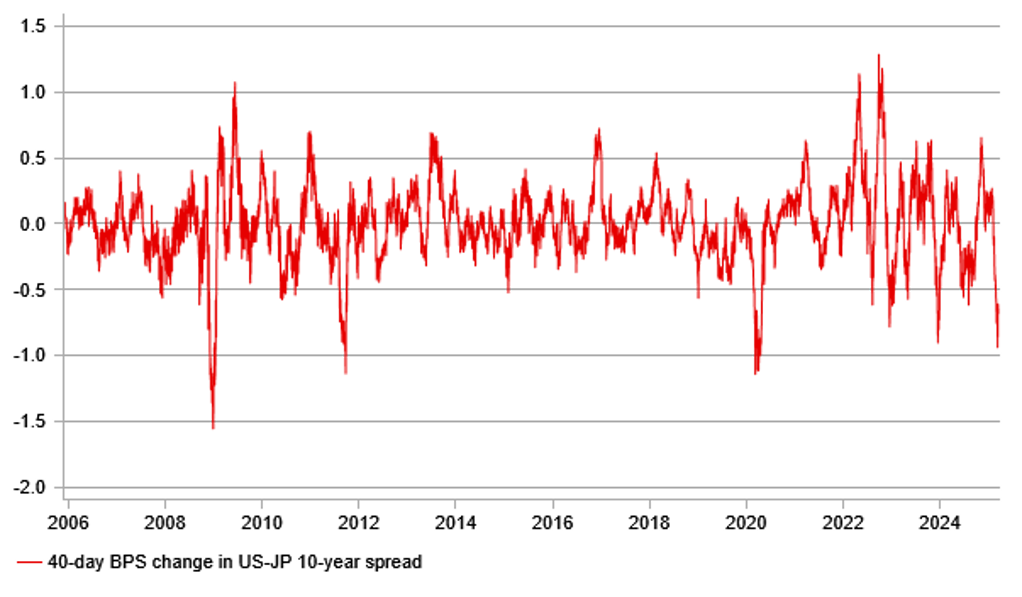

The chart below highlights the reasserting negative correlation between USD/JPY and the 10-year JGB yield that suggests the shift higher in yields fuelled by the gradual grind higher in the estimate of the terminal rate has influenced USD/JPY lower this year. The more usual positive correlation reflects the influence of US Treasury yields on JGBs and hence higher JGB yields (driven by USTs) lifts USD/JPY. The shift this year therefore is also reflected in the sharp narrowing of the 10-year US-JP spread. The 10-year US-JP spread has narrowed by close to 100bps in a 40-day period since 13th Jan – one of the largest declines since the GFC (below).

Barring a shock surprise communication from the FOMC, we expect JGB yields to be driven by the outcome of the BoJ meeting with a clear message that the BoJ is on track to hike again later in the year with encouragement provided by the strong wage growth this week. That will support JGB yields and the yen. Less favourable risk conditions post reciprocal tariff day on 2nd April is likely another factor that will curtail yen selling going forward. Our bias remains selling USD/JPY on rallies.

NEGATIVE JGB USD/JPY CORRELATION RETURNING

Source: Bloomberg, Macrobond & MUFG GMR

LARGEST 40-DAY DROP IN US-JP SPEAD SINCE COVID

Source: Bloomberg, Macrobond & MUFG GMR

GBP: BoE to stick to plans for quarterly rate cuts as UK inflation picks up

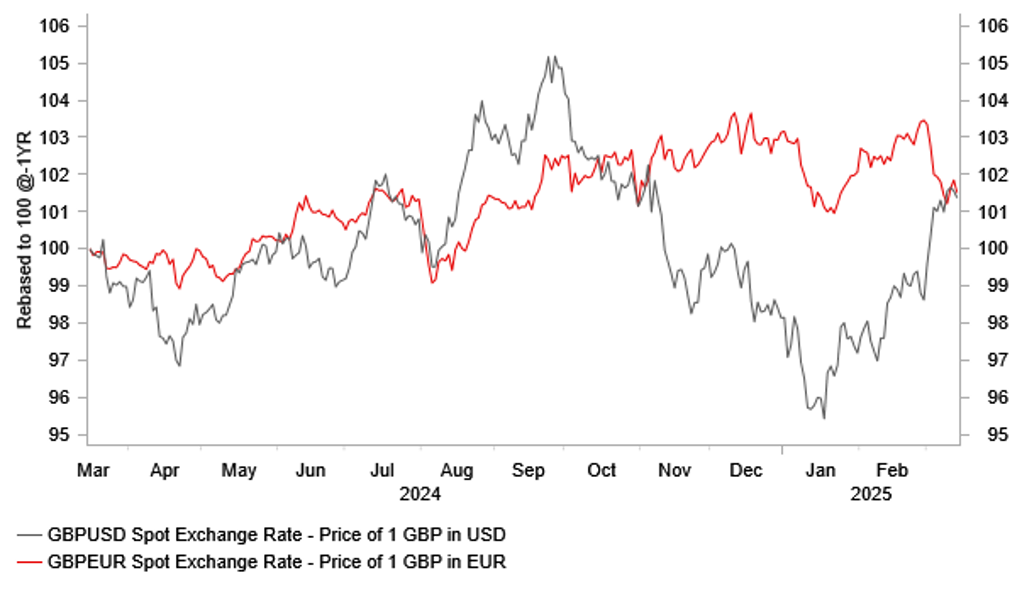

The GBP has outperformed alongside other European currencies this month benefitting from the significant improvement in investor sentiment towards the region. It has helped to lift cable back up towards the 1.3000-level for the first time since last year’s US election. In contrast, the GBP has weakened modestly against the EUR lifting EUR/GBP back above the 0.8400-level for the second time this year. The EUR is expected to benefit more than the GBP from Germany’s plans for looser fiscal policy (click here). The last time EUR/GBP rose above 0.8400 in January it was driven more by negative sentiment towards the GBP reflecting concerns over UK government debt.

Market participants now expect monetary policies between the ECB and BoE to diverge less going forward which has helped to narrow yield spreads in favour of a stronger EUR. At the ECB’s last policy meeting (click here) they left the door open for further modest rate cuts with the policy rate now closer to the neutral estimate put forward by President Lagarde between 1.75% and 2.25%. Based on our assumption that legislation is passed next week on Tuesday to boost fiscal policy in Germany, it will ease pressure on the ECB to lower rates below neutral. The main risk to that view would be a much bigger hit to growth in Europe from President Trump’s upcoming plans for trade tariffs in early April. The EU’s decision to quickly retaliate by imposing tariff hikes from next month on EUR26 billion of US imports in response to US tariff hikes on steel and aluminium imports has angered President Trump, and he has since threatened to impose 200% tariffs on over USD10 billion of alcohol imports from the EU. In contrast, the Trump administration has praised the UK government for their decision not to retaliate. It will further encourage market expectations that the UK economy will not be hit as hard by further tariff hikes in the coming months.

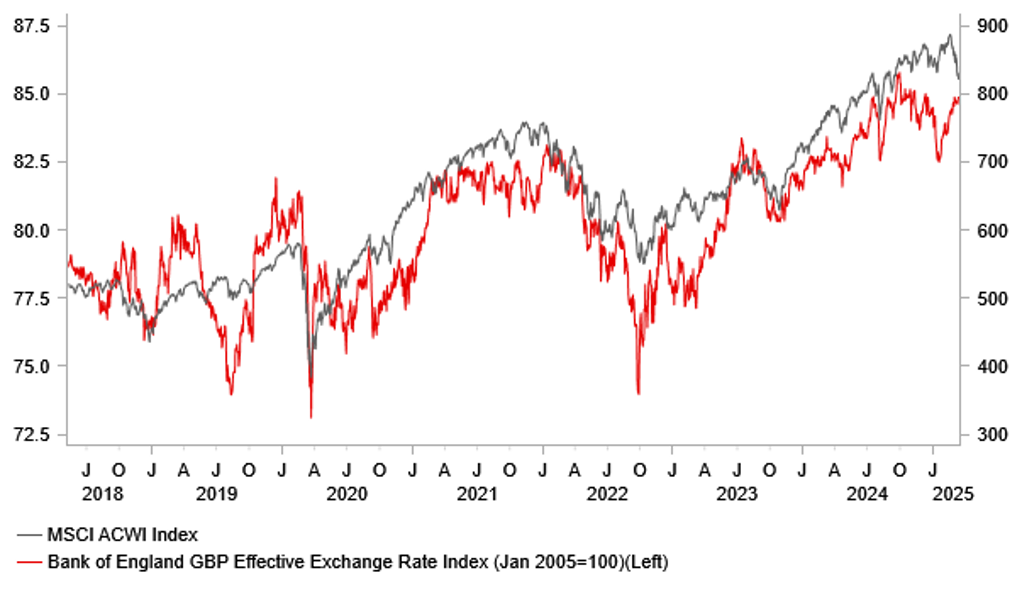

Market expectations for BoE policy have recently been relatively more stable than for the ECB. The UK rate market is still expecting the BoE to stick to the current quarterly pace of rate cuts by delivering the next rate cut in May (17bps of cuts priced in) and then again in August (38bps of cuts priced in). However, there is less confidence that rates will fall further below 4.00% by the end of this year. It is helping to keep yields in the UK at higher levels than on offer in other major economies providing support for the GBP. The BoE holds their latest policy meeting next week. Ahead of that meeting UK economic data has been improving with the exception of today’s softer UK GDP report for January. Overall it points to strengthening growth momentum since late year. At the same time the slowdown in services inflation and wage growth remains frustratingly slow. It will become more uncomfortable for the BoE to keep cutting rates heading into the summer when inflation is expected to temporarily pick up towards 4.0%. Overall, the GBP remains attractive. A deeper sell-off for global equity markets that undermines financial stability poses the main downside risk for the GBP.

GBP STRENGTHENS VS. USD BUT SOFTER VS. EUR

Source: Bloomberg, Macrobond & MUFG GMR

DEEPER EQUITY SELL-OFF COULD WEIGH ON GBP

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Ccy |

Date |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

CNY |

17/03/2025 |

02:00 |

Industrial Production YTD YoY |

Feb |

5.3% |

-- |

!! |

|

CNY |

17/03/2025 |

02:00 |

Retail Sales YTD YoY |

Feb |

3.8% |

-- |

!! |

|

CNY |

17/03/2025 |

02:00 |

Fixed Assets Ex Rural YTD YoY |

Feb |

3.2% |

-- |

!! |

|

USD |

17/03/2025 |

12:30 |

Retail Sales Advance MoM |

Feb |

0.7% |

-0.9% |

!!! |

|

EUR |

18/03/2025 |

10:00 |

Trade Balance SA |

Jan |

-- |

14.6b |

!! |

|

USD |

18/03/2025 |

12:30 |

Housing Starts |

Feb |

1383k |

1366k |

!! |

|

CAD |

18/03/2025 |

12:30 |

CPI YoY |

Feb |

-- |

1.9% |

!!! |

|

USD |

18/03/2025 |

12:30 |

Import Price Index MoM |

Feb |

-0.1% |

0.3% |

!! |

|

USD |

18/03/2025 |

13:15 |

Industrial Production MoM |

Feb |

0.3% |

0.5% |

!! |

|

JPY |

18/03/2025 |

23:50 |

Trade Balance |

Feb |

¥722.8b |

-¥2758.8b |

!! |

|

JPY |

19/03/2025 |

Tbc |

BOJ Target Rate |

0.50% |

0.50% |

!!! |

|

|

JPY |

19/03/2025 |

04:30 |

Industrial Production MoM |

Jan F |

-- |

-1.1% |

!! |

|

EUR |

19/03/2025 |

10:00 |

Labour Costs YoY |

4Q |

-- |

4.6% |

!!! |

|

EUR |

19/03/2025 |

10:00 |

CPI YoY |

Feb F |

-- |

2.4% |

!! |

|

EUR |

19/03/2025 |

10:45 |

ECB's Villeroy speaks |

!! |

|||

|

USD |

19/03/2025 |

18:00 |

FOMC Rate Decision (Upper Bound) |

4.50% |

4.50% |

!!! |

|

|

USD |

19/03/2025 |

21:45 |

GDP SA QoQ |

4Q |

0.4% |

-1.0% |

!! |

|

AUD |

20/03/2025 |

00:30 |

Employment Change |

Feb |

28.0k |

44.0k |

!! |

|

GBP |

20/03/2025 |

07:00 |

Average Weekly Earnings 3M/YoY |

Jan |

-- |

6.0% |

!!! |

|

GBP |

20/03/2025 |

07:00 |

Employment Change 3M/3M |

Jan |

-- |

107k |

!! |

|

CHF |

20/03/2025 |

08:30 |

SNB Policy Rate |

0.25% |

0.5% |

!!! |

|

|

SEK |

20/03/2025 |

08:30 |

Riksbank Policy Rate |

2.25% |

2.25% |

!!! |

|

|

CHF |

20/03/2025 |

09:00 |

SNB's Schlegel Speaks |

!! |

|||

|

GBP |

20/03/2025 |

12:00 |

Bank of England Bank Rate |

4.50% |

4.50% |

!!! |

|

|

EUR |

20/03/2025 |

12:00 |

ECB's Lane Speaks |

!! |

|||

|

USD |

20/03/2025 |

12:30 |

Current Account Balance |

4Q |

-- |

-$310.9b |

!! |

|

USD |

20/03/2025 |

12:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

JPY |

20/03/2025 |

23:30 |

Natl CPI YoY |

Feb |

3.6% |

4.0% |

!!! |

|

GBP |

21/03/2025 |

07:00 |

Public Sector Net Borrowing |

Feb |

-- |

-15.4b |

!! |

|

CAD |

21/03/2025 |

12:30 |

Retail Sales MoM |

Jan |

-- |

2.5% |

!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- There is a busy schedule of central bank meetings in the week ahead. The BoJ and the Fed hold their latest policy meetings on Wednesday followed by the SNB, Riksbank and BoE on Thursday.

- The BoJ are expected to leave their policy rate unchanged at 0.50% after raising rates by a further 25bps at their previous policy meeting in January. The updated policy guidance will be scrutinized closely to assess the likely timing of the next BoJ rate hike. The Japanese rate market is currently pricing in around 7bps of hikes by the following meeting in May and 13bps by the June policy meeting. Recent communication from the BoJ has remained hawkish indicating that further rate hikes will be delivered if the economy evolves in line with their outlook.

- The Fed is expected to leave rates on hold again in the week ahead. Fed Chair Powell reiterated recently that they are in not in a hurry to cut rates again amidst heightened uncertainty over the implementation of President Trump’s policy platform. At the current juncture, we expect only modest changes to the Fed’s growth and inflation forecasts. As a result, the updated DOT plot is likely to be similar to from December still projecting two further rate cuts this year and next.

- The BoE is expected to leave rates on hold at 4.50% following the 25bps rate cut delivered in February. The vote count will attract market attention again after the dovish surprise in February when MPC member Catherine Mann voted for a larger 50bps cut. We still expect the BoE to stick the current quarterly pace of rate cuts and leave the door open next week to another cut in May. Risks are tilted towards more hawkish guidance to reflect concerns over wage growth and stronger activity data recently.