To read the full report, please download PDF.

Yen carry revival on shakier ground

FX View:

The improvement in some of the US economic data – the retail sales data in particular – has helped ease fears over a hard-landing of the US economy that has reduced Fed rate cut expectations and helped reignite yen selling. We are sceptical of this rebound in USD/JPY and yen crosses will prove lasting. A 20-big figure drop in USD/JPY is hard to ignore – it’s the biggest drop (over 18 trading days) since the GFC in October 2008 and this drop will inevitably alter investors’ expectations on future direction and start to alter the behaviour of market participants. The shock of such a sudden drop will likely increase appetite for yen buying at weaker levels as appetite for hedging yen upside exposure increases. We also see scope for EUR and GBP upside versus the dollar and this week also assess the impact in the past from Jackson Hole speeches by Fed Chairs. We see evidence of a bigger Jackson Hole impact in years when the policy cycle is turning.

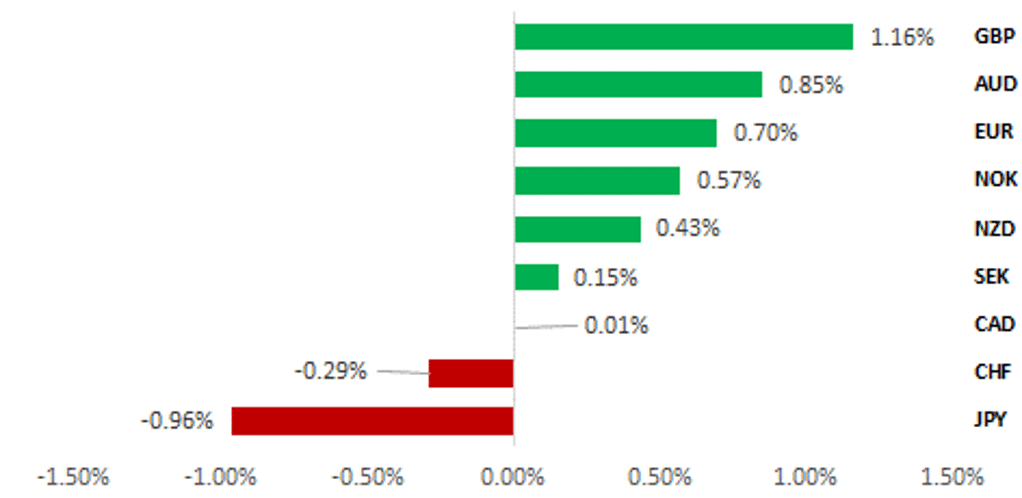

RISK-ON TRADING UNDERMINES JPY AND CHF

Source: Bloomberg, 13:00 BST, 16th August 2024 (Weekly % Change vs. USD)

Trade Ideas:

We are maintaining a short NZD/CAD trade recommendation.

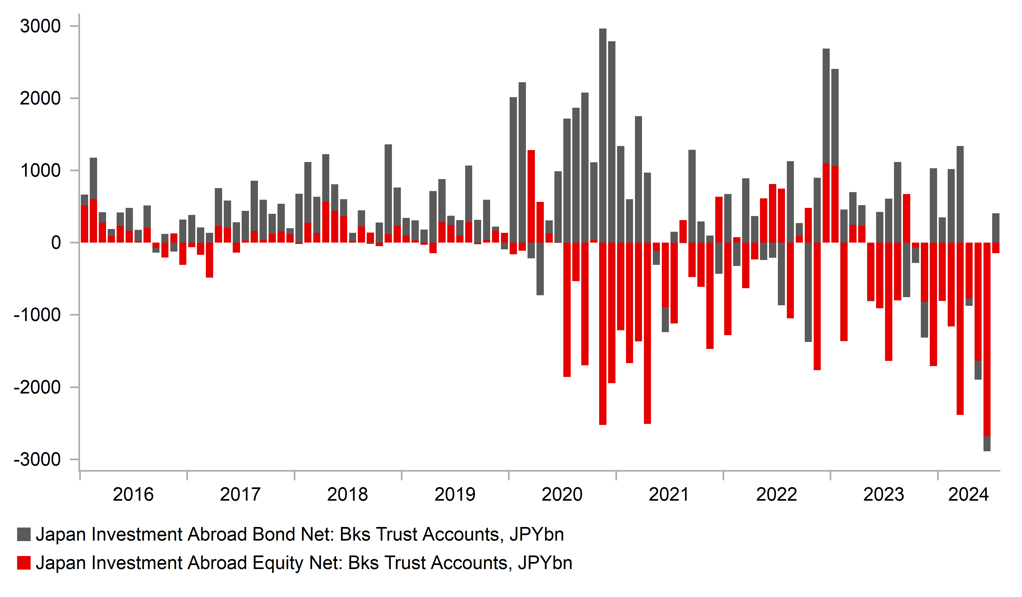

JPY Portfolio Flows:

The International Transactions in Securities data was released last week for the month of July and revealed selling of foreign bonds for the second month which was the largest two-month drop since October 2022. Japanese banks were the main sellers possibly locking in profits as yields fell.

Does Jackson Hole Impact FX Markets?:

Our analysis identifies a bigger market impact both initially (+1 Hr) and for a more sustained period (+1 Day) in EUR/USD and USD/JPY following the Fed Chair’s speech if delivered at a pivotal point in the rate cycle. As the Fed edges closer to cutting rates in September next week’s speech poses downside risks for the USD.

FX Views

JPY: Carry revives but JPY dynamics are changing

Optimism that the US economy will avoid any abrupt slowdown has returned and with that the pricing on firstly an inter-meeting rate cut from the FOMC to secondly a 50bp cut at the next meeting on 18th September have been removed with the market now positioned for a more standard 25bp cut. Our current published forecasts indicate 200bps of rate cuts by the FOMC over the next 12mths as the Fed acts to remove the restrictive monetary stance. Our view is not aggressive when viewed in the context of 200bps merely removing the restrictive stance and returning the policy stance to neutral. 200bps of cuts will take the real policy rate to around the estimated R* of 1.00% as implied by the Fed’s estimate of the neutral nominal policy rate. It also implies more of a soft landing than a hard landing for the US economy. However, as is usually the case going into an economic downturn, the incoming economic data from the US is likely to send mixed signals of the scale of the downturn which we believe means increased financial market volatility like what we have witnessed in the last two weeks. Increased volatility is not conducive to attractive returns on carry trade strategies.

We don’t agree that the substantial volatility on 5th August was triggered by the BoJ policy decisions on 31st July. Of course the 15bp rate hike (expected by us and 30% of the market) and the signal of more to come contributed to the volatility but there were other meaningful events that all combined to fuel the most abrupt correction in carry since the yen depreciation trend began in March 2022. Fed Chair Powell for the first time explicitly put a rate cut on the table for the following meeting, the weak jobs report on 2nd August and even the BoE rate cut on 1st August all played a role in increasing uncertainty over the sustainability of the yen depreciation trend. Even before the 31st July we had had weeks of increased EM FX volatility in popular carry currencies like ZAR and MXN following elections and some disappointing tech earnings results that worsened carry conditions and helped fuel the sudden liquidation.

The scale of the moves on 5th August in particular certainly point to a considerable liquidation of carry positions. The scale of the Japanese equity market move also reflected forced selling, most likely by retail margin traders forced to cover margin. Flow data today released for the week ending 9th August revealed stock and futures selling was most pronounced by foreign investors and domestic individual investors. Domestic institutional investors were buyers and no doubt took advantage to buy at the extreme lows. We suspect that foreign investors returned to the Japanese market this week as yen depreciation extended further. What we do know is that ‘fast-money’ incorporating leveraged speculative flows have liquidated the vast amount of yen shorts. The four-week reduction in yen shorts amongst Leveraged Funds and Institutional Investors was the largest since March 2007 in the latest data to Tuesday of last week. BIS data also indicates an upturn in cross-border lending in yen to entities reporting yen liabilities as a foreign currency. This flow after conversion to higher yielding domestic currencies is often left unhedged in order to take advantage of the cheap financing costs but hedging more of this exposure going forward could well be a factor that will provide support for the yen. The speed of retracement in USD/JPY this week certainly suggests a belief that carry can remain an attractive strategy despite the recent turmoil. We would however argue that while the rate spread will remain attractive, the danger is that we have entered a period of more sustained volatility that will encourage further liquidation of yen carry positions over the coming months.

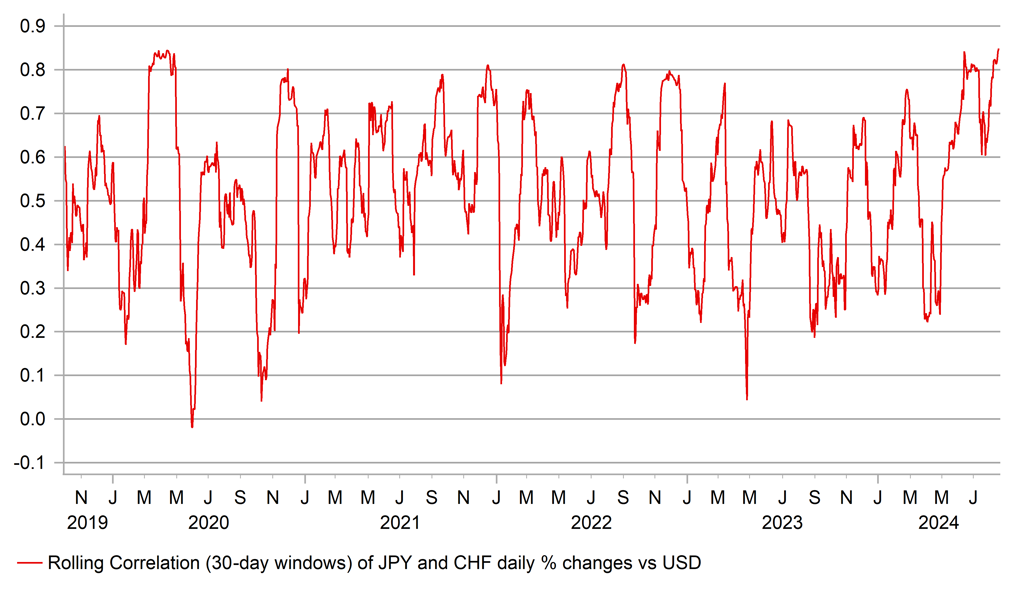

STRONG JPY & CHF CORRELATION

Source: Bloomberg, Macrobond & MUFG GMR

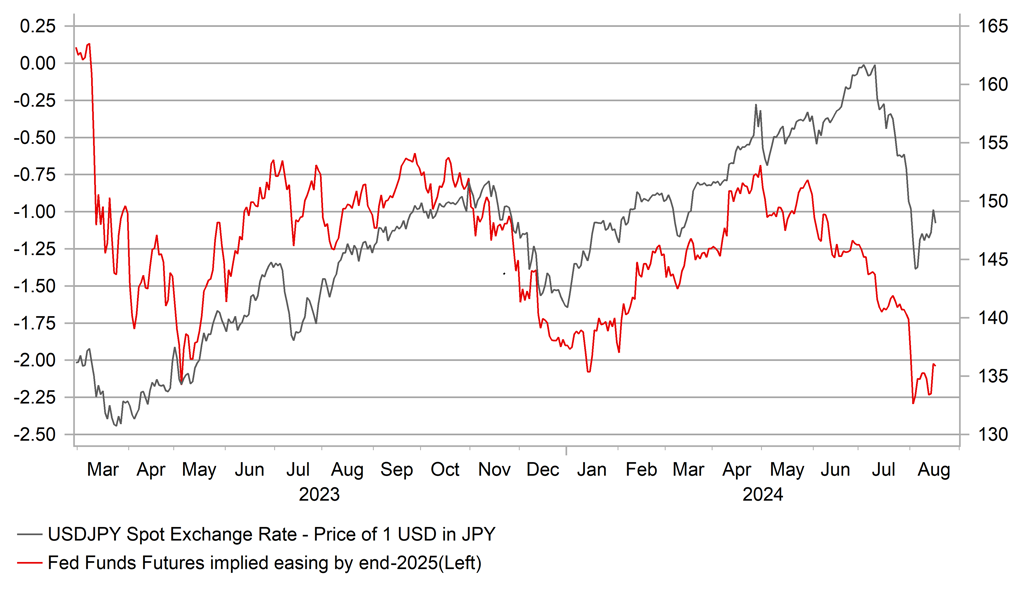

EXPECTED FED EASING BY END-2025 & USD/JPY

Source: MUFG & Global Markets Research

OTC FX retail margin trading positioning data from the Financial Futures Association of Japan is only available to end-June but the data confirms that the retail sector was not heavily positioned and indeed our own internal flows suggest margin retail traders were initially buyers of USD/JPY when USD/JPY dropped on 31st July but then turned sellers before resuming buying this week. With positioning light that segment of the market was probably supportive for USD/JPY at lower levels. In regard to institutional investor flows, we doubt there has been much dramatic change. Lifers were already avoiding foreign bond markets due to high hedging costs. Those costs remain high and feasibly could have lightened up on hedged positions (USD/JPY buyers therefore) given the 20-big figure drop was well beyond any reasonable expectation of near-term FX moves. Trust flows of late already imply liquidation of foreign equity positions while foreign bond purchases have been muted implying a potential shift of capital from that sector back to the Japan domestic markets. Given the FX move, this shift was clearly an opportune move at stronger foreign currency levels.

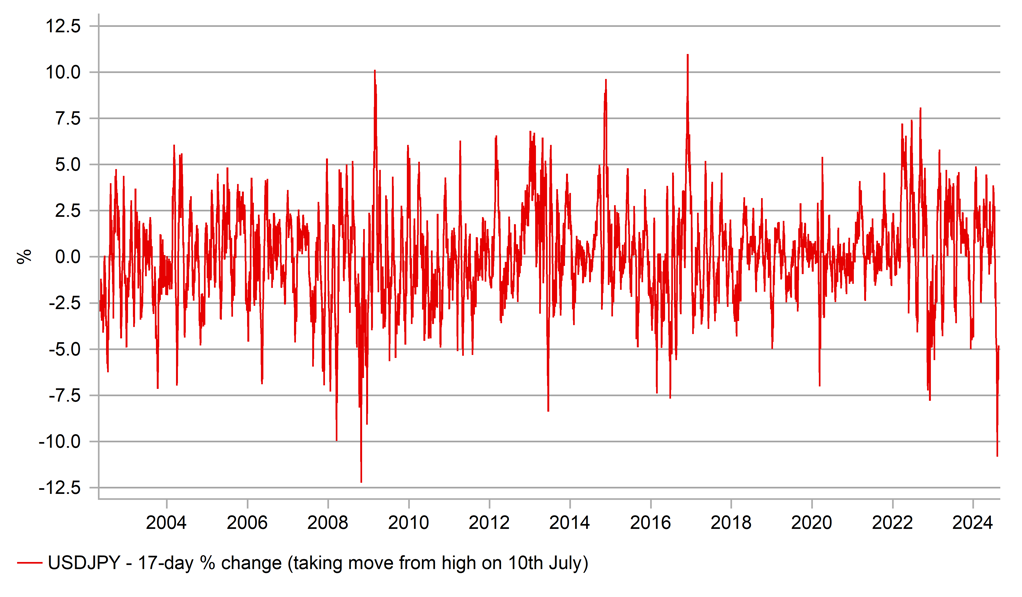

A 20-big figure drop in USD/JPY we believe will have a meaningful impact on expectations of future direction and therefore potentially on behaviour. The last time USD/JPY moved like this recent move (18 days) was in October 2008 during the GFC. Back then USD/JPY rebounded by about 8 big figures and then resumed its decent. The rebound now has fallen short of hitting the 38.2% retracement of the move (at 149.44) and risks remain skewed to the downside. The Fed are to commence rate cuts soon which differentiates this move from previous corrections during the global inflation shock period when declines fully reversed. Behavioural changes likely mean a greater willingness to buy yen at weaker levels skewing the risk to a strengthening bias.

JAPAN TRUSTS HAVE BEEN SELLING FOREIGN ASSETS

Source: Bloomberg, Macrobond & MUFG GMR

18-DAY % DROP IN USD/JPY BIGGEST SINCE GFC

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Softer UK services inflation fails to prevent a GBP recovery

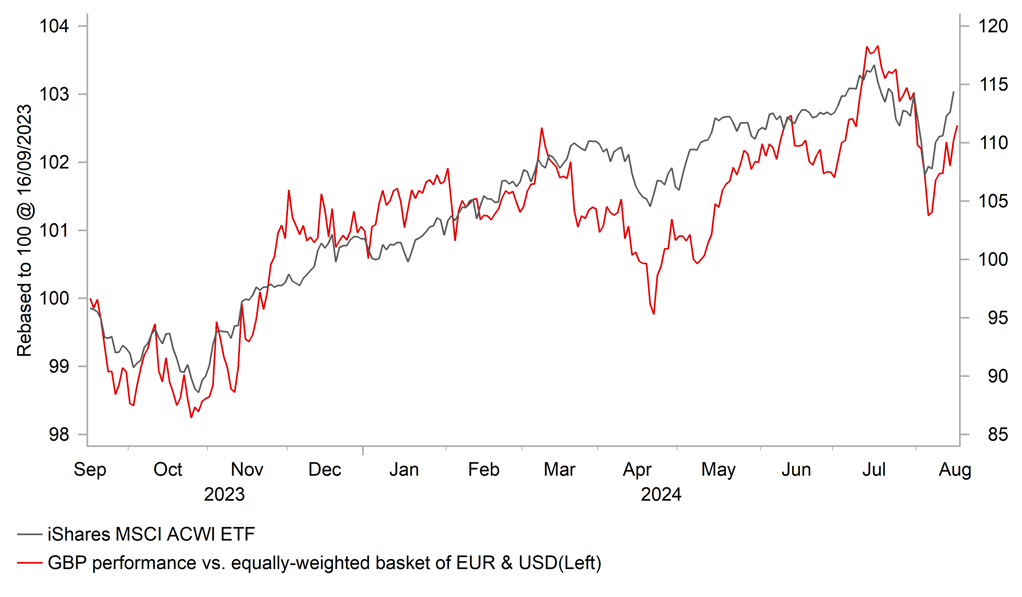

The GBP has been recovering lost ground over the past week following the sell-off in early August. It has resulted in EUR/GBP falling back towards the 0.8500-level after hitting a high of 0.8625 on 8th August. Similarly, cable has risen back up towards the 1.2900-level after bouncing off support provided by the 200-day average at around 1.2660. The GBP has been supported by the improvement in global investor risk sentiment that has boosted demand for higher yielding currencies. After falling by around -7.5% in early August, MSCI’s ACWI global equity index has almost fully recovered those losses. The release of the latest IMM report revealed that long GBP positions held by Leveraged Funds had been cut for the second consecutive week to the 6th August driven by the broad-based position unwind which has run out of steam.

It has meant that the GBP has recovered this week even after the releases of the latest UK labour market and CPI report have on the whole supported market expectations for further BoE rate cuts this year. The biggest surprise was the sharper drop in the annual rate of services CPI to 5.2% in July from 5.7% which was well below the BoE’s own forecast. However, the downside surprise was mainly driven by volatile categories such as air fares and hotel prices. Core services excluding accommodation services held at 5.5% in July. The BoE will be watching closely in the coming months to see if the slowdown in services inflation is sustained. The weaker inflation print is not sufficient on its own to encourage the BoE to deliver back to back cuts in September. We are sticking to our forecast for the next rate cut to be delivered in November given that the first cut in August was a close call. A gradual pace of BoE cuts should not trigger a bigger correction lower for the GBP. The still higher yields on offer in the UK and stronger cyclical momentum for the UK economy remain supportive for the GBP. The UK economy expanded strongly for the second consecutive quarter by 0.6% in Q2 although weaker personal consumption and business investment suggest that the much stronger pace of growth is unlikely to be sustained in 2H of this year.

The EUR has also continued to strengthen against the USD over the past week even as US yields have picked up as market participants have scaled back expectations for the Fed to deliver a larger 50bps cut in September. It leaves EUR/USD threatening to break above the topside of the current 1.0500-1.1000 trading range. The release of the ECB’s latest negotiated wage indicator for Q2 will attract market attention in the week ahead (Thurs). It follows the release of a study from the WSI earlier this week reporting that collective-bargaining agreements in Germany during the 1H of this year point to a 5.6% increase for 2024 as a whole which would be the fastest in more than a decade. The euro-zone rate market is still confident that the ECB will cut again in September even though policymakers have indicated that it is not a done deal.

GBP REBOUNDS AFTER SELL-OFF IN EARLY AUGUST

Source: Bloomberg, Macrobond & MUFG GMR

SLOWDOWN IN UK INFLATION CONTINUES

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Ccy |

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

USD |

08/19/2024 |

15:00 |

Leading Index |

Jul |

-0.3% |

-0.2% |

! |

|

AUD |

08/20/2024 |

02:30 |

RBA Minutes of Aug. Policy Meeting |

!! |

|||

|

SEK |

08/20/2024 |

08:30 |

Riksbank Policy Rate |

-- |

3.75% |

!!! |

|

|

EUR |

08/20/2024 |

09:00 |

ECB Current Account SA |

Jun |

-- |

36.7b |

!! |

|

EUR |

08/20/2024 |

10:00 |

CPI YoY |

Jul F |

-- |

2.5% |

!! |

|

CHF |

08/20/2024 |

10:30 |

SNB President Thomas Jordan Speaks |

!! |

|||

|

CAD |

08/20/2024 |

13:30 |

CPI YoY |

Jul |

2.4% |

2.7% |

!!! |

|

JPY |

08/21/2024 |

00:50 |

Trade Balance |

Jul |

-¥350.0b |

¥224.0b |

!! |

|

GBP |

08/21/2024 |

07:00 |

Public Sector Net Borrowing |

Jul |

-- |

13.6b |

!! |

|

USD |

08/21/2024 |

15:00 |

BLS releases payrolls benchmark revisions |

!!! |

|||

|

USD |

08/21/2024 |

19:00 |

FOMC Meeting Minutes |

-- |

-- |

!!! |

|

|

NOK |

08/22/2024 |

07:00 |

GDP Mainland QoQ |

2Q |

-- |

0.2% |

!! |

|

EUR |

08/22/2024 |

09:00 |

HCOB Eurozone Manufacturing PMI |

Aug P |

-- |

45.8 |

!! |

|

EUR |

08/22/2024 |

09:00 |

HCOB Eurozone Services PMI |

Aug P |

-- |

51.9 |

!!! |

|

GBP |

08/22/2024 |

09:30 |

S&P Global UK Manufacturing PMI |

Aug P |

-- |

52.1 |

!! |

|

GBP |

08/22/2024 |

09:30 |

S&P Global UK Services PMI |

Aug P |

-- |

52.5 |

!!! |

|

EUR |

08/22/2024 |

10:00 |

Euro-zone Negotiated Wages for Q2 |

!!! |

|||

|

EUR |

08/22/2024 |

12:30 |

ECB Publishes Account of July Decision |

!! |

|||

|

USD |

08/22/2024 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

USD |

08/22/2024 |

14:45 |

S&P Global US Composite PMI |

Aug P |

-- |

54.3 |

!! |

|

NZD |

08/22/2024 |

23:45 |

Retail Sales Ex Inflation QoQ |

2Q |

-- |

0.5% |

!! |

|

JPY |

08/23/2024 |

00:30 |

Natl CPI YoY |

Jul |

2.7% |

2.8% |

!!! |

|

SEK |

08/23/2024 |

07:00 |

Unemployment Rate SA |

Jul |

-- |

8.2% |

!! |

|

CAD |

08/23/2024 |

13:30 |

Retail Sales MoM |

Jun |

0.2% |

-0.8% |

!! |

|

USD |

08/23/2024 |

15:00 |

Fed Chair Powell speaks |

|

|

|

!!! |

|

USD |

08/23/2024 |

15:00 |

New Home Sales |

Jul |

633k |

617k |

!! |

|

GBP |

08/23/2024 |

20:00 |

BoE Governor Bailey speaks |

!!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- The main focus in the week ahead will be the Fed’s annual economic symposium at Jackson hole between 22nd and 24th The main focus of the symposium this year is “reassessing the effectiveness and transmission of monetary policy”. Market participants will be closely scrutinizing comments from Fed officials for any further guidance over the path for the policy rate. We expect Chair Powell to indicate more confidence that they will begin to lower rates from the next policy meeting in September although it is less clear that a larger 50bps will be delivered. Further evidence of US labour market weakness will be required to encourage the Fed to cut rates more quickly. The release of the annual benchmark revisions for nonfarm payrolls in the week ahead will provide further insight into the health of the US labour market but shouldn’t significantly alter the current picture of softening labour demand. The minutes from the last FOMC meeting from the end of July will also be released. In comparison to comments made at Jackson Hole, the minutes are likely to be viewed as dated limiting their market impact.

- The Riksbank is the only G10 central bank scheduled to meet in the week ahead. We expect the Riksbank to deliver another 25bps rate cut next week lowering the policy rate to 3.50%. After pausing rates at their last meeting in June, the case for lower has been supported by the faster than expected drop for inflation in Sweden. The CPIF excluding energy measure of underlying inflation pressures in Sweden slowed sharply to 2.2% in July down from 3.0% in May. With the next meeting scheduled to take place in relatively quick succession on 25th September, we expect the Riksbank to stick to a series of 25bps rate cuts rather than deliver a larger 50bps cut next week. Alongside delivering a 25bps cut next week, we expect the Riksbank to reiterate that they plan to cut rates two more times by the end of this year.

- The other important data releases in the week ahead will be the latest CPI reports from Canada and Japan for July, the latest PMI surveys from the euro-zone and UK for August, and the ECB’s negotiated wages indicator for Q2. The euro-zone and Canadian rate markets are almost fully priced for further ECB and BoC rate cuts at their next meetings in September. The ECB has indicated though that they are not fully convinced that they will cut rates again as soon as September given ongoing concerns over stronger wage growth in the euro-zone. The negotiated wage indicator held up better than expected in Q1.