To read the full report, please download PDF.

USD benefitting from troubles outside of the US

FX View:

The USD has continued to recover over the past week against the other FX majors. Heightened political risks in France and the BoJ’s slow pace of policy normalization are helping to boost the USD’s relative appeal. At a time when US yields have been adjusting lower in response to softer US inflation data and building evidence of softening US labour demand. Chinese policymakers willingness to allow the CNY to weaken gradually against the USD is providing an additional tailwind. With market participants already expecting a weak US PCE deflator report in the week ahead, we expect the USD to strengthen further ahead of the French elections. In contrast, high beta G10 commodity currencies have been holding up better supported by investor optimism over a soft landing for the global economy.

HIGH BETA G10 COMMODITY FX OUTPERFORMS

Source: Bloomberg, 14:15 BST, 21st June 2024 (Weekly % Change vs. USD)

Trade Ideas:

We are maintaining a short EUR/JPY trade idea ahead of the upcoming French elections on 30th June and 7th July.

JPY Flows – Balance of Payments :

This week we look at the April BoP data and once again we have evidence of a further expansion of the current account surplus – in fact on a 12mth basis to a new record. We also look at French bond buying which relative to pre-covid has not been as strong.

Sentiment Analysis on BoE MPC Minutes :

The latest MPC minutes suggest policy makers could be willing to cut rates as soon as the next policy meeting in August. Inflation sentiment remained distinctly negative as policy makers flag caution on sticky services inflation. While labour market sentiment has worsened to levels not seen since May-2023 as policy makers highlight risks to a loosening labour market.

FX Views

USD: Negative developments overseas provide offset to softer US inflation

The USD has continued to rebound over the past week helping to lift the dollar index back up towards the 106.00-level where it struggled to sustain levels above in the 2H of April. The dollar index is on course to close higher for the third consecutive week this month. The breakdown of the weekly performance reveals a more mixed performance against G10 currencies. The high beta G10 commodity currencies of the NOK, AUD, and CAD have all strengthened against the USD. While the other major currencies of the JPY, GBP, CHF and EUR have all weakened against the USD. The price action is more consistent with risk-on trading conditions. MSCI’s ACWI global equity index has hit fresh record highs at the end of this week while bond yields in developed markets have continued to correct lower after peaking at the end of April. It reflects building investor optimism over a softer landing for the global economy triggered by the recent run of softer US inflation prints. The release in the week ahead of the latest US PCE report is expected to provide confirmation that the core deflator increased by only +0.1%M/M in May which alongside leading indicators pointing towards a further softening of US labour demand is encouraging US rate market participants to price back in multiple Fed rate cuts in the 2H of this year.

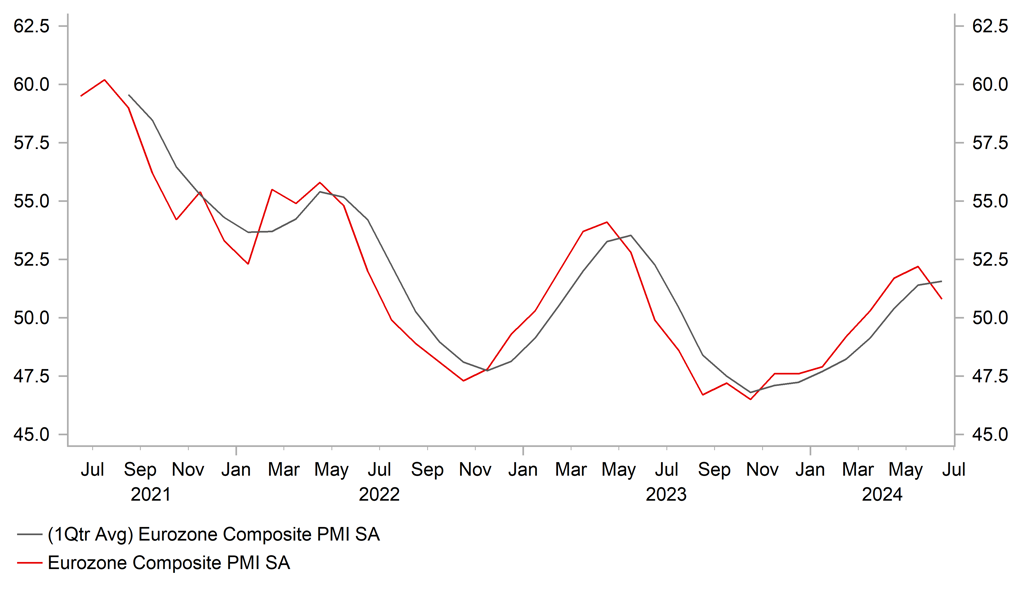

The USD rebound has been mainly driven by negative developments outside of the US. Heightened political risks in France have weighed modestly on the performance on European currencies in recent weeks in including the EUR and the Central European currencies of the CZK, HUF and PLN. It reflects in part a sharp repricing of French government bonds in response to fears that the outcome from the French elections will lead to further fiscal slippage. Earlier this week the European Commission warned France and Italy over their public finances by placing them in the Excessive Deficit Procedure. France’s budget deceit totalled 5.5% of GDP last year and is expected to narrow only marginally to 5.3% of GDP this year which is well above the EU deficit limit of 3% of GDP. Talks between Paris and the Commission will take place in the coming months in order to reach an agreement on required fiscal consolidation plans. Market participants are wary that plans to implement even a slow pace of tightening over say a seven year period could prove more difficult in implement after the upcoming elections. It has already resulted in the yield spread between 10-year French and German government bonds widening out to the highest levels since the euro-zone debt crisis back between 2011 and 2012. In contrast, the negative impact on the EUR has been more modest so far. EUR/USD has weakened by around 2% and EUR/GBP by around 0.8%. We continue to see room for EUR/USD to continue adjusting lower towards the bottom of the current 1.0500 to 1.1000 trading range ahead of the French elections in anticipation of a hung parliament. While we do not expect the negative political developments to derail the tentative economic recovery in the euro-zone, the release today of the softer PMI surveys for June will create some near-term doubts. The euro-zone composite PMI averaged 51.6 in Q2 which is consistent with growth of around 0.2%Q/Q following growth of 0.3%Q/Q in Q1.

DOLLAR INDEX VS SHORT-TERM YIELD SPREAD

Source: Bloomberg, Macrobond & MUFG GMR

JPY FUNDED CARRY TRADES PERFORMING WELL

Source: Bloomberg, Macrobond & MUFG GMR

The other negative developments outside of the US that are encouraging a rebound for the USD are taking place in Asia. The JPY has continued to weaken over the past week resulting in USD/JPY rising back above 159.00 today as it moves back closer to the year to date high from 29th April at 160.17. The price action highlights that the impact of intervention by Japan to support the yen from in late April/early May has almost fully reversed. The JPY and Japanese yields have fallen after the BoJ disappointed market expectations last week by announcing that they will wait until next month’s policy meeting before finalizing plans to slowdown JGB purchases. Comments from BoJ officials this week including by Governor Ueda and Deputy Governor Uchida have indicated though that they are still thinking about raising rates again at the same time as announcing JGB slowdown plans at the July meeting. We are sticking to our forecast for a 15bps rate hike next month. However, it may still prove insufficient to prevent the JPY from weakening further. As we have seen in recent months, the JPY has continued to weaken even as yield spreads have narrowed in Japan’s favour. Market participants would have to move to price in an even faster pace of rate cuts outside of Japan to trigger a reversal of the JPY weakening trend if say optimism over a softer landing was challenged.

The tight correlation between the performance of USD/JPY and USD/CNY has remained in place this week with both the JPY and CNY weakening. USD/CNY has hit a fresh year to date high overnight of 7.2615 as it continues to move back towards last year’s highs between 7.3000 and 7.3500. The gradual adjustment higher for USD/CNY has been encouraged by the PBoC setting higher daily fixes. Yesterday’s daily fix attracted more market attention as it was raised from 7.1159 to 7.1192 which was the largest daily increase since 16th April. It has encouraged more market speculation that Chinese policymakers will continue to allow a weaker CNY through the rest of this year heading into the US election when rising trade tensions between the US and China are expected to attract even more market attention. Overall, the developments point to further Asian currency weakness against the USD in the near-term.

EURO-ZONE ECONOMY IS STILL RECOVERING

Source: Macrobond & Bloomberg & MUFG Research

USD/CNY & USD/JPY MORE STRONGLY CORRELATED

Source: Macrobond & Bloomberg & MUFG Research

Weekly Calendar

|

Ccy |

Date |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EUR |

06/24/2024 |

09:00 |

Germany IFO Business Climate |

Jun |

89.0 |

89.3 |

!! |

|

GBP |

06/24/2024 |

11:00 |

CBI Trends Total Orders |

Jun |

- 25.0 |

- 33.0 |

! |

|

EUR |

06/24/2024 |

13:30 |

ECB's Villeroy Speaks |

!! |

|||

|

EUR |

06/24/2024 |

16:30 |

ECB's Schnabel Speaks |

!! |

|||

|

CAD |

06/24/2024 |

18:30 |

BoC Governor Tiff Macklem Speaks |

!!! |

|||

|

CAD |

06/25/2024 |

13:30 |

CPI YoY |

May |

2.6% |

2.7% |

!!! |

|

USD |

06/25/2024 |

14:00 |

S&P CoreLogic CS 20-City MoM SA |

Apr |

-- |

0.3% |

!! |

|

USD |

06/25/2024 |

15:00 |

Conf. Board Consumer Confidence |

Jun |

100.0 |

102.0 |

!! |

|

USD |

06/25/2024 |

17:00 |

Fed's Cook speaks |

!!! |

|||

|

USD |

06/25/2024 |

19:15 |

Fed's Bowman speaks |

!!! |

|||

|

AUD |

06/26/2024 |

02:30 |

CPI YoY |

May |

3.7% |

3.6% |

!!! |

|

EUR |

06/26/2024 |

10:30 |

ECB's Rehn Speaks |

!! |

|||

|

GBP |

06/26/2024 |

11:00 |

CBI Retailing Reported Sales |

Jun |

-- |

8.0 |

!! |

|

EUR |

06/26/2024 |

11:40 |

ECB's Lane Speaks |

!!! |

|||

|

USD |

06/26/2024 |

15:00 |

New Home Sales |

May |

650k |

634k |

!! |

|

JPY |

06/27/2024 |

00:50 |

Retail Sales MoM |

May |

-- |

1.2% |

!! |

|

SEK |

06/27/2024 |

08:30 |

Riksbank Policy Rate |

3.75% |

3.75% |

!!! |

|

|

EUR |

06/27/2024 |

09:00 |

M3 Money Supply YoY |

May |

-- |

1.3% |

!! |

|

USD |

06/27/2024 |

13:30 |

GDP Annualized QoQ |

1Q T |

1.5% |

1.3% |

!!! |

|

USD |

06/27/2024 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

USD |

06/27/2024 |

13:30 |

Durable Goods Orders |

May P |

0.0% |

0.6% |

!! |

|

JPY |

06/28/2024 |

00:30 |

Jobless Rate |

May |

-- |

2.6% |

!! |

|

JPY |

06/28/2024 |

00:30 |

Tokyo CPI YoY |

Jun |

-- |

2.2% |

!! |

|

JPY |

06/28/2024 |

00:50 |

Industrial Production MoM |

May P |

1.9% |

-0.9% |

!! |

|

UK |

06/28/2024 |

07:00 |

GDP QoQ |

1Q F |

0.6% |

0.6% |

!!! |

|

UK |

06/28/2024 |

07:00 |

Current Account Balance |

1Q |

-- |

-21.2b |

!! |

|

SW |

06/28/2024 |

07:00 |

Retail Sales MoM |

May |

-- |

0.3% |

!! |

|

FR |

06/28/2024 |

07:45 |

CPI YoY |

Jun P |

-- |

2.3% |

!! |

|

GE |

06/28/2024 |

08:55 |

Unemployment Change (000's) |

Jun |

-- |

25.0k |

!! |

|

NO |

06/28/2024 |

09:00 |

Unemployment Rate SA |

Jun |

-- |

2.0% |

!! |

|

CA |

06/28/2024 |

13:30 |

GDP MoM |

Apr |

-- |

0.0% |

!!! |

|

US |

06/28/2024 |

13:30 |

PCE Core Deflator MoM |

May |

0.1% |

0.2% |

!!! |

|

US |

06/28/2024 |

15:00 |

U. of Mich. Sentiment |

Jun F |

-- |

65.6 |

!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- Market attention will continue to focus on political opinion polls in the UK and in France ahead of upcoming elections. The main economic data releases in the week ahead will be: i) the US PCE deflator report for May, ii) the Canadian CPI report for May, and iii) the Australia CI report for May. The US PCE deflator report is expected to reveal that core inflation increased by just 0.1%M/M in May. It follows the release of the much weaker US CPI and PPI report for May. The report should provide reassurance to the Fed that inflation is continuing to slow back towards their 2.0% target after the temporary pick-up in Q1. Fed officials have indicated that they want to see further evidence of slowing inflation in the coming months before considering to cut rates for the first time in September.

- In contrast to the Fed and BoC, the RBA is still weighing up whether to hiker rates further in response to recent upside inflation surprises in Australia. At this week’s policy meeting, the RBA indicated that inflation in Q2 will be particularly important. Another upside inflation surprise in May would encourage expectations that the RBA would hike rates further in 2H of this year.

- Unlike in the US and Australia, inflation has been better behaved so far this year in Canada. Slowing core inflation encouraged the BoC to begin cutting rates at the start of this month. The Canadian rate market is currently pricing in around 17bps of cuts for the next meeting in July. the May CPI report would have to be much stronger than expected to challenge those expectations.