To read the full report, please download PDF.

USD consolidating ahead of tariff announcements

FX View:

The US dollar has weakened against most G10 currencies this week but for most currencies the moves have been contained ahead of the key risk-event next week – the reciprocal tariff announcements on 2nd April. There has been a clear pattern of less and less market reaction to Trump tariff announcements but this may simply reflect difficulty trading the announcements given the uncertainty over the longevity of announcements. There is also we believe a degree of optimism over the scale of tariffs with expectations of exemptions and carve-outs diluting the negative macro impact. However, we see a high chance of very broad-based tariffs with more aggressive action on countries which the US runs larger trade deficits. G10 central bank rate expectations could well adjust to price more cuts that would help propel the dollar stronger for a period. However, FX is a relative price and US growth expectations have declined and with DOGE actions not yet clear, there will be limits to the scale of dollar strength over the short-term before we see renewed depreciation in second half of this year as Fed easing resumes.

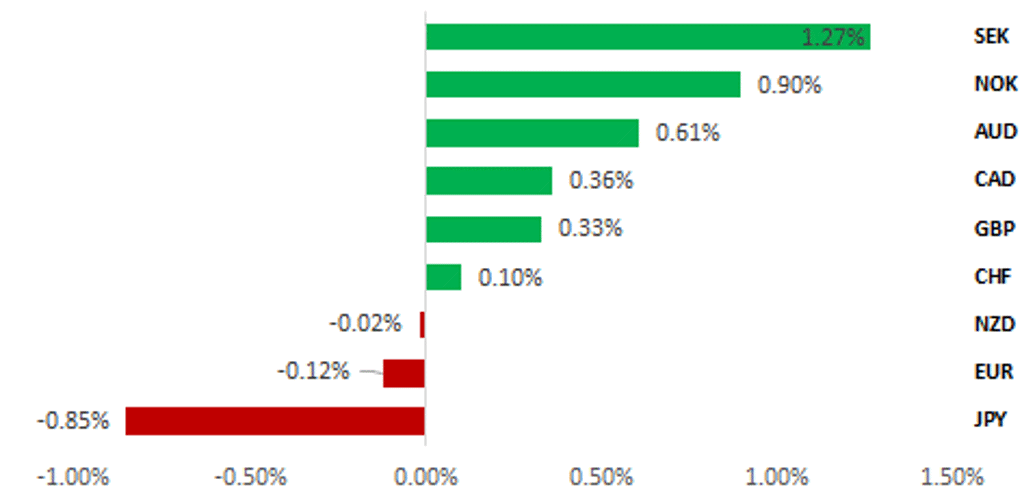

HIGH-BETA G10 OUTPERFORMS AS TARIFF FEARS REMAIN SUBDUED

Source: Bloomberg, 13.30 GMT, 28th March 2025 (Weekly % Change vs. USD)

Trade Ideas:

We are recommending a new long USD/CAD trade idea, and are maintaining our long USD/SEK trade idea.

Weekly Calendar:

The main market moving event and economic data release in the week ahead are likely to be from the US. President Trump has described the 2nd April as “Liberation Day” when he plans to outline his “reciprocal tariff” plans. The release of the latest nonfarm payrolls report for March will be watched closely as well to determine if employment growth continues to slow at the start of this year.

Price Action following Trump's Tariff Announcements:

The decreasing half-life of DXY changes following Trump's tariff announcements indicates that the market's reaction has diminished over time. This trend reflects the market's growing resilience and ability to quickly absorb and adjust to tariff-related news.

FX Views

USD: Tariff plans & the US dollar outlook

The foreign exchange market is in a holding pattern and we doubt there will be substantial moves ahead of the key event next week – the announcement of President Trump’s reciprocal tariff plans on 2nd April. All but one G10 currency (SEK) have moved by less than 1% versus the US dollar despite Trump’s decision to announce a 25% global tariff on all auto and auto-parts imports into the US. That plan becomes effective on 3rd April with further considerations given to auto-parts imports from Canada and Mexico under the USMCA deal. Given the numerous factors cited by the Trump administration in determining the level of reciprocal tariffs (tariff differentials US vs trading partners; sales taxes; non-tariff barriers; alignment of foreign exchange rates; other unfair trade practices) it is impossible to know what metrics will be used and what level tariffs will ultimately be set at. It’s for this reason partly that market participants are not pricing outcomes ahead of 2nd April.

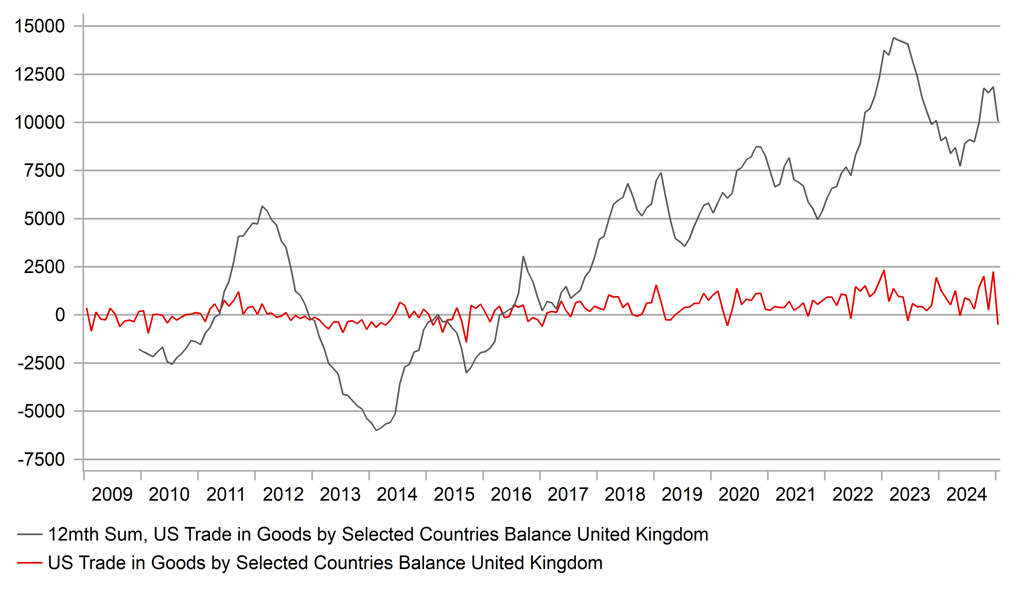

We expect the Trump administration next week to announce broad-based tariffs on all the US’ main trading partners. Countries with larger trade deficits with the US will likely be treated more harshly than countries with smaller deficits or obviously countries running surpluses. The Office of the US Trade Representative (USTR) announced a review on unfair foreign trade practices on 24th January and sought comment on 20th February which closed on 11th March. During this period the USTR emphasised it was seeking comment in relation to trade with G20 countries and countries with the largest trade deficits in goods citing: Argentina; Australia; Brazil; Canada; China; the EU; India; Indonesia; Japan; Korea; Malaysia; Mexico; Russia; Saudi Arabia; South Africa; Switzerland; Taiwan; Thailand; Turkiye; the UK and Vietnam. These countries make up 88% of total goods trade with the US. We can be sure that the focus will be on this list of countries. 9 of the 21 countries listed here are in the Asia region and that’s where the biggest impact is likely to be seen. We are somewhat surprised to see the UK cited on this list. According to the US Census Bureau, the US recorded a USD 12bn trade surplus in 2024. Since Trump’s election victory on 5th November last year, the pound is the 3rd best performing G10 currency in part on optimism that the UK will escape the worst of the reciprocal tariff plan.

The sell-off of the US dollar from the intra-day high in January to the low in March amounted to 6.5% (DXY basis) although nearly half of that move (3.0%) took place in just three trading days as market participants responded to the German fiscal expansion plans. China also announced policy stimulus plans that same week while the US economic data flow has disappointed. So there were some justified relative macro developments that warranted the reversal of the US dollar not related to trade tariff expectations. Over the period since mid-January CFTC positioning data indicates that Leveraged Funds have cut long dollar positions by nearly 75% and long dollar positions are now the smallest since October last year. So the FX market is now much more position-neutral and hence we see much better potential for some recovery if investors begin to reassess the negative impact on economic conditions outside the US. If you narrow down the above trade deficit countries to the top ten which could be treated most harshly, six are in Asia (China; Vietnam; Taiwan; Japan; S. Korea; and India); two are in Europe (Germany and Ireland) and then the two USMCA countries (Canada and Mexico). The countries that saw the biggest increases in trade deficits with the US (2024 vs 2023) were Taiwan (+52%); Ireland (33%); and S. Korea (27%). These are the currencies where we see risks of bigger sell-offs vs the dollar.

12MTH SUM US GOODS TRADE BALANCE WITH THE UK

Source: Bloomberg, Macrobond & MUFG GMR

USD POSITIONING – LEVERAGED FUNDS

Source: Bloomberg, Macrobond & MUFG GMR

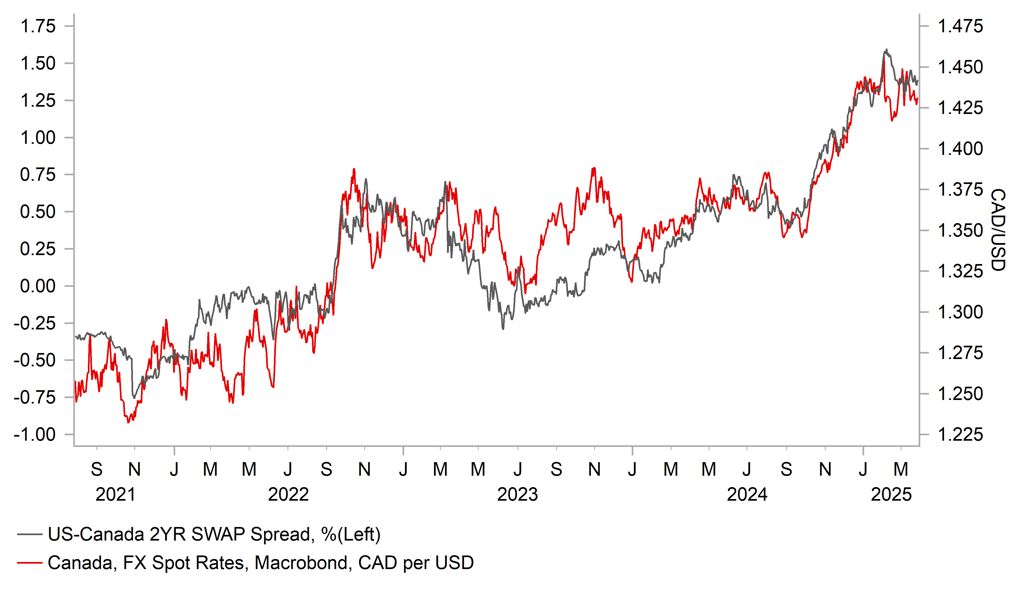

When looking at the performance of CAD and MXN it’s clear that there remains a high level of optimism over the impact of tariffs. Investors believe possibly that Trump will be restrained in his announcements, or the announcements will be quickly watered down or reversed, or that the US fallout will be as bad as in foreign countries. We see all of those possibilities as unlikely or wrong. The macro impact in the countries mentioned above will be worst and we see tariffs remaining in place for longer than perhaps is currently assumed. Interest rate differentials will remain a key channel for FX adjustments. Terminal rates implied in OIS pricing suggest on average no more than 50bps of further monetary easing across most of G10 (excl Japan, Sweden & Switzerland) which we believe could be questioned and adjusted to the downside as expectations of bigger hits to economies increase. For example, the BoC has already laid out a scenario of a 25% tariff on Canada imports to the US resulting in a 2.0ppt hit to GDP in year one and 1.5ppt hit in year two. The ECB has estimated a 0.5ppt GDP hit. Both assume retaliatory tariffs are implemented. But these hits to growth would likely prompt terminal policy rates to move lower across much of G10 and more widely.

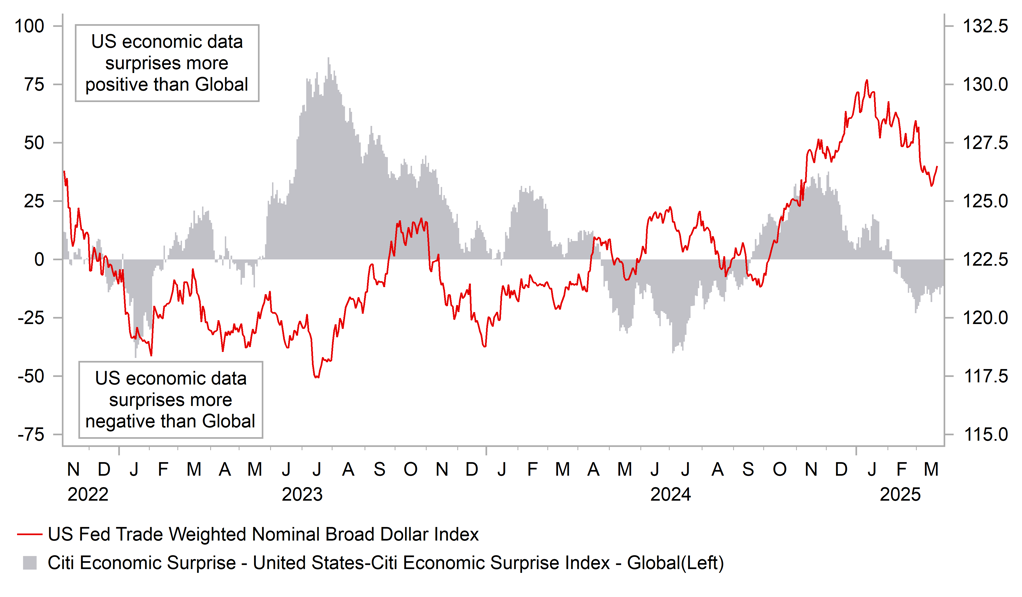

Of course FX is a relative price and part of the US dollar sell-off related to the expectations of weaker US growth ahead as economic data worsened due to trade and general policy uncertainties. Fed policy is also restrictive and we believe the US is at a point in the economic cycle when growth is set to slow anyway. DOGE remains a variable that is difficult to predict but actions by DOGE will clearly add to US economic headwinds. While we see scope for some US dollar recovery from today’s levels (3% or so), the scale of gains will be curtailed by US growth uncertainties and we continue to forecast US dollar weakness in the second half of 2025. Fed caution (due to tariff inflation risks) will likely give way as the labour market weakens and Fed inflation fears recede allowing for rate cuts in H2 that helps take the US dollar around 4% lower than current levels by year-end.

USD/CAD VERSUS US-CA 2-YEAR SWAP SPREAD

Source: Bloomberg, Macrobond & MUFG GMR

US DATA FLOW RELATIVE TO ROW VERSUS USD

Source: Bloomberg, Macrobond & MUFG GMR

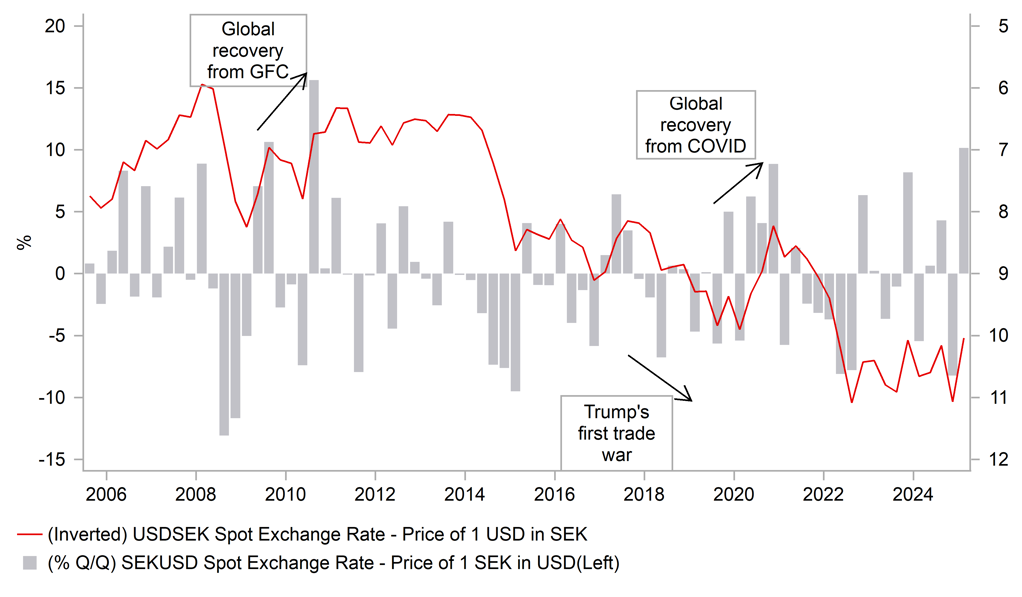

European FX: Has SEK strength overshot improvement in fundamentals?

The top performing G10 currencies at the start of this year have been the European currencies of the SEK (+10.4% YTD vs. USD), NOK (+8.4%) and EUR (+4.1%) alongside the JPY (+4.5%). The outsized gains for European currencies reflect the sharp improvement in investor sentiment towards the region. It would represent the largest quarterly gain for the SEK (vs. USD) since Q3 2010 when the global economy initially recovered robustly from the Global Financial Crisis by 5.2% in 2010. More recently the SEK staged a similar strong rebound during the 2H 2020 when the global economy was recovering robustly initially from the negative COVID shock.

German Chancellor-in-waiting Friedrich Merz’s quick decision to pass legislation to finance a significant loosening in fiscal policy (click here) over the next decade or so has proven to be a game changer for the growth outlook for European economies. It could potentially result in government spending on defence and public infrastructure increasing by over EUR1.0 trillion supporting a stronger economic recovery in Germany in the coming years. At the same time, the Swedish government has announced plans this week to spend an extra SEK300 billion on defence during the next decade. The “loan-financed investment” plans to lift defence spending to 3.5% of GDP by 2030 compared to the previous target of 2.6% set last spring. The ruling coalition and its cooperation partners the Sweden Democrats agree that the change in policy is “urgent” and the “current target is not enough”. Defence spending in Sweden has already been increasing in recent years rising to 2.1% of GDP in 2024 up from 1.7% in 2023. Additional government spending on defence would support the stronger economic recovery already underway in Sweden. Economic growth picked up more strongly than expected during the 2H of last year when GDP expanded by an annualized rate of 2.8%. Stronger growth and the pick-up in inflation at the start of this year has given the Riksbank more confidence to signal an end to their rate cut cycle after lowering the policy rate in total by 1.75 points to 2.25%.

The main downside risks for the SEK that could trigger a setback after recent outsized gains would be the emergence of evidence revealing that heightened policy uncertainty and tariff disruption at the start of President Trump’s second term is having a bigger dampening impact on global growth. Sweden is a small and open economy (exports account for around 55% of GDP) which makes the SEK sensitive to global trade developments. The announcement this week of US plans to implement 25% tariffs on imports of autos and certain auto parts will add to those downside risks going forward especially the longer those tariffs remain in place. Next week’s US “reciprocal tariffs” plan could further increase the risk of a more disruptive global trade war. Sweden would be negatively impacted both directly and indirectly by tariffs imposed on the EU.

SEK GAINS THREATENED BY TRADE DISRUPTION

Source: Bloomberg, Macrobond & MUFG GMR

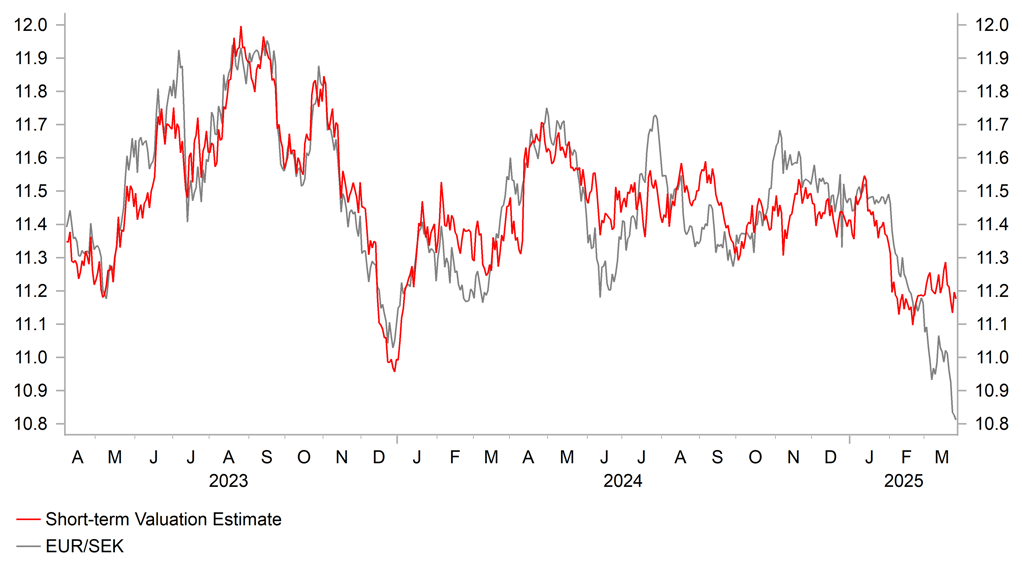

SEK STRENGTH RUNNING AHEAD OF FUNDAMENTALS

Source: Bloomberg, Macrobond & MUFG GMR

Weekly Calendar

|

Ccy |

Date |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

JPY |

31/03/2025 |

00:50 |

Retail Sales MoM |

Feb |

0.2% |

0.5% |

!! |

|

CNY |

31/03/2025 |

02:30 |

Manufacturing PMI |

Mar |

50.4 |

50.2 |

!! |

|

CNY |

31/03/2025 |

02:30 |

Non-manufacturing PMI |

Mar |

50.6 |

50.4 |

!! |

|

EUR |

31/03/2025 |

07:00 |

Germany Retail Sales MoM |

Feb |

0.1% |

0.2% |

!! |

|

EUR |

31/03/2025 |

13:00 |

Germany CPI YoY |

Mar P |

-- |

2.3% |

!!! |

|

JPY |

01/04/2025 |

00:50 |

Tankan Large Mfg Index |

1Q |

12.0 |

14.0 |

!! |

|

AUD |

01/04/2025 |

01:30 |

Retail Sales MoM |

Feb |

0.4% |

0.3% |

!! |

|

AUD |

01/04/2025 |

04:30 |

RBA Cash Rate Target |

4.10% |

4.10% |

!!! |

|

|

EUR |

01/04/2025 |

09:00 |

HCOB Eurozone Manufacturing PMI |

Mar F |

-- |

48.7 |

!! |

|

GBP |

01/04/2025 |

09:30 |

S&P Global UK Manufacturing PMI |

Mar F |

-- |

44.6 |

!! |

|

EUR |

01/04/2025 |

10:00 |

CPI Estimate YoY |

Mar P |

-- |

2.3% |

!!! |

|

EUR |

01/04/2025 |

10:00 |

Unemployment Rate |

Feb |

-- |

6.2% |

!! |

|

EUR |

01/04/2025 |

13:30 |

ECB's Lagarde Speaks |

!!! |

|||

|

USD |

01/04/2025 |

15:00 |

JOLTS Job Openings |

Feb |

-- |

7740k |

!! |

|

USD |

01/04/2025 |

15:00 |

ISM Manufacturing |

Mar |

49.8 |

50.3 |

!! |

|

EUR |

01/04/2025 |

17:30 |

ECB's Lane Speaks |

!! |

|||

|

USD |

02/04/2025 |

13:15 |

ADP Employment Change |

Mar |

118k |

77k |

!! |

|

USD |

02/04/2025 |

15:00 |

Durable Goods Orders |

Feb F |

-- |

0.9% |

!! |

|

USD |

02/04/2025 |

Tbc |

Reciprocal Tariffs Plan Released |

|

|

|

!!! |

|

CHF |

03/04/2025 |

07:30 |

CPI YoY |

Mar |

-- |

0.3% |

!! |

|

EUR |

03/04/2025 |

09:00 |

HCOB Eurozone Services PMI |

Mar F |

-- |

50.4 |

!! |

|

GBP |

03/04/2025 |

09:30 |

S&P Global UK Services PMI |

Mar F |

-- |

53.2 |

!! |

|

EUR |

03/04/2025 |

12:30 |

ECB Publishes Account of March Meeting |

!! |

|||

|

USD |

03/04/2025 |

13:30 |

Trade Balance |

Feb |

-$110.0b |

-$131.4b |

!! |

|

USD |

03/04/2025 |

13:30 |

Initial Jobless Claims |

-- |

-- |

!! |

|

|

USD |

03/04/2025 |

15:00 |

ISM Services Index |

Mar |

53.2 |

53.5 |

!!! |

|

SEK |

04/04/2025 |

07:00 |

CPI YoY |

Mar P |

-- |

1.3% |

!! |

|

CAD |

04/04/2025 |

13:30 |

Net Change in Employment |

Mar |

-- |

1.1k |

!!! |

|

USD |

04/04/2025 |

13:30 |

Change in Nonfarm Payrolls |

Mar |

120k |

151k |

!!! |

Source: Bloomberg, Macrobond & MUFG GMR

Key Events:

- The main market moving event and economic data release in the week ahead are likely to be from the US. President Trump has described the 2nd April as “Liberation Day” when he plans to outline his much anticipated plans for “reciprocal tariffs”. It follows the announcement this week of 25% tariffs on the imports of autos and certain auto parts. Alongside the auto tariff announcement he attempted to dampen investor concerns over potential disruption from “reciprocal tariffs” by stating he’ll “probably be more lenient than reciprocal” while adding that there will be “some exceptions”. A White House official also told CNBC that President Trump may not factor in non-tariff barriers, indirect levies like on value-added taxes, into his reciprocal tariffs.

- The release of the latest nonfarm payrolls report for March will be watched closely as well to determine if employment growth continues to slow at the start of this year. Employment growth has averaged 138k/month in the first two months of this year compared to 209k/month in the Q4 of last year and the twelve month average of 162k/month. There has been building concerns that DOGE’s efforts to shrink the state alongside heightened policy uncertainty will result in weaker employment growth. The Fed’s plans for further rate cuts this year are built on the assumption that the unemployment rate will rise modestly up towards 4.5%. Slower immigration and labour supply growth could dampen the move higher in the unemployment rate even as employment growth slows.

- Elsewhere, the main economic data releases will be the latest China PMI surveys for March, and euro-zone and Swiss CPI reports for March. ECB officials have indicated this week that they will be weighing up at their next meeting in April whether to skip a rate cut or deliver another back-to-back 25bps cut. The decision is no longer as much of a done deal as at previous meetings with the policy rate judged closer to or already neutral. President Trump’s tariff plans and EU retaliation will heighten uncertainty over ECB policy.

- The RBA is expected to leave rates on hold at 4.10% in the week ahead. It follows on from their decision to cut rates for the first time at their previous policy meeting in February. We expect the RBA to leave the door open to another cut at the following policy meeting in May encouraged by the release of the softer Australian CPI report for February.