Key Points

Please click on download PDF above for full report

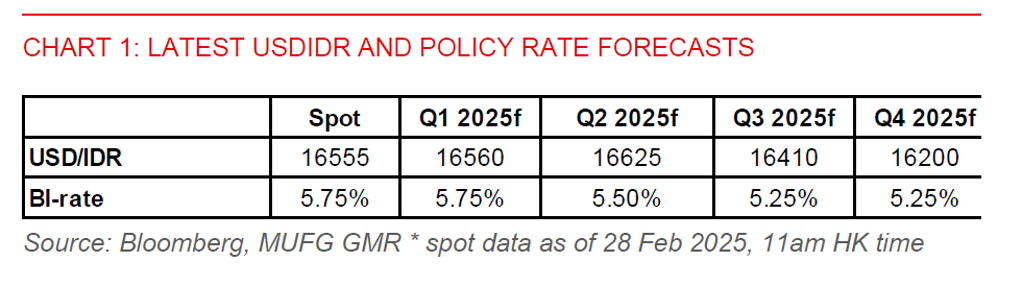

- We have been expecting rupiah weakness amid heightened global uncertainties. Indeed, global trade uncertainty will likely persist, while domestic fiscal uncertainty is also keeping investors on the sidelines. But the pace of rupiah depreciation has still surprised us, despite ongoing resolve by authorities to support the currency. USD/IDR is at risk of testing the covid pandemic level high of 16,625. We’ve revised up our USDIDR forecast to 16,625 by Q2, from 16,450 previously.

- Tariff risks have returned to the fore following a period of calm. US President Trump has confirmed that the proposed 25% tariffs on Canada and Mexico will come into effect on 4 March, while he has raised the prospect of an additional 10% tariff on imports from China and reciprocal tariffs on 2 April. The US dollar has regained strength on the back of renewed tariff rhetoric from Trump, with the broad US dollar index regaining strength.

- Indonesia, being a domestic oriented economy. is likely less affected by global trade frictions. It is also not that exposed to Trump’s proposal of reciprocal tariff hikes, as both Indonesia and the US have imposed a similar import tariff rate on one another’s products, at about 4.1% on a weighted average basis. Nonetheless, Indonesia’s economy won’t be immune to higher US tariffs on China, given its rising export exposure to the Chinese market.

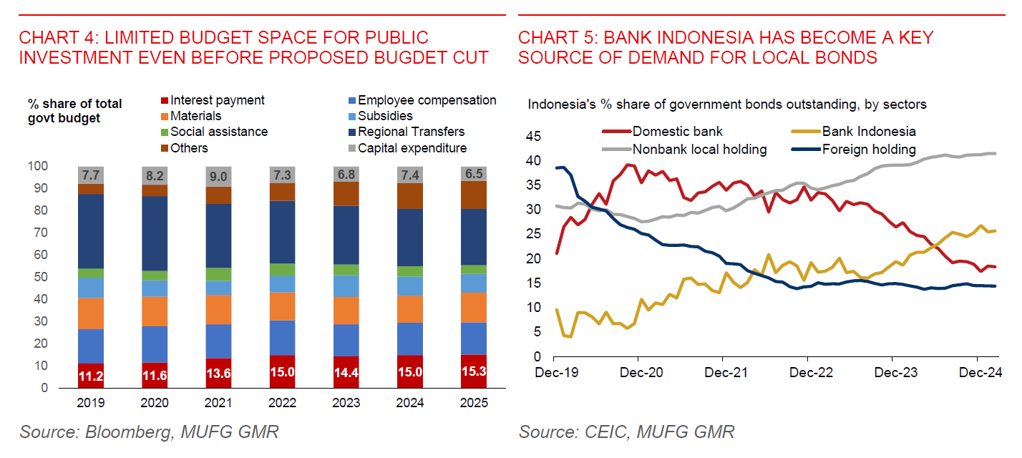

- In addition to that, there is greater domestic fiscal uncertainty today as President Prabowo shapes his economic policies. Prabowo plans to cut the 2025 state budget spending by IDR306.7 trillion (about $19bn) to fund his social initiatives such as the free school lunch programme. However, this could hinder public investment, while it has led to students taking to the streets to protest in recent days. Spending by ministries and agencies would be cut by IDR256.1 trillion, while local government allocations would decline by IDR50.6 trillion. It remains to be seen whether the government is willing to scale back some of its fiscal initiatives.

- Also, the risk of further government debt monetization has hurt market sentiment, raising the risk premia on Indonesian equities and rupiah. Bank Indonesia plans to purchase more than $9 billion of government bonds to support Prabowo’s affordable housing programme. This will add to BI’s already sizeable holding of about one-quarter of government bonds outstanding.

- President Prabowo has launched Danantara - a second sovereign wealth fund – on 24 February with the aim of optimising state-owned enterprise (SOE) investments for socio-economic development. This has given rise to market concerns about corporate governance of this fund. Former President Jokowi will be one of the fund’s advisor, while Sri Mulyani will also be a member of the supervisory board. While there are likely checks and balances in place, as well as potential benefits of optimising state-owned enterprise (SOE) investments, investors may perhaps like to get more assurance for now.

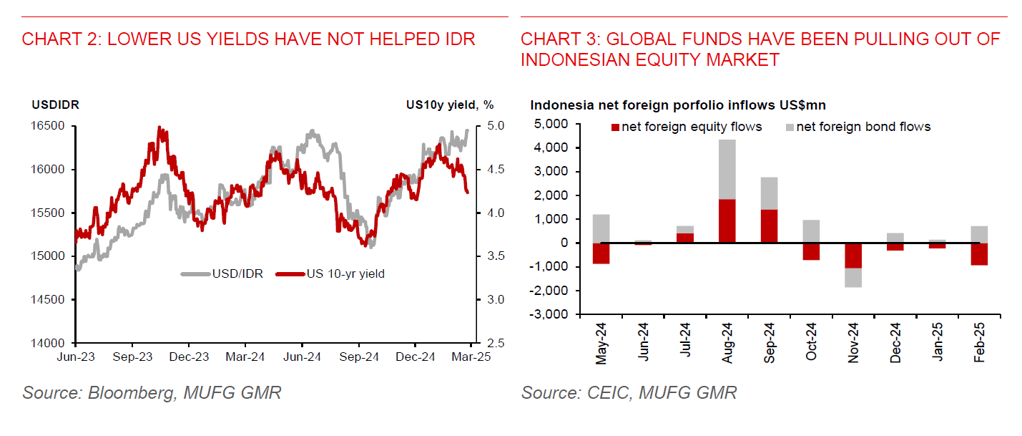

- Given heightened uncertainties, global funds have pulled out of Indonesia’s equity market since President Trump’s inauguration on 20 January, reflecting cautious market sentiment. The Jakarta Composite Index (JCI) has corrected by about 13% since the US election on 5 November.