Please download PDF from above for the following currencies.

Australian dollar // New Zealand dollar //Canadian dollar // Norwegian krone // Swedish Krona // Swiss franc // Czech koruna // Hungarian forint //Polish zloty // Romanian leu // Russian rouble // South African rand // Turkish lira // Indian rupee // Indonesian rupiah // Malaysian ringgit // Philippine peso //Singapore dollar // South Korean won // Taiwan dollar // Thai baht // Vietnamese dong // Argentine peso // Brazilian real // Chilean peso // Mexican peso // Crude oil // Saudi riyal // Egyptian pound

Monthly Foreign Exchange Outlook

DEREK HALPENNY

Head of Research, Global Markets EMEA and International Securities

Global Markets Research

Global Markets Division for EMEA

E: derek.halpenny@uk.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

E: lee.hardman@uk.mufg.jp

LIN LI

Head of Global Markets Research Asia

Global Markets Research

Global Markets Division for Asia

E: lin_li@hk.mufg.jp

MICHAEL WAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: michael_wan@sg.mufg.jp

LLOYD CHAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: lloyd_chan@sg.mufg.jp

EHSAN KHOMAN

Head of Commodities, ESG and Emerging Markets Research – EMEA

DIFC Branch – Dubai

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Analyst, ESG and Emerging Markets Research – EMEA

DIFC Branch – Dubai

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

December 2024

KEY EVENTS IN THE MONTH AHEAD

1) MONETARY POLICY TO TAKE FOCUS

The ‘Trump trade’ looks to have run its course for now having commenced in early October and run through to 22nd November (USD peak) – over that period the DXY advanced by close to 7%. Politics could now take a backseat given President-elect Trump has named his cabinet meaning the next key scheduled event will be inauguration on 20th January. We will potentially get further hints on policy actions but the move in FX and rates certainly incorporates a high level of expectations of a quick implementation of trade tariffs, a move to commence immigrant deportations and a push to get Trump’s tax plans through Congress. In the meantime the focus is likely to shift back to fundamentals and monetary policy. The US jobs report on 6th December will be important in shaping expectations of what the FOMC will do on 18th December and assuming no major surprise strength in the jobs report, we expect the FOMC to cut by 25bps. Nine of the G10 central banks will meet in December (RBNZ will not) and we expect the BoC (11th), the ECB (12th), the SNB (12th), and Riksbank (19th) to all cut probably by 25bps. The BoC and the SNB could surprise and cut by 50bps. The RBA (10th), the BoE (19th), and Norges Bank (19th) will likely maintain their current monetary stances. Communications on guidance in 2025 from all central banks will likely be cautious given the uncertainties over Trump’s trade policy approach and the potential for countries to then retaliate. Renewed US dollar strength could be curtailed, especially against the euro given the very strong seasonal bias that tends to result in EUR/USD appreciation in December.

2) BoJ THE ODD ONE OUT AGAIN

With the eight other G10 central banks meeting in December either cutting or leaving policy rates unchanged, we believe the BoJ could well be the odd one out in hiking rates. The BoJ meeting will follow the FOMC meeting less than twelve hours later and we may well see an FOMC cut followed by a BoJ hike. It’s not a done deal yet but the inflation data in November (PPI services and Tokyo CPI) certainly could provide the justification for a move. Given the financial market turmoil that followed the July rate hike we would certainly expect some communication signalling a plan to hike. There are no scheduled speeches by senior BoJ officials (only Nakamura on 5th Dec who is a dove) but we could have comments from Diet appearances or via the media to hint at possible action at the December meeting.

3) LOOKING FOR POLICY GUIDELINES FROM DECEMBER’S MEETINGS

There are two major policy meetings to watch in China in December, namely the Annual Central Economic Work Conference and Politburo meeting. Typically, these two meetings allow Chinese leaders to review the economic work done in the year and lay out the main economic priorities in the following year, which we may reveal a clearer roadmap on future fiscal expansion and other stimulus plans. Meanwhile, the PBoC is likely to deliver a 25bps-50bps RRR cut in December to ease the liquidity condition and reduce the cost of funding for commercial banks, which would help alleviate the squeeze in net interest margin as well.

Forecast rates against the US dollar - End-Q1 to End-Q4 2025

|

Spot close 29.11.24 |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

JPY |

150.44 |

154.00 |

152.00 |

150.00 |

148.00 |

|

EUR |

1.0550 |

1.0200 |

1.0500 |

1.0600 |

1.0800 |

|

GBP |

1.2700 |

1.2360 |

1.2800 |

1.2930 |

1.3010 |

|

CNY |

7.2440 |

7.4000 |

7.5000 |

7.5000 |

7.4000 |

|

AUD |

0.6510 |

0.6350 |

0.6300 |

0.6500 |

0.6600 |

|

NZD |

0.5911 |

0.5800 |

0.5750 |

0.5900 |

0.6000 |

|

CAD |

1.4010 |

1.4400 |

1.4100 |

1.3900 |

1.3700 |

|

NOK |

11.058 |

11.765 |

11.619 |

11.415 |

11.019 |

|

SEK |

10.921 |

11.569 |

11.524 |

11.321 |

10.926 |

|

CHF |

0.8820 |

0.9020 |

0.8760 |

0.8770 |

0.8700 |

|

|

|

|

|

|

|

|

CZK |

23.924 |

25.100 |

24.570 |

24.430 |

23.800 |

|

HUF |

391.19 |

408.80 |

400.00 |

398.10 |

393.50 |

|

PLN |

4.0665 |

4.2650 |

4.1900 |

4.1980 |

4.0740 |

|

RON |

4.7149 |

4.8820 |

4.7710 |

4.7550 |

4.6940 |

|

RUB |

107.32 |

113.97 |

117.36 |

121.71 |

125.48 |

|

ZAR |

18.039 |

18.500 |

18.750 |

19.000 |

18.750 |

|

TRY |

34.690 |

37.500 |

40.000 |

41.500 |

42.500 |

|

|

|

|

|

|

|

|

INR |

84.490 |

85.200 |

85.500 |

85.700 |

86.000 |

|

IDR |

15843 |

16250 |

16210 |

16170 |

16100 |

|

MYR |

4.4425 |

4.5700 |

4.5500 |

4.5200 |

4.4800 |

|

PHP |

58.592 |

59.700 |

59.300 |

59.000 |

58.800 |

|

SGD |

1.3418 |

1.3800 |

1.3750 |

1.3700 |

1.3650 |

|

KRW |

1398.0 |

1430.0 |

1450.0 |

1450.0 |

1440.0 |

|

TWD |

32.496 |

33.100 |

33.300 |

33.200 |

33.000 |

|

THB |

34.299 |

36.100 |

36.000 |

35.700 |

35.500 |

|

VND |

25310 |

25800 |

25900 |

25800 |

25700 |

|

|

|

|

|

|

|

|

ARS |

1009.2 |

1110.0 |

1200.0 |

1310.0 |

1500.0 |

|

BRL |

5.9904 |

6.1000 |

6.2000 |

6.3000 |

6.4000 |

|

CLP |

972.95 |

1030.0 |

1050.0 |

1070.0 |

1050.0 |

|

MXN |

20.305 |

22.000 |

21.500 |

21.000 |

20.500 |

|

|

|||||

|

Brent |

73.23 |

73.00 |

69.00 |

74.00 |

77.00 |

|

NYMEX |

69.25 |

68.00 |

64.00 |

69.00 |

72.00 |

|

SAR |

3.7564 |

3.7500 |

3.7500 |

3.7500 |

3.7500 |

|

EGP |

49.565 |

49.700 |

49.300 |

49.100 |

48.700 |

Notes: All FX rates are expressed as units of currency per US dollar bar EUR, GBP, AUD and NZD which are expressed as dollars per unit of currency. Data source spot close; Bloomberg closing rate as of 4:30pm London time, except VND which is local onshore closing rate.

US dollar

|

Spot close 29.11.24 |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

USD/JPY |

150.44 |

154.00 |

152.00 |

150.00 |

148.00 |

|

EUR/USD |

1.0550 |

1.0200 |

1.0500 |

1.0600 |

1.0800 |

|

Range |

Range |

Range |

Range |

||

|

USD/JPY |

145.00-160.00 |

143.00-158.00 |

141.00-156.00 |

139.00-154.00 |

|

|

EUR/USD |

0.9900-1.0600 |

1.0100-1.0800 |

1.0300-1.1000 |

1.0400-1.1200 |

MARKET UPDATE

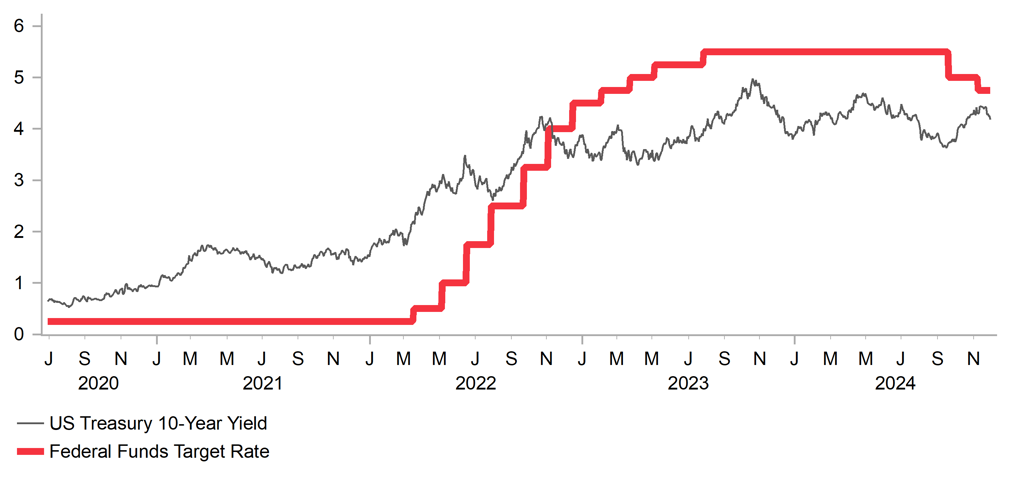

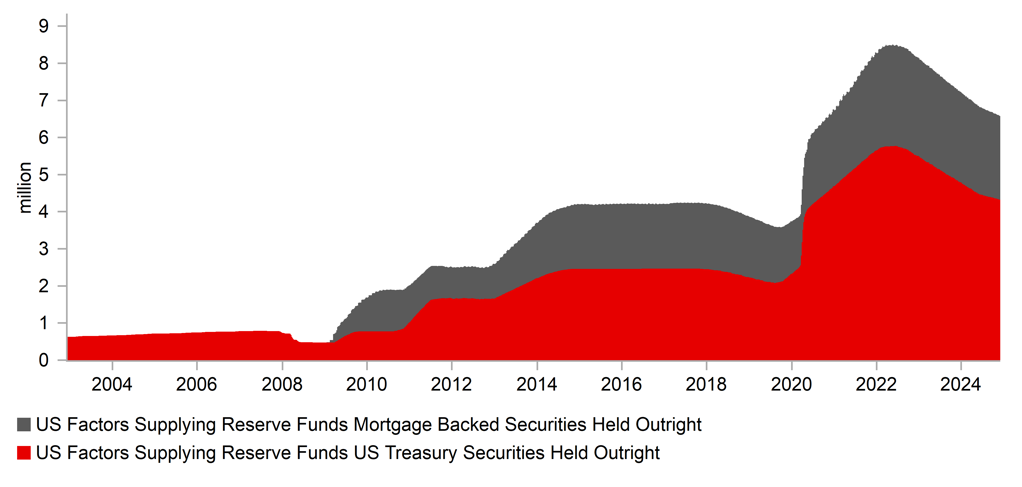

In November the US dollar strengthened notably against the euro in terms of London closing rates, from 1.0859 to 1.0550. However, the dollar weakened against the yen, from 152.43 to 150.44. The FOMC at its meeting in November cut the federal funds rate by 25bps to a range of 4.50% to 4.75%, and followed a 50bp cut in September. The FOMC continued with its policy of reducing its securities holdings with QT ongoing but at a reduced rate of USD 60bn per month through a reduction in UST bond holdings from USD 60bn to USD 25bn. The pace of reduction in the holdings of MBS remains at USD 35bn per month.

OUTLOOK

The US dollar on a DXY basis strengthened further in November in response to the victory for Donald Trump in the presidential election on 5th November. We had highlighted in this publication over recent months our view for a US dollar gain of around 7-8% on a Trump victory. When considering the ‘Trump trade’ recommenced in October, the drop from close to 1.1200 to the lows around 1.0400 in EUR/USD equates close to our estimated move. US Treasury yields and US equities moved higher as well on the back of expectations that Trump’s policies will lift growth, inflation and corporate earnings. Trump’s cabinet picks confirm the importance of loyalty over experience and the potential for disruption over the status quo. Trump did take more time on his economic / financial market-related picks that indicated he valued experience in those fields as well. The choice of Howard Lutnick as Commerce Secretary with an increased remit over the Office of the US Trade Representative make us confident of a quick start to implementing trade tariffs unlike in Trump’s first term. The US Trade Rep (Jamieson Greer) is also pro-trade tariffs and Trump’s threat to implement tariffs on China, Canada and Mexico on day one strengthens the likelihood of an aggressive start to trade policies in January.

The expectations of higher inflation due to trade tariffs on all US imports, increased deportations and tax cuts resulted in a paring of Fed rate cut expectations. We still expect a 25bp rate cut in December (assuming NFP is broadly as expected) and then three further cuts in 2025. This is notably less than what we expected if Kamala Harris had won the election and this shift is reflected in the strengthening of the dollar. However, we expect more cuts than is currently priced in the OIS market and there is a risk that Trump does not deliver tariffs as aggressively in the near-term. We also are sceptical of Trump’s policies to deliver a pick-up in economic growth without fuelling additional inflationary pressures. Real yields therefore are unlikely to increase and could even decline modestly, which over time will start to undermine the dollar.

We expect a flurry of trade tariff announcements in January along with action on deportations and a push for quick legislation on tax cuts (similar to 2017) that will fuel renewed dollar appreciation. We may see the dollar peak in 1H 2025 before we see some retracement as the US economy slows and the Fed cuts rates

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

Policy Rate |

4.58% |

4.13% |

3.88% |

3.63% |

3.63% |

|

3-Month T-Bill |

4.46% |

4.01% |

3.76% |

3.55% |

3.58% |

|

10-Year Yield |

4.19% |

4.50% |

4.63% |

4.75% |

4.63% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

We think the Fed will cut rates in December since it was in the September SEP forecast. The latest FOMC minutes were dovish and flagged that market functioning is in focus (with the Fed thinking about reducing the RRP rate by 5bps) so why skip at year-end and create unnecessary volatility during a potential illiquid period for broader markets. Not to mention skipping may seem political since its in their forecasts from before the election and they have not really signaled the cut is off the table. The only way the Fed does not cut is if the NFP data from November meaningfully beats expectations and the prior weaker NFP data gets revised higher. We are skeptical that the latest NFP report will be strong given that the data collection period was during the election week. However, we do believe December will be the last of the consecutive meeting cuts, and expect the tone of the meeting to be mildly hawkish, with an emphasis on taking it slow and seeing what incoming data and policies look like in 2025. In the updated December SEP forecast, the Committee could reduce cuts from four to three for 2025 and signal there is no need to rush to normalize policy, as the rate cuts delivered thus far is already a big down payment in their pursuit of neutral rates.

(George Goncalves)

10YR UST YIELD VS. FED FUNDS RATE

Source: MUFG GMR, Bloomberg

FOMC SECURITIES HOLDINGS, UST VS. MBS

Source: Bloomberg, Macrobond

Japanese yen

|

Spot close 29.11.24 |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

USD/JPY |

150.44 |

154.00 |

152.00 |

150.00 |

148.00 |

|

EUR/JPY |

158.71 |

157.10 |

159.60 |

159.00 |

159.80 |

|

Range |

Range |

Range |

Range |

||

|

USD/JPY |

145.00-160.00 |

143.00-158.00 |

141.00-156.00 |

139.00-154.00 |

|

|

EUR/JPY |

151.00-162.00 |

150.00-163.00 |

149.00-163.00 |

149.00-163.50 |

MARKET UPDATE

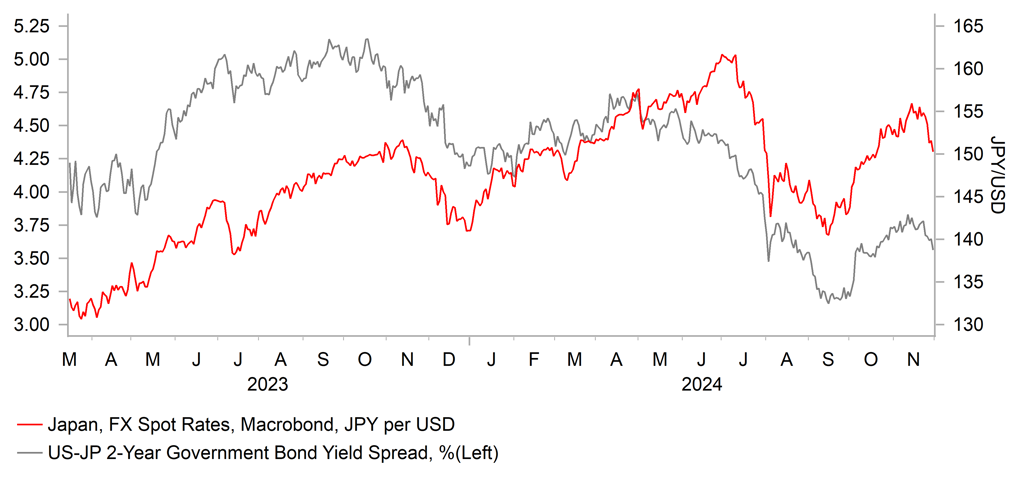

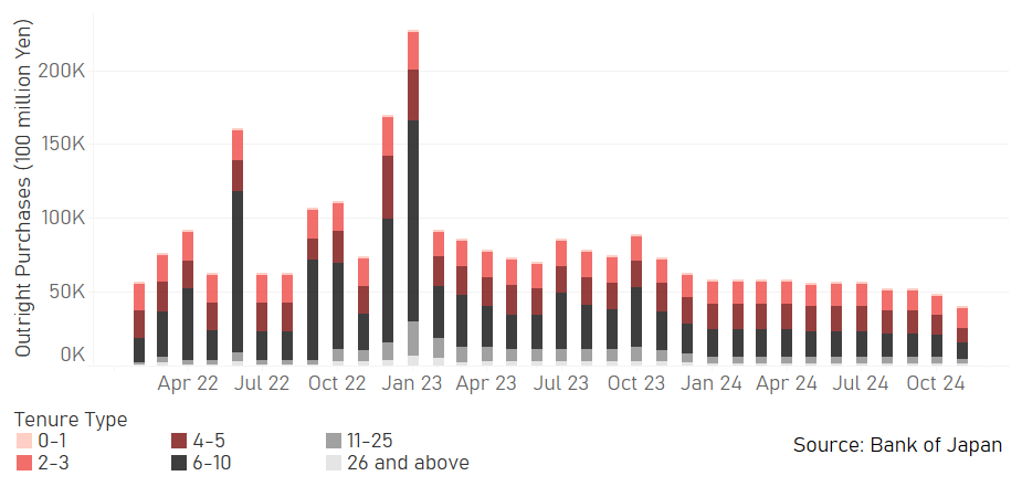

In November the yen strengthened versus the US dollar in terms of London closing rates from 152.43 to 150.44. In addition, the yen strengthened versus the euro, moving from 165.52 to 158.71. The BoJ did not meet in November and hence the monetary stance was unchanged following the announcements in July when the BoJ hiked the key policy rate 15bps to 0.25% and cut the JGB monthly purchase rate by JPY 400bn per quarter, which is estimated to see purchases fall to around JPY 2.9trn per month by Q1 2026.

OUTLOOK

The yen was the top performing G10 currency in November, marginally outperforming the strong US dollar as the focus shifted from the implications of Donald Trump’s election victory to the prospects of another rate hike from the BoJ. The resilience of the yen may also have reflected the sharp depreciation in October ahead of the election – the yen was the second worst performing G10 currency in October, falling by 5.5%. The threat of intervention may have helped curtail yen selling in November. Expectations of a different approach to FX policy under new PM Ishiba receded after comments from senior MoF officials expressing dissatisfaction with yen depreciation and hinting at possible intervention. Finally, the new LDP-led minority government managed with relative ease to agree a fiscal stimulus package with the main opposition party – the DPP – to help support households and boost real GDP growth which in turn lifted expectations of a BoJ rate hike. The fiscal stimulus agreement further reinforced expectations of a rate hike by the BoJ.

We recently pushed back the timing of the next BoJ rate hike from December to January but in light of developments in November now believe that decision was premature. We are reverting back to a December hike due to the above factors and due to the victory of Donald Trump in the election. That development has raised the risk of higher yields in the US that increases the risk of an unwarranted weakening of the yen. While initially PM Ishiba and other government officials urged caution in regard to further rate hikes, the situation has changed quickly and with the Upper House elections in July 2025, the government will be more supportive of action to limit yen selling risks. The BoJ have also likely become more confident in the virtuous cycle between wages and inflation. PPI Services inflation data released by the BoJ in November revealed this measure related specifically to companies with a high labour cost ratio jumped to 3.3% YoY, the highest level since 1992. Rengo, Japan’s largest trade union has set a target of “at least 5%” – similar to this year for the FY25 wage negotiations set to commence in February-March next year.

There is still a high chance that in the initial stages of the second Trump presidency that USD/JPY could rebound as the dollar more broadly strengthens again, especially if Japan is hit with tariffs, but we would then expect to see USD/JPY drift lower with the Fed still having scope to cut rates and the BoJ to hike.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

Policy Rate |

0.25% |

0.50% |

0.50% |

0.75% |

1.00% |

|

3-Month Bill |

0.13% |

0.70% |

0.85% |

0.90% |

1.10% |

|

10-Year Yield |

1.05% |

1.20% |

1.25% |

1.30% |

1.40% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year JGB yield increased in November largely reflecting the move in US Treasury yields following Donald Trump’s election victory with the 10-year JGB yield closing at 1.05%, up 10bps. The JGB move in yields also reflected domestic developments after the agreement on a supplementary budget to finance additional government spending to boost economic growth. The JPY 13.9trn additional budget was slightly larger than a year earlier and will be in part financed by tax revenues that are stronger than expected and some unused funds from previous spending plans. It means that JGB issuance related to the supplementary budget will be JPY 6.69trn. The stimulus package will help maintain confidence that Japan has moved to a new era of modest positive inflation after years of deflation. That’s the view of the BoJ as well and in addition to hikes to the key policy rate, the BoJ is set to continue gradually shrinking its balance sheet by reducing its monthly purchase rate of JGBs. The JGB purchase policy is consistent with the gradual increase in the 10-year JGB yield throughout the four quarters of 2025.

USD/JPY VS. SHORT-TERM YIELD SPREAD

Source: Bloomberg, Macrobond

JGB OUTRIGHT MONTHLY PURCHASES

Source: Bank of Japan

Euro

|

Spot close 29.11.24 |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

EUR/USD |

1.0550 |

1.0200 |

1.0500 |

1.0600 |

1.0800 |

|

EUR/JPY |

158.71 |

157.10 |

159.60 |

159.00 |

159.80 |

|

Range |

Range |

Range |

Range |

||

|

EUR/USD |

0.9900-1.0600 |

1.0100-1.0800 |

1.0300-1.1000 |

1.0400-1.1200 |

|

|

EUR/JPY |

151.00-162.00 |

150.00-163.00 |

149.00-163.00 |

149.00-163.50 |

MARKET UPDATE

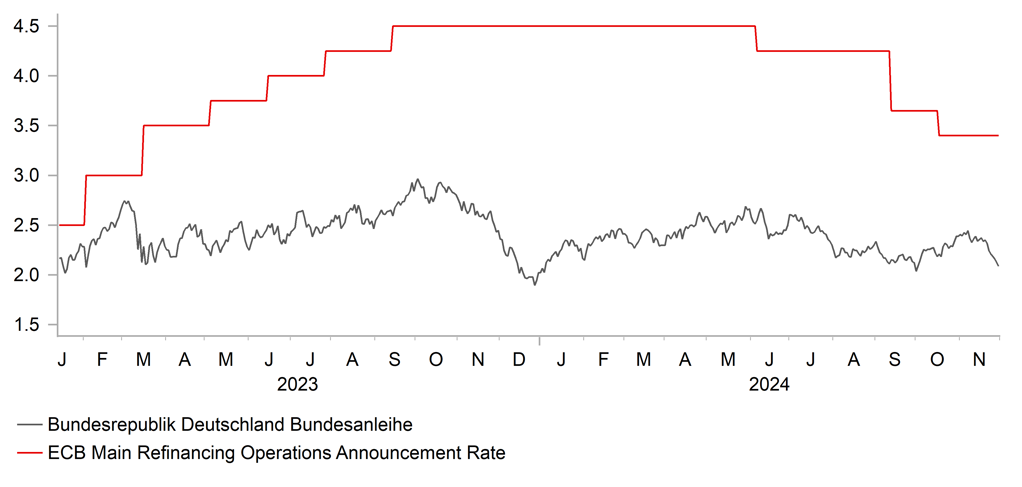

In November the euro weakened notably versus the US dollar in terms of London closing rates, moving from 1.0859 to 1.0550. The ECB did not meet in November and hence the key policy rate remained at 3.25%, following three cuts of 25bps in June and September and October, reversing 75bps of the 450bps of rate hikes through to September 2023. The ECB is running down APP securities and started PEPP run-off in July with about EUR 380bn of securities rolling off the balance sheet in 2024.

OUTLOOK

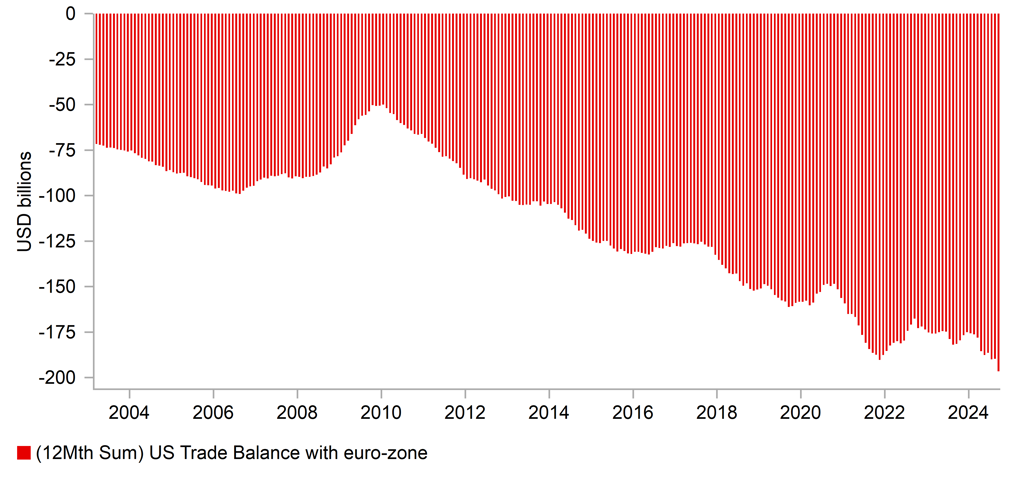

The euro depreciated sharply in November in response to the election victory for Donald Trump. Trump’s anticipated policies on trade tariffs, deportations of illegal immigrants and tax cuts are expected to fuel a further divergence in economic growth and monetary policy. We expect the initial driver of FX in the first quarter and into the second will be on expected trade tariff actions that could drive EUR/USD further lower. The market is now priced for action but it is difficult to know precisely how Trump will act but we do expect an aggressive start that will likely include Europe. The US trade deficit with the euro-zone has widened – since the end of 2019 the deficit has increase from USD 158bn to USD 196bn in September 2024. As one entity, the euro-zone accounts for the largest portion of total US imports, at 14% in 2023. The under-spend in reaching the NATO military spending threshold of 2% of GDP could also incentivise an aggressive approach to the euro-zone. NATO data released earlier this year revealed of the 31 countries reported, eight were below the 2% target and of those eight, seven were euro-zone countries (Canada the other).

The expectations of tariffs has fuelled expectations of a hit to GDP growth that will prompt more aggressive ECB rate cuts. At the end of November, the OIS market was priced for 168bps of cuts from the ECB by the end of next year while pricing for the Fed was a little over 70bps. We view this divergence as excessive and doubt the ECB will cut its policy rate to this extent in circumstances of increased trade conflict and the risks to inflation associated with possible retaliation by the euro-zone. Furthermore, while tariffs on exports to the US will be a clear negative for euro-zone growth, there are certain factors that might mean the impact is less severe than expected. Firstly, euro-zone exports to the US as a percentage of GDP amounts to 3.3%, not insignificant but a size that could mean the negative impact is countered, possibly by improving domestic demand. Inflation is reverting back to target at a time of significant increases in nominal wages. ECB negotiated wages surged by 5.4% YoY in Q3, the biggest increase since the start of the single currency in 1999 which will be a key support for domestic demand conditions going forward.

Growth fears as tariff announcements are made in Q1 into Q2 will weigh on EUR/USD. Trump is unlikely to introduce 10%/20% on imports globally but the euro-zone is at risk of action across a number of sectors. We still see the ECB then cutting by less than priced which with the Fed cutting should allow EUR/USD to recover

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

Policy Rate |

3.25% |

2.50% |

2.00% |

2.00% |

2.00% |

|

3-Month Bill |

2.87% |

2.20% |

1.80% |

1.90% |

1.90% |

|

10-Year Yield |

2.09% |

2.10% |

2.10% |

2.20% |

2.30% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year bund yield fell sharply in November reflecting the election victory for Donald Trump that has increased the prospect of trade tariffs damaging already weak growth in the euro-zone. The 10-year German bund yield fell 30bps to close at 2.09%, more than fully retracing the move higher in yields in October. The US-EZ 10-year spread widened by 20bps. As stated above, we are not convinced of the scale of divergence priced and see scope for that to be pared back. The wage data released in November underlines the positive impact that should come from an improvement in real incomes and therefore consumer spending. Underlying inflation also remains elevated and ECB officials have continued to express concerns over sticky inflation. Services CPI on an annual basis has remained at around 4.0% for the last 12mths. Some ECB officials have expressed scepticism of current market pricing. While admittedly more of a hawk, ECB Executive Board member Schnabel stated on 25th November that she saw limited scope for further rate cuts. 10-year yields will likely initially go lower but should then stabilise and move higher as ECB rate cuts are less extensive than currently priced and moves are dictated by the US.

ECB POLICY RATE VS. 10YR GERMAN GOVT. YIELD

Source: Bloomberg, Macrobond

US TRADE DEFICIT WITH EURO-ZONE

Source: Bloomberg, Macrobond

Pound Sterling

|

Spot close 29.11.24 |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

EUR/GBP |

0.8307 |

0.8250 |

0.8200 |

0.8200 |

0.8300 |

|

GBP/USD |

1.2700 |

1.2360 |

1.2800 |

1.2930 |

1.3010 |

|

GBP/JPY |

191.06 |

190.40 |

194.60 |

193.90 |

192.60 |

|

Range |

Range |

Range |

Range |

||

|

GBP/USD |

1.2000-1.2800 |

1.2200-1.3100 |

1.2400-1.3300 |

1.2500-1.3500 |

MARKET UPDATE

In November the pound weakened notably against the US dollar in terms of London closing rates from 1.2872 to 1.2700. However, the pound strengthened against the euro from 0.8436 to 0.8307. The MPC at its meeting in November cut the key policy rate by 25bps to 4.75% following on from the 25bp cut in August which was the first after 14 consecutive rate increases through to August last year.

OUTLOOK

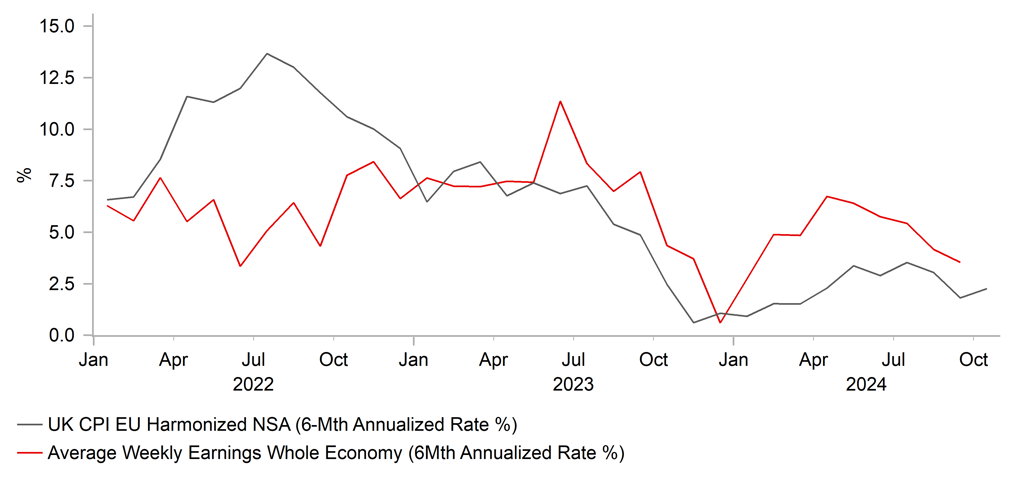

The pound depreciated further against the US dollar reflecting the broad dollar strengthening in response to the election victory for Donald Trump. Still, the pound managed to outperform the euro and most other G10 European currencies with the UK possibly better positioned to deal with the probable trade tariffs to be implemented by the Trump administration. The UK economy looks better positioned to cope and the rates divergence with the US has been more marginal. Indeed, through the next eight policy meetings through to Q4 2025 the OIS market is showing 75bps of cuts by both the Fed and the BoE. In contrast, the ECB is expected to cut by 165bps. The economy does look to have slowed after strong growth in 1H 2024 but the labour market data points to the potential for continued upside risks to inflation. Average hourly earnings accelerated on a 3mth YoY basis from 3.9% to 4.3% while core CPI on an annual basis picked up from 3.2% to 3.3% and services CPI remains elevated at 5.0%. The advance PMI data does point to a deterioration in business sentiment probably reflecting increased concerns over trade tariffs being implemented in the new year. There was also a likely negative impact from the government’s decision to increase the National Insurance Contribution rate for employers which could squeeze companies profit margins.

The market pricing on rates implying that the UK could be better positioned to deal with trade tariffs does make some sense. Two-thirds of UK exports to the US are services, and goods exports are equivalent to about 2.0% of UK GDP. Furthermore, analysing US trade statistics shows that the US is actually running a trade surplus with the UK, totalling USD 10bn over the 12 month period to September. While possibly better positioned we still expect the BoE to potentially cut by more than implied by current OIS market pricing. We see scope for 100bps of cuts once the BoE becomes more confident that inflation will ease further. While the direct impact of tariffs might prove less for the UK, the UK’s exposure to the euro-zone and elsewhere will see indirect impacts from US trade policies. Still, this implies one additional cut relative to current market pricing which is unlikely to have a dramatic impact on the performance of the pound. The front-loaded nature of the spending outlined in the budget should help offset weaker global growth conditions.

The low point in GBP/USD should come in 1H 2025 as trade tariff fears reach their peak. Current OIS pricing on ECB rate cuts (too much) and BoE cuts (too little) should mean EUR/GBP can drift modestly higher towards the end of 2025.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

Policy Rate |

4.75% |

4.50% |

4.00% |

3.75% |

3.75% |

|

3-Month Bill |

4.74% |

4.40% |

3.80% |

3.60% |

3.60% |

|

10-Year Yield |

4.24% |

4.20% |

4.10% |

4.20% |

4.40% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

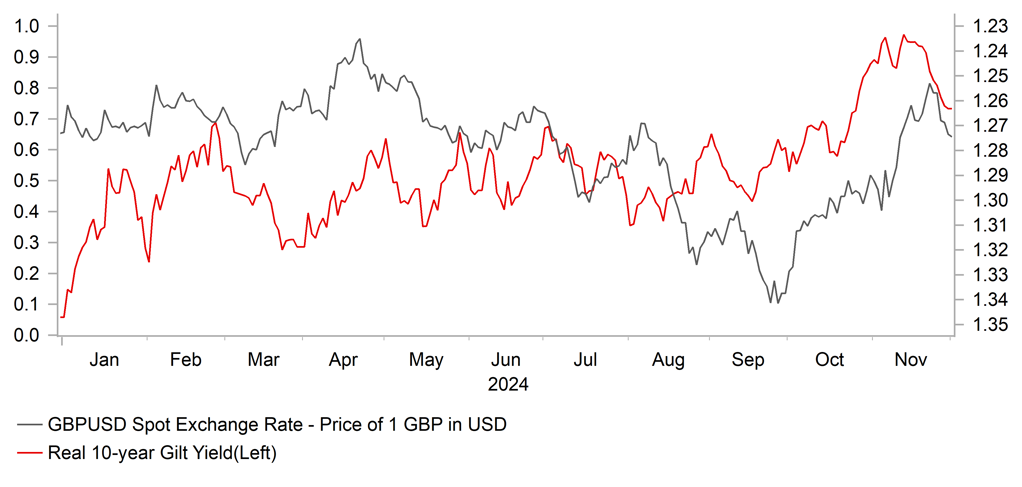

After jumping notably in October, the 10-year Gilt yield fell in November, by 21bps to close at 4.24%. The move lower was helped by a reversal in yields in the US as ‘Trump trades’ lost momentum. The big increase in government borrowing related to the budget announcement on 30th October could see Gilt yields remain more elevated through a widening in the term premium given the increased uncertainties. Overall borrowing over the course of the forecast period in the budget to 2029-30 is estimated to increase by GBP 142bn, which is hard for investors to ignore. But there are signs of moderating economic growth in some of the recent data and we continue to assume that over the coming 12 month period, inflation is set to slow by more than the BoE currently assumes. The latest Monetary Policy Report shows inflation accelerating to 2.8% in Q3 2025 before then moving lower to 2.2% by the end of 2026. This view of the inflation outlook is too pessimistic and we therefore see scope for the BoE delivering more than the current 75bps of cuts expected next year. If correct that will help reduce upside risks to longer-term yields, and we see scope for a modest decline in 10-year yields but yields then go higher in sympathy with the US.

GBP/USD VS. 10YR GILT YIELD

Source: Bloomberg, Macrobond

UK CPI VS. AVERAGE WEEKLY EARNINGS

Source: Bloomberg, Macrobond

Chinese renminbi

|

Spot close 29.11.24 |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

USD/CNY |

7.2440 |

7.4000 |

7.5000 |

7.5000 |

7.4000 |

|

USD/HKD |

7.7805 |

7.7900 |

7.7800 |

7.7700 |

7.7700 |

|

Range |

Range |

Range |

Range |

||

|

USD/CNY |

7.1000-7.6000 |

7.2000-7.7000 |

7.2000-7.7000 |

7.1000-7.6000 |

|

|

USD/HKD |

7.7700-7.8500 |

7.7600-7.8400 |

7.7600-7.8400 |

7.7500-7.8300 |

MARKET UPDATE

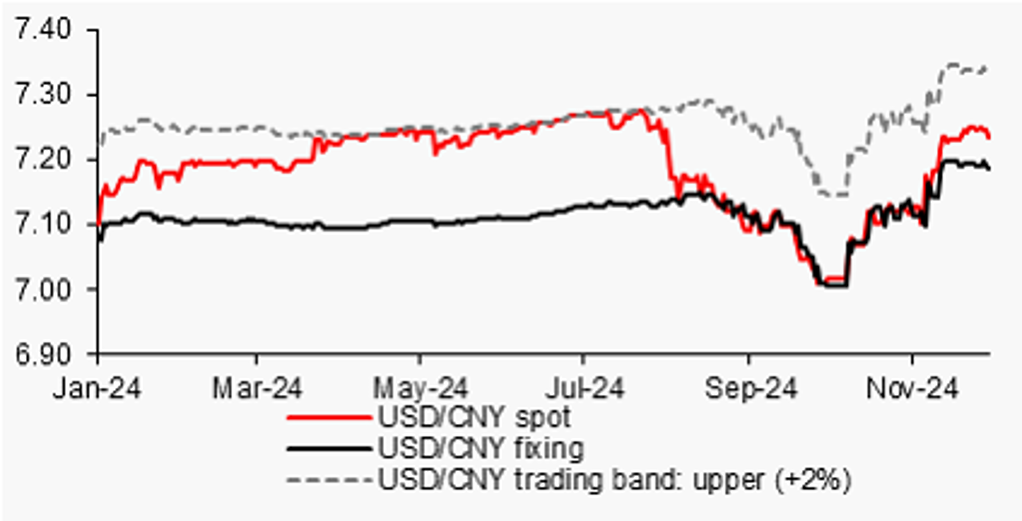

In November, USD/CNY increased from 7.1162 to 7.2440. On 20th November, the PBoC kept the 1Y and 5Y LPR at 3.10% and 3.60% respectively, after cutting 25bps in the month earlier. The PBoC also kept 1Y MLF rate steady at 2%. Speaking at the Financial Street Forum in Beijing on 18th October, Governor Pan mentioned the possibility of another 25bps-50bps RRR cut by year-end depending on the liquidity condition.

OUTLOOK

October’s major macroeconomic data was mixed, with an improving retail sales growth and persisting weak performance of the property sector. China’s retail sales surprised the market to the upside in October, thanks to the support from the consumer goods trade-in program. However, despite a jump in retail sales growth, the consumer price inflation remained subdued. October industrial profits remained under pressure with three consecutive months of negative growth, partly due to intensifying PPI deflation. Meanwhile, October IP growth slowed while FAI YTD growth remained unchanged from prior the month’s low level. The lukewarm recovery pace of the Chinese economy requires additional stimulus especially fiscal policies. The local government debt-swap program (RMB 6tn) was introduced on 8th November to defuse the hidden debt risk and free up resources of local governments for development in strategic areas and improving people’s livelihood. Looking forward, we do expect the government to introduce more incremental policies, including “forceful” fiscal policy next year as pointed out by Finance minister Lan, among others. The government may push out more consumption-related stimulus such as expanding the existing consumer goods trade-in program.

US tariffs on imports from China clouds the prospect of China’s economic recovery and USD/CNY. With Trump’s victory and the GOP’s red sweep in both the US Senate and House, compared with the case in Trump’s first term when the tariffs was launched more than one year after Trump took the office, the Trump 2.0's tariff progress likely will be significantly faster. We are assuming a phased tariff on China goods, with that assumption consistent with Trump’s recent threats of imposing an additional 10% tariff on imports from China. Trump will certainly not stop there, as the US trade deficit is still running large with China and the direction of the US-China relationship is unlikely to be turned. The outlook for USD/CNY heavily depends on the assumptions of the magnitude of the tariff and the timing of the tariffs on China exports to the US. Our forecasts of USD/CNY reflect our assumption of an extra 20ppts increase of tariffs, and a timing of phased tariff implementation in Q2 or Q3 2025. Having said that, should the Chinese government roll out significant extra stimulus to combat the negative impact caused by the tariffs, CNY may need not to depreciate as much to balance the economy. We are not ruling out the possibility of PBOC’s intervention to shore up the CNY as well. We expect USD/CNY to reach 7.3000 by the end of this year.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q1 2025 |

Q2 2025 |

Q3 2025 |

Q4 2025 |

|

|

LPR 1Y |

3.10% |

2.90% |

2.90% |

2.90% |

2.90% |

|

MLF 1Y |

2.00% |

1.70% |

1.70% |

1.70% |

1.70% |

|

7-Day Repo Rate |

1.50% |

1.30% |

1.30% |

1.30% |

1.30% |

|

10-Year Yield |

2.03% |

1.95% |

1.90% |

2.00% |

2.10% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

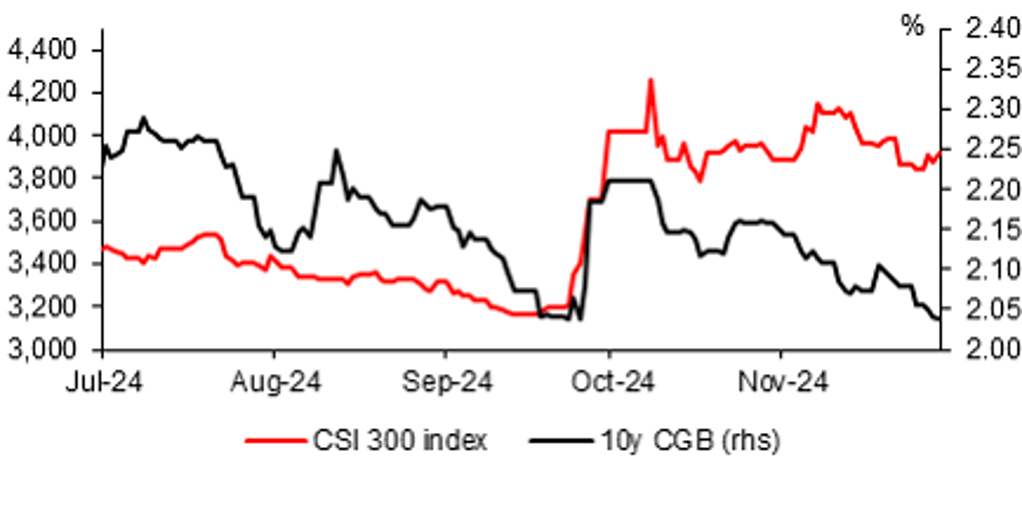

China’s government bond yields shifted lower in November. So far, fiscal efforts have been more concentrated on dealing with local governments’ hidden debt risks. There certainly is an expectation of further incremental fiscal support to work on investment and consumption directly. But the size of it is unlikely to be generous enough to reverse the current trend of declining government bonds yields, in our view. We expect a more moderate 4.5% real GDP growth for 2025 compared with this year’s growth of 5%. Such a profile of lower medium GDP growth expectation and persisting low consumer price inflation, combined with a further relaxation of monetary policies including an RRR cut and policy rate cut, will likely send China’s real rates lower and keep investors' enthusiasm sustained for bonds at least for couple quarters. The risk aversion caused by tariffs could help keep bond yields low as well. We expect the PBoC to cut the RRR by another 25bps to 50bps in December to ease the liquidity conditions given the upcoming sizeable maturities of existing PBoC instruments (MLF, 7-day reverse repo) and a year-end seasonal liquidity squeeze. We expect the 10-year CGB yield to edge lower until mid-2025, before tilting up slightly in 2H 2025.

USD/CNY FIXING HAS BEEN ADJUSTED HIGHER BY PBOC SINCE MID-NOV

Source: : Bloomberg, MUFG GMR

SENTIMENT WEAKENED AGAIN AS ECONOMIC RECOVERY REMAINS SLOW

Source: : Bloomberg, MUFG GMR