Please download PDF from above for the following currencies.

Australian dollar // New Zealand dollar //Canadian dollar // Norwegian krone // Swedish Krona // Swiss franc // Czech koruna // Hungarian forint //Polish zloty // Romanian leu // Russian rouble // South African rand // Turkish lira // Indian rupee // Indonesian rupiah // Malaysian ringgit // Philippine peso //Singapore dollar // South Korean won // Taiwan dollar // Thai baht // Vietnamese dong // Argentine peso // Brazilian real // Chilean peso // Mexican peso // Crude oil // Saudi riyal // Egyptian pound

Monthly Foreign Exchange Outlook

DEREK HALPENNY

Head of Research, Global Markets EMEA and International Securities

Global Markets Research

Global Markets Division for EMEA

E: derek.halpenny@uk.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

E: lee.hardman@uk.mufg.jp

LIN LI

Head of Global Markets Research Asia

Global Markets Research

Global Markets Division for Asia

E: lin_li@hk.mufg.jp

MICHAEL WAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: michael_wan@sg.mufg.jp

LLOYD CHAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: lloyd_chan@sg.mufg.jp

EHSAN KHOMAN

Head of Commodities, ESG and Emerging Markets Research – EMEA

DIFC Branch – Dubai

E: ehsan.khoman@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

July 2024

KEY EVENTS IN THE MONTH AHEAD

1) FOMC & BOJ MEETINGS IN FOCUS

The US dollar was the best performing currency in the first half of 2024 followed closely behind by the pound. The US dollar gained in June as well with some help from uncertainties abroad including the French parliamentary elections. The monetary policy focus in July will very much be on the final day of the month when the BoJ and then the FOMC hold monetary policy meetings. The BoJ remains very cautious over changing its monetary stance but we expect to see a rate hike and the details of the already announced plan to slow the pace of JGB purchases. The failure to announce that plan in June provided added encouragement to sell the yen so the actions in July are important in helping to provide support for the yen given USD/JPY in June hit the highest level since 1986. BoJ action in itself will probably not be enough to turn the yen stronger and hence the FOMC decision, and more importantly the guidance of future policy action will be key for the dollar. We suspect we are a lot closer to a clearer downturn in the jobs market in the US and if evidence of this becomes more compelling, as we expect, then the FOMC should be in a better position to signal the potential for a rate cut in September. We expect the dollar to weaken in the second half of the year, although by less than previously assumed.

2) POLITICS IN EUROPE – BUT FRANCE IS KEY

There is some relief after the first round of the France parliamentary elections revealed a very large number of constituencies in which three candidates have reached the second round on 7th July. A turnout of 67% was much larger than in 2022 (48%) and the greater opportunity for alliances against Marine Le Pen’s National Rally reduces the risk of an outright majority. Some form of hung parliament seems most likely which while not a positive outcome is better than some of the alternative scenarios. Near-term EUR risks remain to the downside but as we progress through the year, the scale of Fed rate cuts we expect relative to current market pricing should allow EUR/USD to move higher. We see the Labour Party winning a large majority in the UK general election on 4th July. We have raised our GBP forecasts in part on better political stability ahead and in part on the signs of a stronger rebound in economic growth than we previously expected.

3) CHINA’S THIRD PLENUM IS KEY TO WATCH

The much-delayed third plenum is confirmed to be held in mid-July. According to the party’s official newspaper, China will continue to implement reforms. While we do not expect much drastic new ideas of reforms to be rolled out, due to that President Xi’s vision of a modern China had long been laid out since he took power in 2013, prioritizing on “most urgent things” could offer positive surprises, in our view. China’s economy is suffering lingering low confidence, and a still contracting property sector. The messages coming out of the meeting and answering the question of how to achieve his vision, such as “high-quality development” and “Chinese modernisation” and help to stabilize the growth in near term, could also stimulate positive sentiment.

Forecast rates against the US dollar - End-Q3 2024 to End-Q2 2025

|

Spot close 28.06.24 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

JPY |

160.84 |

154.00 |

152.00 |

150.00 |

148.00 |

|

EUR |

1.0717 |

1.0800 |

1.0900 |

1.1200 |

1.1200 |

|

GBP |

1.2642 |

1.2860 |

1.2980 |

1.3250 |

1.3180 |

|

CNY |

7.2670 |

7.2200 |

7.1800 |

7.1500 |

7.1000 |

|

AUD |

0.6677 |

0.6700 |

0.6800 |

0.6950 |

0.7100 |

|

NZD |

0.6094 |

0.6100 |

0.6200 |

0.6300 |

0.6300 |

|

CAD |

1.3683 |

1.3600 |

1.3400 |

1.3200 |

1.3000 |

|

NOK |

10.651 |

10.463 |

10.275 |

9.8210 |

9.6430 |

|

SEK |

10.589 |

10.556 |

10.367 |

10.000 |

9.8210 |

|

CHF |

0.8984 |

0.8940 |

0.8990 |

0.8840 |

0.8930 |

|

|

|

|

|

|

|

|

CZK |

23.364 |

23.150 |

23.120 |

22.680 |

22.770 |

|

HUF |

368.23 |

366.70 |

367.00 |

360.70 |

364.30 |

|

PLN |

4.0193 |

3.9540 |

3.9630 |

3.8840 |

3.9110 |

|

RON |

4.6408 |

4.6200 |

4.6060 |

4.5090 |

4.5270 |

|

RUB |

86.032 |

87.840 |

88.420 |

88.240 |

91.080 |

|

ZAR |

18.243 |

18.300 |

18.200 |

17.900 |

17.700 |

|

TRY |

32.794 |

34.250 |

35.500 |

37.000 |

38.000 |

|

|

|

|

|

|

|

|

INR |

83.385 |

83.500 |

83.000 |

82.500 |

82.800 |

|

IDR |

16370 |

16420 |

16360 |

16150 |

16030 |

|

MYR |

4.7160 |

4.7500 |

4.6000 |

4.5700 |

4.5300 |

|

PHP |

58.588 |

59.000 |

58.700 |

58.500 |

58.000 |

|

SGD |

1.3553 |

1.3350 |

1.3200 |

1.3000 |

1.2900 |

|

KRW |

1376.3 |

1385.0 |

1370.0 |

1345.0 |

1325.0 |

|

TWD |

32.430 |

32.400 |

32.000 |

31.700 |

31.400 |

|

THB |

36.725 |

35.700 |

35.300 |

35.000 |

34.700 |

|

VND |

25454 |

25600 |

25700 |

25700 |

25700 |

|

|

|

|

|

|

|

|

ARS |

911.87 |

970.00 |

1350.00 |

1425.0 |

1500.0 |

|

BRL |

5.5414 |

5.8000 |

5.7000 |

5.6000 |

5.4000 |

|

CLP |

940.71 |

960.00 |

970.00 |

930.00 |

890.00 |

|

MXN |

18.258 |

18.200 |

18.400 |

18.100 |

17.700 |

|

|

|||||

|

Brent |

86.40 |

88.00 |

93.00 |

95.00 |

91.00 |

|

NYMEX |

81.43 |

83.00 |

88.00 |

90.00 |

86.00 |

|

SAR |

3.7516 |

3.7500 |

3.7500 |

3.7500 |

3.7500 |

|

EGP |

47.995 |

47.600 |

47.300 |

47.100 |

46.600 |

Notes: All FX rates are expressed as units of currency per US dollar bar EUR, GBP, AUD and NZD which are expressed as dollars per unit of currency. Data source spot close; Bloomberg closing rate as of 4:30pm London time, except VND which is local onshore closing rate.

US dollar

|

Spot close 28.06.24 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

USD/JPY |

160.84 |

154.00 |

152.00 |

150.00 |

148.00 |

|

EUR/USD |

1.0717 |

1.0800 |

1.0900 |

1.1200 |

1.1200 |

|

Range |

Range |

Range |

Range |

||

|

USD/JPY |

150.00-165.00 |

148.00-163.00 |

146.00-161.00 |

144.00-159.00 |

|

|

EUR/USD |

1.0300-1.1100 |

1.0400-1.1300 |

1.0500-1.1500 |

1.0700-1.1700 |

MARKET UPDATE

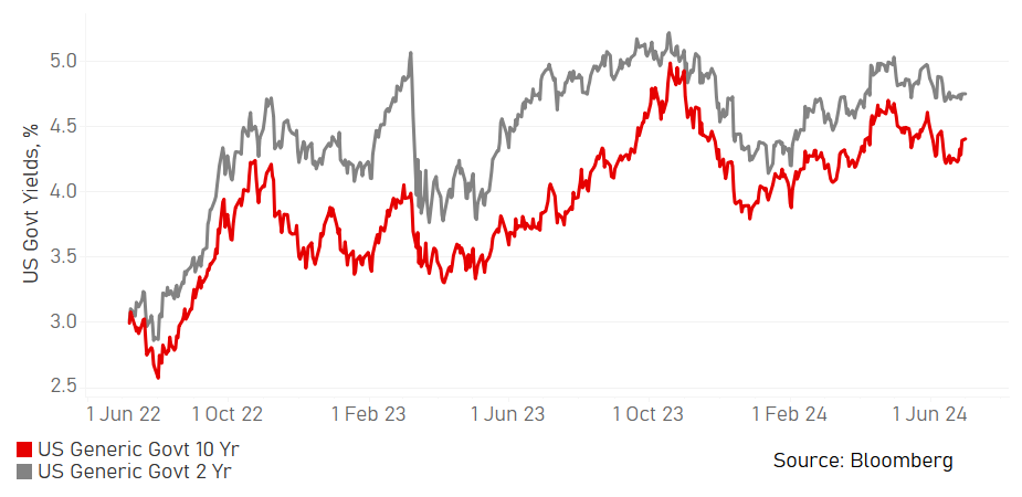

In June the US dollar strengthened against the euro in terms of London closing rates, from 1.0846 to 1.0717. In addition, the dollar strengthened against the yen, from 157.22 to 160.84. The FOMC at its meeting in June left the fed funds rate unchanged in a range of 5.25% to 5.50%. The FOMC continued with its policy of reducing its securities holdings with QT ongoing but at a reduced rate of USD 60bn per month through a reduction in UST bond holdings from USD 60bn to USD 25bn. The pace of reduction in the holdings of MBS remains at USD 35bn per month. The FOMC reduced its median dot profile for 2024 from three rate cuts to just one.

OUTLOOK

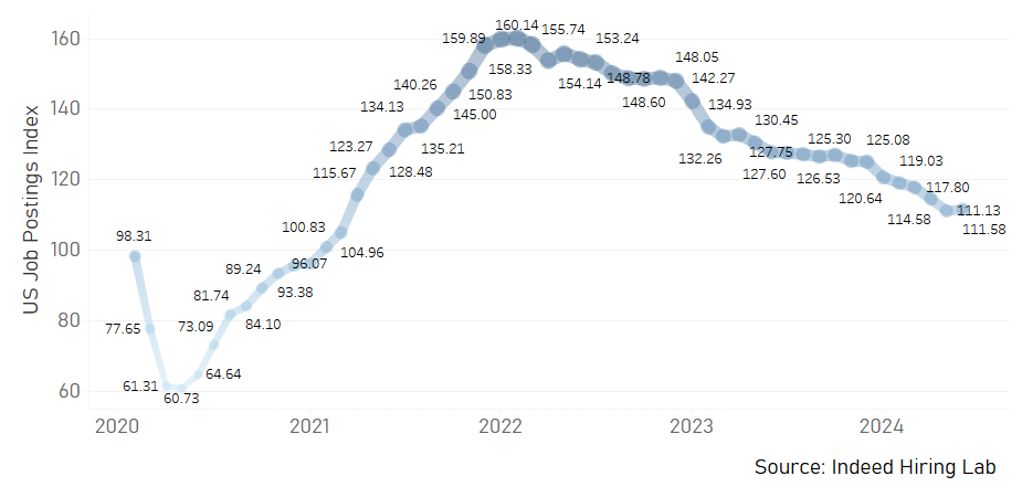

The US dollar advanced in June although for reasons less common than what usually drives the dollar. The 2-year UST bond yield fell in June, by 12bps as investors responded to the weak US inflation print and growing evidence of a weakening labour market. This did not have negative implications for the dollar for a few reasons. Firstly, front-end yields in core Europe also fell sharply, and by slightly more than in the US in response to the uncertainty triggered by the decision to hold snap elections in France. Secondly, the BoJ’s decision to hold-off on changing its JGB buying policy fuelled a renewed bout of yen selling and new USD/JPY highs not seen since 1986. So international factors came to the rescue for the dollar. We would still view the drop in US yields as telling and indicative of investors growing more confident about easing US inflation pressures and scope for Fed easing. Most labour market indicators continue to point to easing labour demand. Continued claims hit the highest level since November 2021, Challenger layoffs are at higher levels than pre-covid while ISM services employment index readings point to softer jobs growth ahead which we believe will inevitably show up in NFP data over the coming months.

Weaker jobs growth in the NFP data will be we believe a crucial turning point for rates and the dollar. Fed officials by and large continue to happily push the ‘higher for longer’ rhetoric arguing for caution on cutting rates. The main factor holding the Fed back from cutting is the labour market and wage growth keeping core inflation ‘sticky’. But AHE YoY growth is at 4.1% without much weakness in NFP and a rate of 3.5% is viewed as broadly consistent with price stability. The Fed could pivot quite quickly once the jobs data turns. Fed President Daly did state we could be approaching an “inflection point” for the labour market while Fed President Goolsbee stated the Fed needs to be mindful of leaving policy too restrictive. We believe the FOMC will cut in September and at the final two meetings of the year in Q4.

On the basis of three cuts delivered this year, there is plenty of downside scope for front-end yields with weakening data likely to also increase expectations on the extent of easing in 2025 as well. However, we have raised our US dollar levels for Q3 and Q4 (previously EUR/USD 1.1000 & 1.1200) given the near-term downside risks and given the increased probability of a Trump victory in November.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

Policy Rate |

5.33% |

5.13% |

4.63% |

4.13% |

3.63% |

|

3-Month T-Bill |

5.35% |

5.00% |

4.38% |

3.88% |

3.63% |

|

10-Year Yield |

4.40% |

4.25% |

4.13% |

4.00% |

4.00% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

An update on the timing of the first Fed cut: Post the hawkish leaning SEP update at the June FOMC meeting, in which Fed forecasters only pencilled in one cut for 2024, along with Chair Powell’s more hawkish than usual tone at the presser, resulted in us pushing back our call for the Fed’s first cut to September (from July). For what it is worth, we were one of the last holdouts for an initial cut in July, largely because we have been of the view that the Fed should be pre-emptive on normalization rather than having to cut aggressively later on (especially if the aim is to stick to the soft landing). We assume data will continue to soften and although risk assets are in a melt-up phase, which can just as easily roll over at any moment triggering cuts ahead. We analysed the typical start time and size for the first cut by cataloguing the historical first cuts. We found that the Fed tends to launch cuts during summer (many first cuts took place in June/July/September). Our take on that is by mid-year, if the economy isn’t performing as expected, the Fed will start to ease (like now). Lastly, even when we exclude the 1970s/80s, the average first cut is 44bps, so if economic conditions were to weaken quickly, 50bp cuts are possible too.

(George Goncalves)

US JOB POSTINGS INDEX

US GOVERNMENT BOND YIELDS

Japanese yen

|

Spot close 28.06.24 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

USD/JPY |

160.84 |

154.00 |

152.00 |

150.00 |

148.00 |

|

EUR/JPY |

172.37 |

166.30 |

165.70 |

168.00 |

165.80 |

|

Range |

Range |

Range |

Range |

||

|

USD/JPY |

150.00-165.00 |

148.00-163.00 |

146.00-161.00 |

144.00-159.00 |

|

|

EUR/JPY |

161.00-177.00 |

159.00-176.00 |

158.00-175.00 |

157.00-174.00 |

MARKET UPDATE

In June the yen weakened versus the US dollar in terms of London closing rates from 157.22 to 160.84. The yen weakened much more modestly versus the euro, from 170.52 to 172.37. The BoJ, at its meeting in June left its monetary stance unchanged after the major changes announced in March that essentially brought to an end the QQE/NIRP policy framework adopted in 2013 (QQE) and enhanced in 2016 (NIRP). With the BoJ now paying 0.10% on excess reserves, the unsecured overnight call rate closed at 0.08%. The BoJ did pre-announce in June its plan to slow the pace of JGB buying each month from the current rate of “around JPY 6trn”.

OUTLOOK

The yen weakened notably in June and broke above the levels where intervention took place toward the end of April when USD/JPY briefly broke the 160-level. USD/JPY has now reached levels last traded in 1986 with yen selling momentum remaining strong given the broader drivers of yen weakness have not changed. At the root of the yen’s problems is the very deep negative policy rate in real terms. The level at over -200bps is the deepest negative level since 1998 when the Japanese authorities were last intervening to buy the yen.

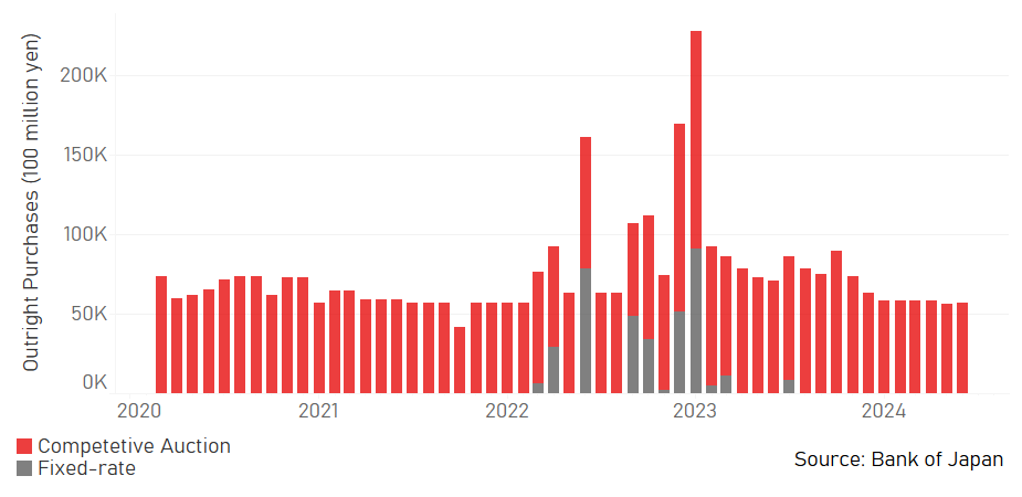

There had been high expectations that the BoJ would announce a plan to slow its monthly purchases of JGBs. The fact that the BoJ failed to do this and instead confirmed that a plan would be revealed at the next meeting in July only served to reinforce the perception of the BoJ moving to alter its policy stance at a snails’ pace. It once again revealed possible divisions between the BoJ and the MoF which has intervened to halt yen weakness. It is not surprising given the BoJ meeting in June that the yen has hit new lows. It is unlikely that circumstances are going to change notably that would warrant a change in expectations of yen direction. Lows have been hit across many currencies as investors likely view global central banks as only gradually cutting policy rates given the ongoing evidence of sticky inflation.

We are maintaining our view that the BoJ will raise the key policy rate range by 15bps and reveal a plan to slow JGB purchases. Given the behaviour so far from the BoJ on altering its policy stance it seems likely that the plan will likely reveal a very slow, cautious pace of decline in the monthly purchase pace. A quarterly reduction of JPY 0.3trn per quarter or only a little over JPY 1trn per year could be the scale of caution to expect. If the pace is in this ballpark that would unlikely result in any notable reaction in the JGB market. Yields could in fact decline initially although we would expect the rate hike, which is not currently expected, to help limit a JGB yield decline and should help to provide some initial moderate support for the yen.

The weakness of the yen has extended beyond our expectations with the BoJ more cautious than expected and the Fed remaining more hawkish for longer. We still expect this mix to change, which will help result in a turn stronger for the yen.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

Policy Rate |

-0.10% |

0.25% |

0.25% |

0.50% |

0.50% |

|

3-Month Bill |

0.02% |

0.30% |

0.30% |

0.60% |

0.60% |

|

10-Year Yield |

1.06% |

1.10% |

1.20% |

1.30% |

1.40% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year JGB yield initially fell in June but then recovered, ending June close to unchanged, down just 1bp at 1.06%. This was a telling performance though considering the drop in UST bond yields in June, it marked the second consecutive month of narrowing for the 10-year US-JP 10yr yield spread. The narrowing totalled 10bps. This underlines the fact that while the FX markets do not show any impact from the changing stance of the BoJ, the JGB market does. Even given the disappointment of delaying the plan to reduce JGB purchases, yields finished unchanged and does underline risks ahead given the changing BoJ stance. The market is still only priced at about 40% for a 15bp rate hike in July (our expectation) and hence we see scope for yields to move further higher. When asked about whether rates could be lifted at the same meeting as the JGB buying reduction plan is revealed, Governor Ueda stated “yes, of course”. The depreciation of the yen will add to prospects of a rate hike while diminishing labour supply will help keep wage growth stronger. Ultimately, we expect the 10-year JGB yield to drift further higher.

CFTC JPY ASSET MANAGER POSITIONING

BOJ’S MONTHLY PURCHASES OF JGBS

Euro

|

Spot close 28.06.24 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

EUR/USD |

1.0717 |

1.0800 |

1.0900 |

1.1200 |

1.1200 |

|

EUR/JPY |

172.37 |

166.30 |

165.70 |

168.00 |

165.80 |

|

Range |

Range |

Range |

Range |

||

|

EUR/USD |

1.0300-1.1100 |

1.0400-1.1300 |

1.0500-1.1500 |

1.0700-1.1700 |

|

|

EUR/JPY |

161.00-177.00 |

159.00-176.00 |

158.00-175.00 |

157.00-174.00 |

MARKET UPDATE

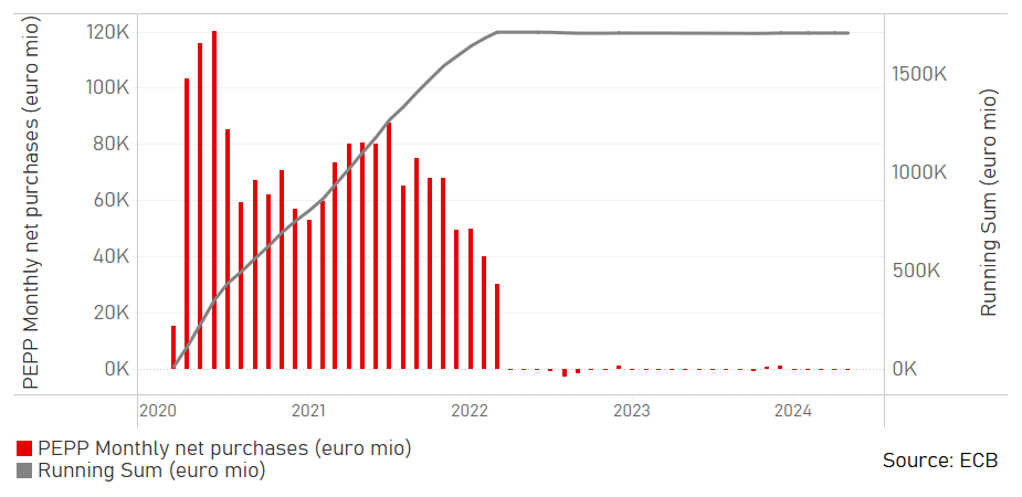

In June the euro weakened versus the US dollar in terms of London closing rates, moving from 1.0846 to 1.0717. At its meeting in June, the ECB cut the key policy rate by 25bps to 3.75%, the first cut after 450bps of rate hikes through to September last year. The ECB is running down APP securities and will commence PEPP run-off in 2H with an estimated EUR 380bn of securities rolling off the balance sheet from both programs combined in 2024.

OUTLOOK

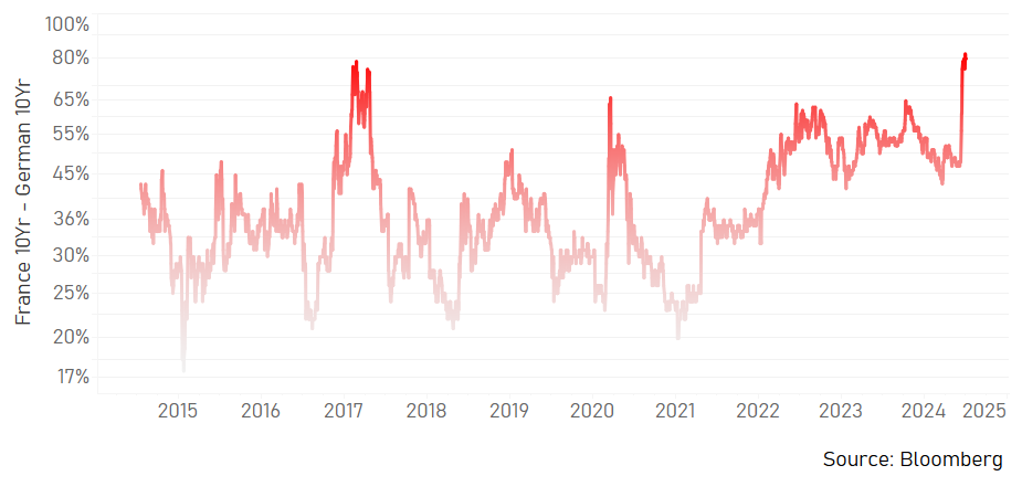

The decision from President Macron to hold snap parliamentary elections was what you can call ‘left-field’ and has skewed the near-term risks clearly to the downside. The first round results from 30th June have confirmed what had been expected but with some positives. Turnout was significant; 67% versus 48% in 2022 and what this resulted in was a larger number of constituencies in which three candidates will compete in Sunday’s second round. Marine Le Pen’s RN was the clear winner as expected with New Popular Front second and Macron’s Ensemble third. The choice of three candidates has opened up the prospect of alignments against RN with that makes it much less likely that RN can obtain an overall majority. That was a plausible scenario that would have sent OAT yields higher and EUR/USD down through the 1.0500-level quickly. Still, RN has watered down numerous policies and both Marine Le Pen and Jordan Bardella have emphasised a willingness to work with President Macron and a desire to ensure stability in order to support businesses and economic growth. RN has also committed to a full audit of France’s finances before deciding on the extent and timing of some previous promises, including reducing the pension age. A hung parliament seems most likely and it may be some time before it becomes clear on whether a government can be formed.

We have lowered our EUR/USD forecasts for Q3 and Q4 (previously 1.10 & 1.12) in part due to the elections risks above that could propel the euro lower over the near-term. A Trump victory in November is now also more likely. However, the relative macro outlook has not really changed and for that reason, we still show a gradual move higher for EUR/USD. The ECB we believe will cut twice more this year with inflation at more benign levels and OIS pricing is close to priced for this outcome. However, US pricing remains much lower than the three Fed rate cuts we expect and hence we do not expect to see any divergence from here favouring the US. The ECB is also set to launch its wind-down of PEPP securities that will speed up balance sheet shrinkage at the same time as the Fed is slowing balance sheet shrinkage.

We are mindful of the obvious downside risks for EUR/USD over the short-term but based on our assumption of an RN victory but one that falls short of an overall majority we do not expect a sustained extended EUR/USD sell-off. More Fed rate cuts than currently priced for this year remains the overall crucial assumption that allows for some modest increases in EUR/USD going forward.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

Policy Rate |

3.75% |

3.50% |

3.25% |

3.00% |

2.75% |

|

3-Month Bill |

3.71% |

3.45% |

3.15% |

2.90% |

2.70% |

|

10-Year Yield |

2.50% |

2.50% |

2.40% |

2.30% |

2.30% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year bund yield fell notably in June, by 16bps to close at 2.50%. The catalyst was the snap election announcement by President Macron – the 10-year core yield fell 26bps in the six trading days following the announcement. That same period also saw weaker than expected US inflation data so there were external factors driving the decline in yields in Germany as well. Strong OAT selling after the second round of elections is a possibility that could extend the drop in German yields so a period of volatility seems likely over the short-term. However, assuming a sell-off is contained and relatively brief, the main driver going forward will be inflation and ECB policy decisions. Based on continued more favourable inflation we continue to expect the ECB to cut rates gradually – 25bps at each forecast meeting that will help to gradually lower long-term yields as well. PEPP securities will commence rolling off the ECB’s balance sheet in July with APP roll-offs continuing so this will act to limit the move lower in long-term rates and steepen the 2s10s yield curve. The France election uncertainty is unlikely to completely reverse but we assume limited overall impact in the end on Bund yields.

FRANCE-GERMAN 10YR GOVT. YIELD DIFFERENTIAL

HISTORY OF MONTHLY NET PURCHASE UNDER THE PEPP

Pound Sterling

|

Spot close 28.06.24 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

EUR/GBP |

0.8477 |

0.8400 |

0.8400 |

0.8450 |

0.8500 |

|

GBP/USD |

1.2642 |

1.2860 |

1.2980 |

1.3250 |

1.3180 |

|

GBP/JPY |

203.33 |

198.00 |

197.20 |

198.80 |

195.00 |

|

Range |

Range |

Range |

Range |

||

|

GBP/USD |

1.2200-1.3200 |

1.2300-1.3300 |

1.2400-1.3500 |

1.2500-1.3600 |

MARKET UPDATE

In June the pound weakened against the US dollar in terms of London closing rates from 1.2725 to 1.2642. However, the pound strengthened against the euro, from 0.8523 to 0.8477. The MPC at its meeting in June left the key policy rate unchanged at 5.25%, following 14 consecutive rate increases through to August last year before commencing a pause from September.

OUTLOOK

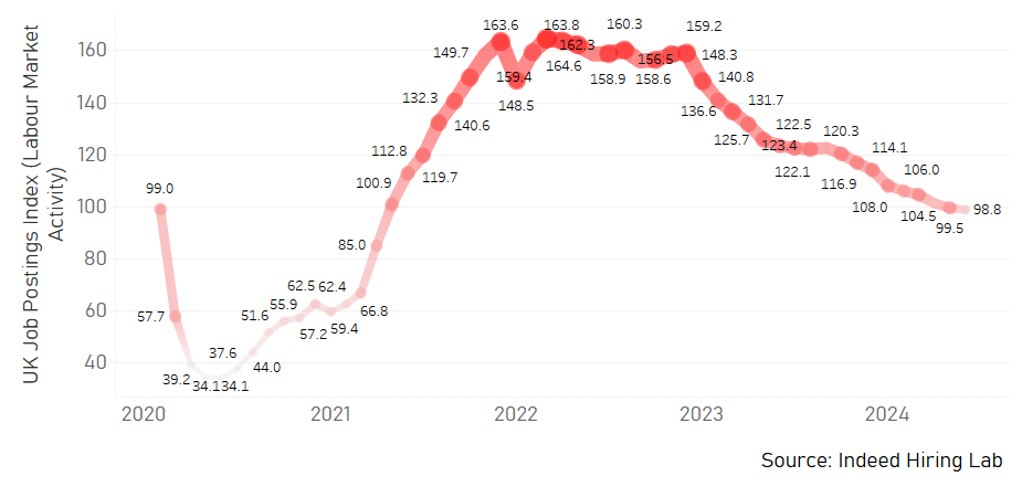

The pound weakened versus the US dollar but advanced versus the euro mainly reflecting the increased political risks in France. Politics is also in focus in the UK and the prospect of the Labour Party winning a large majority in the general election on 4th July is certainly helping to define a clear distinction with Europe. The polling at the end of June did show Labour losing some support but the Tories lost support too with both Reform and the Liberal Democrats the beneficiaries. The economic policies put forward by Labour are very cautious and the strategy is clearly to strengthen trust with voters that it can govern and manage the economy. Labour have only outlined GBP 7.35bn of new spending to be financed primarily by closing tax loopholes on wealthy non-domiciled individuals and introducing VAT on private education fees. Labour remain about 20ppts ahead of the Tories with MRP polls signalling potentially huge majorities. We certainly assume better political stability is on its way with Labour intending to focus on ‘wealth creation’ through cutting red-tape and procedures to help boost business confidence.

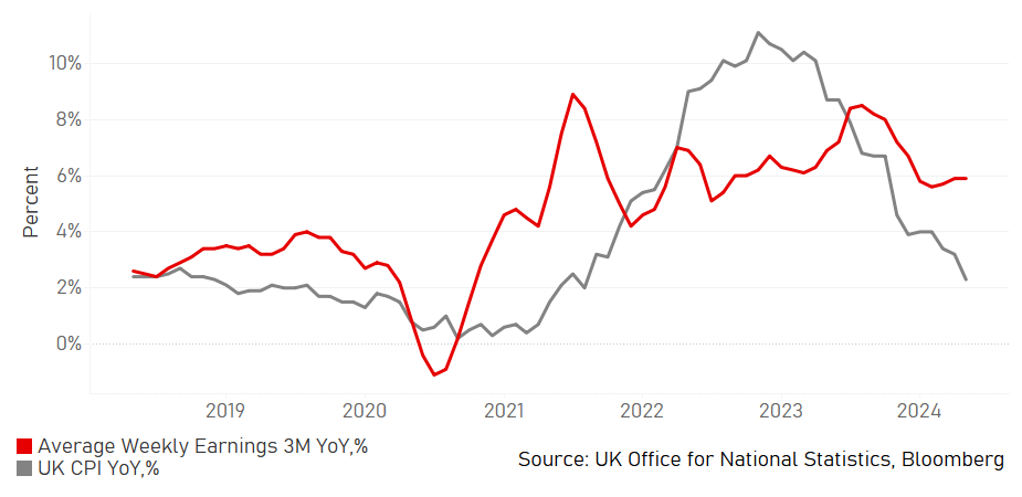

The YoY CPI rate hit the BoE’s 2.0% target in May for the first time since July 2021 and has declined from 11.1% in October 2022. The scale of this drop in of itself is worthy of some monetary easing and we maintain our view that the MPC will vote to cut in August. We see one further cut this year, in November, one less than previously given the better growth pick-up than we previously assumed. The CPI base effect is unfavourable in the coming months and YoY CPI is set to move higher. There are also growing signs of a clear pick-up in both consumer and business confidence. Falling inflation is boosting real incomes that has resulted in real GDP accelerating. These positive developments strengthen the case for a scenario of a gradual growth pick-up that coincides with inflation declining back to target in 2025 following a moderate pick-up this year. Weaker labour demand will help to slow wage growth going forward that will be key to weaker underlying services inflation.

Our previous GBP/USD end-forecast (Q1 2025) has been increased by around 3.0% reflecting our increased confidence over the return of price stability and the ability of the MPC to lower rates as real GDP picks up. The pace of cuts by the MPC will now be a little less than the Fed or ECB and hence MPC action will have a modest supportive FX impact. We also assume a large majority for the Labour Party that will allow for bolder moves on improving business conditions and increase prospects of improving relations with the UK’s main trading partner – the EU.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

Policy Rate |

5.25% |

5.00% |

4.75% |

4.50% |

4.25% |

|

3-Month Bill |

5.27% |

4.95% |

4.70% |

4.40% |

4.20% |

|

10-Year Yield |

4.17% |

4.20% |

4.00% |

3.90% |

3.80% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The 10-year Gilt yield declined by 15bps to close at 4.17%, a little bit more than the decline in UST bond yields. The MPC meeting in June was important and has certainly strengthened our conviction on a rate cut being delivered in August. The MPC voted again 7-2 to hold rates steady but for “some” of the seven to vote to hold the decision was a close call. Assuming there is no big inflation upside surprise, a rate cut should be delivered in August along with potentially two further cuts in November and December. The risk is the MPC cuts less and services inflation and wage growth remain the areas of greatest concern for the MPC. But labour demand is weakening and there has been a drop in the PAYE employment data in three of the last four months with the median wage rate slowing. Assuming two-to-three cuts this year and four in 2025 would get the policy rate much closer to the rough estimate of the equilibrium policy rate of between 3.00%-3.50%. The market is currently priced for around 115-120bps of easing by the end of next year , so we see scope for front-end yields to drop more which will help lower the 10-year yield as well (but by less resulting in a steepening of the curve) to around the 3.50% level by mid-2025.

UK JOB POSTINGS INDEX

WEEKLY EARNINGS 3M YOY,% VS. UK CPI YOY, %

Chinese renminbi

|

Spot close 28.06.24 |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

USD/CNY |

7.2670 |

7.2200 |

7.1800 |

7.1500 |

7.1000 |

|

USD/HKD |

7.8081 |

7.8000 |

7.7900 |

7.7800 |

7.7700 |

|

Range |

Range |

Range |

Range |

||

|

USD/CNY |

7.0500-7.3300 |

7.0000-7.3200 |

6.9500-7.3100 |

6.9000-7.3000 |

|

|

USD/HKD |

7.7700-7.8400 |

7.7600-7.8300 |

7.7600-7.8300 |

7.7500-7.8200 |

MARKET UPDATE

In June, USD/CNY increased from 7.2421 to 7.2670. The PBOC kept the 1-year MLF stable at 2.50% on 17th June and held both its 1-year LPR rate and 5-year LPR rate unchanged at 3.45% and 3.95% respectively on 27th June. On 19th June, Pan Gongsheng, governor of the People's Bank of China, pointed out at the 2024 Lujiazui Forum that China's monetary policy stance is supportive and provides financial support for the continued recovery of the economy. And in the near-term, the governor said that some measures to regulate market behaviour will have a "squeezing out" effect on financial aggregate data, but this does not mean a change in the stance of monetary policy, and it should be more conducive to improving the transmission efficiency of monetary policy.

OUTLOOK

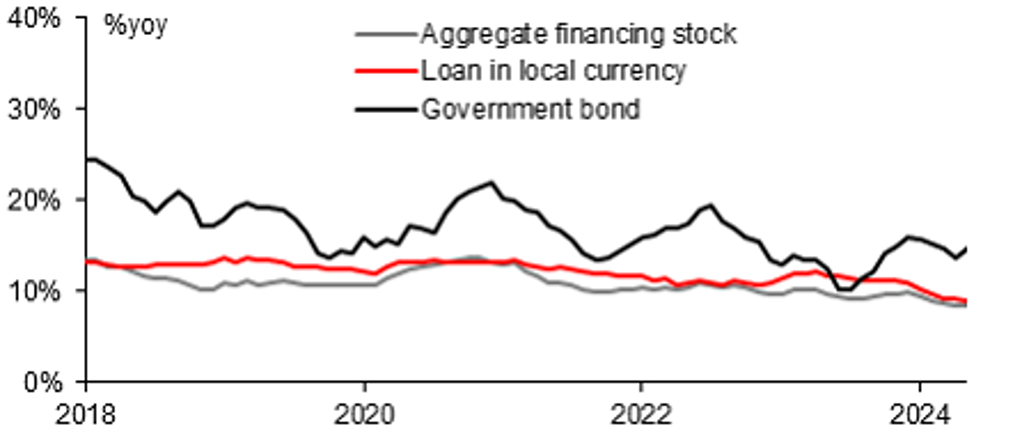

In June, amid a 1.1% appreciation of the US dollar, measured by the DXY index, CNY weakened by 0.34% against the dollar. The continued strength of the dollar (due to the postponing of Fed’s policy rate cut, weakness in EUR and JPY, and still better economic fundamentals in the US compared to Europe) explained a significant portion of the CNY’s depreciation. CNY’s depreciation against the dollar in June was passive to some degree. Having said that, CNY also suffered from the negative market sentiment due to China’s own weak domestic economic and stock market performances. May data implied that the Chinese economy was still facing heavy challenges and real estate sector was still not out of woods yet (ChinaPulse - Government bond issuance is catching up the race to support economy, 19th June 2024). Industrial profits growth dropped to 0.7%yoy in May from April’s 4.0%yoy. The elevated US rates and geopolitical risks also weighed on FDI flows into China. FDI YTD contracted by 28.2%yoy in May, even worse than April’s contraction of 27.9%yoy YTD. Both domestic and overseas sentiments about China were low.

During the past month, USD/CNY fixing has been increasing from 7.1088 to 7.1268 (a 0.25% increase). This triggers market speculation on whether PBOC is considering to let CNY depreciate further. There are two points worthy of mentioning: First, the 0.25% increase in the fixing is still small, and the gaps between the fixing and onshore USD/CNY, and between the onshore and offshore pairs have been large. The government’s intention and actions to stabilize the exchange rate weren’t absent; secondly, compared with the euro against the US dollar and the Japanese yen against the US dollar, the performance of the RMB was actually much stronger recently. Looking forward, with our base case assumption of a weaker US dollar in Q3 and Q4, an expectation of moderate improvement in China economic fundamentals in the near-term suggested by stronger bond issuance and more policy stimulus, we see downside pressure building on USD/CNY. Should offshore RMB exchange rate against the dollar fluctuate much, it is possible that the central bank will strengthen the liquidity adjustment of offshore RMB by increasing the issuance of offshore central bank bills, so to limit offshore RMB’s weakness.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q3 2024 |

Q4 2024 |

Q1 2025 |

Q2 2025 |

|

|

Loan Prime Rate 1Y |

3.45% |

3.35% |

3.25% |

3.25% |

3.25% |

|

MLF 1Y |

2.50% |

2.35% |

2.20% |

2.20% |

2.20% |

|

7-Day Repo Rate |

2.30% |

1.70% |

1.60% |

1.60% |

1.60% |

|

10-Year Yield |

2.21% |

2.30% |

2.40% |

2.45% |

2.55% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

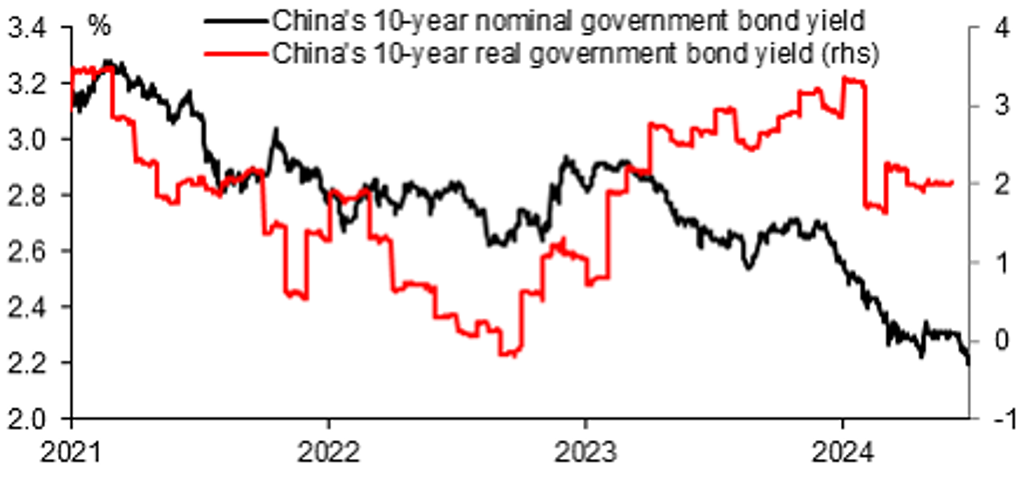

Chinese government bond yields have been declining to a two-decade low of 2.203%. A strong rally in China’s government bonds reflected persistent worries about the outlook for growth. The strong demand for increased government bonds issued was evident this June amid a still struggling economy, and the release of weak May macro key economic indicators in Mid-June and newly released sharp slow down in industrial profits growth for May reinforced market jitters. Also, poor performance of stock markets stressed investor’s confidence as well. The CSI 300 index declined by 3.1% in June, making China the worse performing market in Asia in June. The market still expects a quite muted growth ahead, and more monetary easing measures, including some policy rate cut by PBOC. However, we think that, with policies slowly taking effect, more stimulus to help stabilze the property sector and revitalize sentiment, and the capital raised through the government’s issuance being put to use, it is likely to see a economic recovery in Q3, which will in turn help to stablize yields and even help push up bond yields modestly.

CHINA REAL INTEREST RATE STILL HIGH (10 YEAR GOVERNMENT BOND YIELD – CPI INFLATION)

Source: CEIC, MUFG GMR

STRONG GOVERNMENT BOND ISSUANCE IN MAY 2024 VS LAST YEAR

Source: CEIC, MUFG GMR