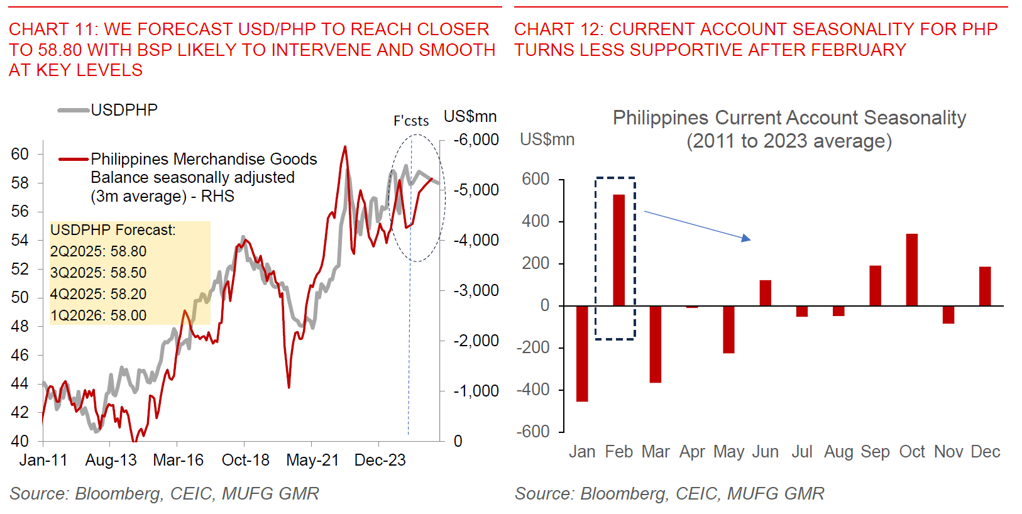

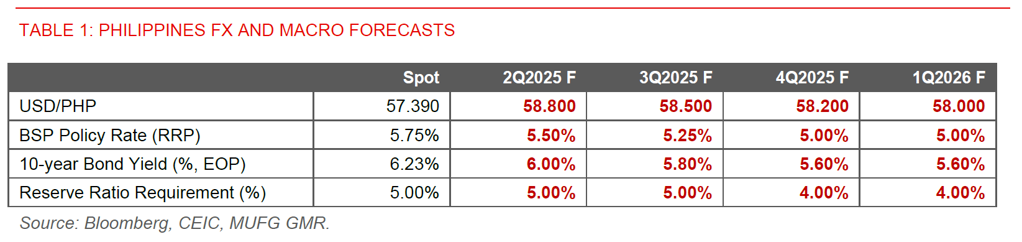

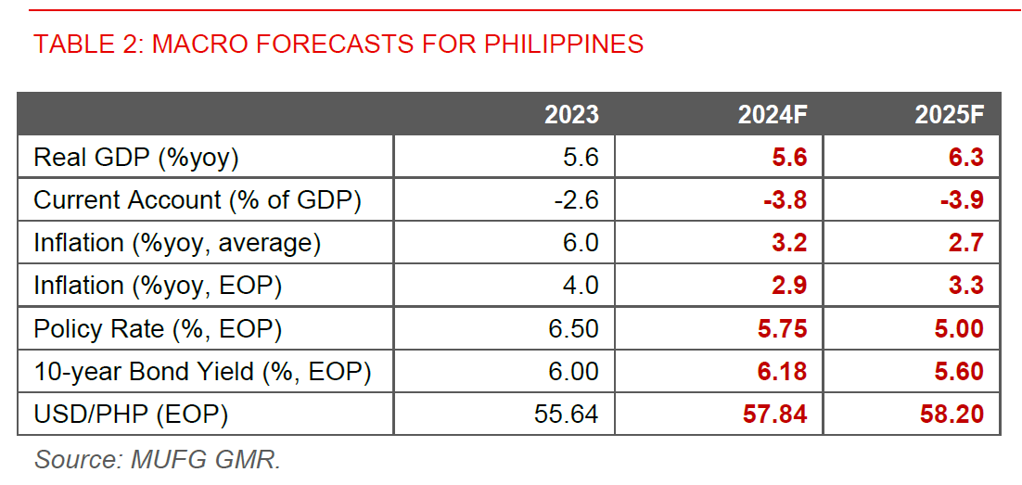

- We maintain our view for USD/PHP to rise to 58.80 in 2Q2025, before moving down to 58.20 in 4Q2025 (see Chart 1 below).

- In many ways, the positive local drivers we have highlighted for PHP previously have not changed. These include the surge in FDI approvals, manageable inflation, improving domestic growth, coupled with far less scrutiny and impact from Trump’s tariffs for the Philippines relative to other Asian economies. The flipside on tariffs is that the Philippines is unlikely to benefit as much from supply chain diversification given the structure of its export basket. We also expect BSP to smooth USD/PHP at key levels including closer to 59.00.

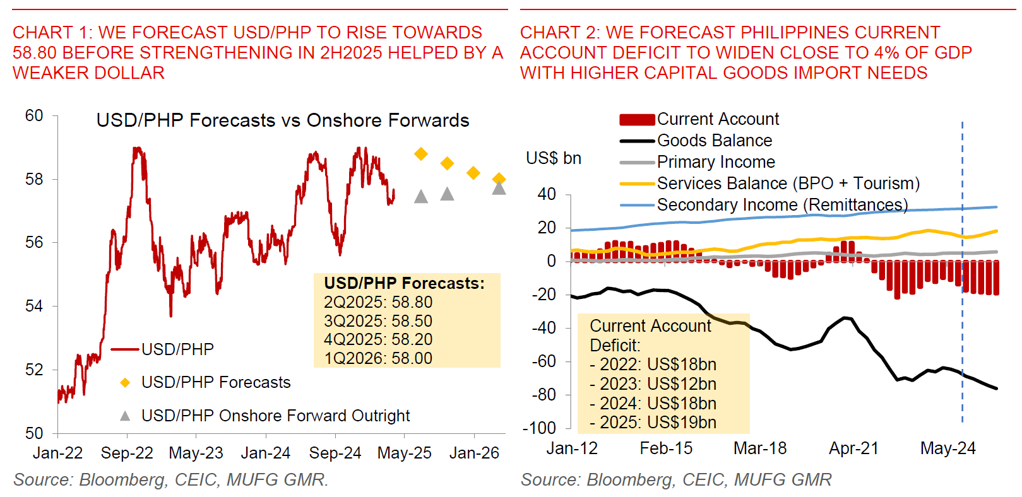

- Nonetheless, what has changed is a larger current account deficit forecast of 3.9% of GDP for the Philippines in 2025 (~US$19bn), driven not just by stronger capital goods imports but also some underperformance in exports. Rising FDI should help to at least partially fund this gap, but a larger current account deficit adds some risks for FX as we move through 2025.

- Balancing these factors, we have kept our USD/PHP FX forecasts unchanged despite the weakness in the Dollar thus far, and also given our expectation for CNY to weaken from 2Q2025.

- We continue to forecast BSP to cut rates by another 75bps to 5.00% by 2025, but see risks that the timing will be delayed if FX volatility picks up sharply. We expect BSP to cut the Reserve Ratio Requirement again by another 100bps this year, bringing it to 4.00%, from 5.00% currently.

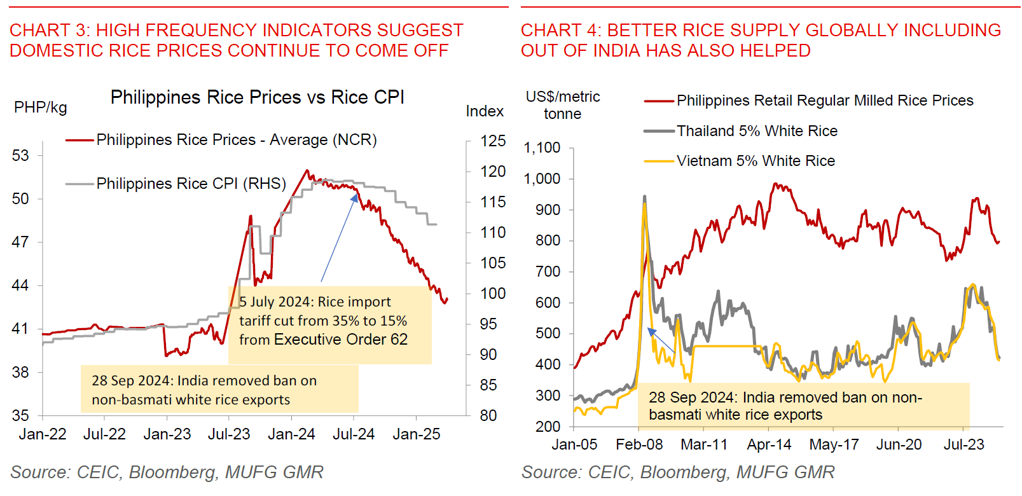

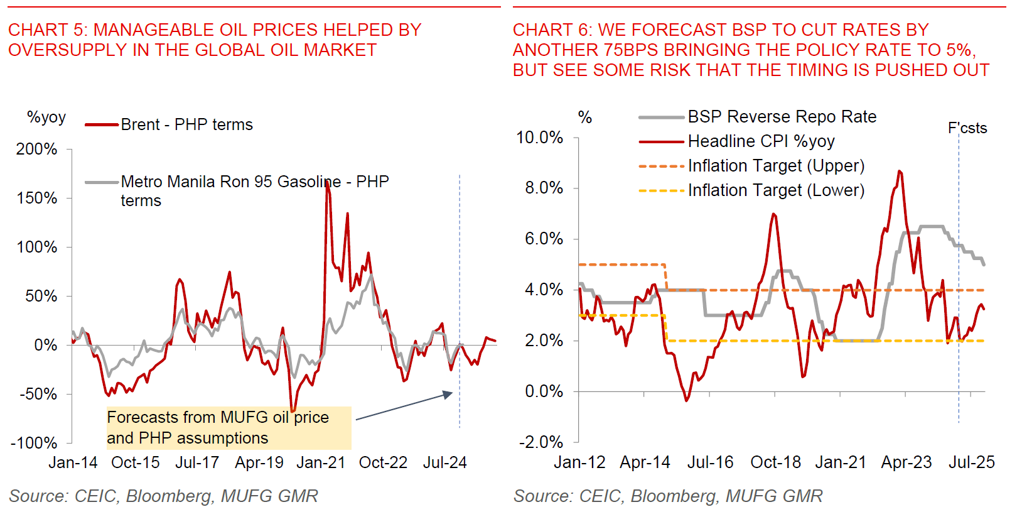

- Inflation manageable with lower domestic rice prices, good global rice supplies, coupled with manageable global oil prices: First, the positives for Philippines macro, including many factors which we been highlighting for a while. We expect inflation in the Philippines to remain manageable at around 3% for 2025, given the continued moderation in domestic rice prices based on the high frequency indicators that we track. This has been helped by the rice import tariff cuts that the Philippines government previously did in July 2024. It is however important to note that it is not just domestic rice prices, but also global rice supplies which have been supportive, with India taking steps to remove export bans on non-basmati white rice. Our commodity analyst expects global oil prices to remain benign this year at below US$80/bbl given oversupply, and this should help cap inflation pressures in the Philippines.

We forecast BSP to cut rates by another 75bps bringing it to 5.00%. We however see some risks that the timing will be delayed if FX volatility picks up through 2025. We think the Philippines central bank is likely to cut rates come the April meeting, and have pencilled in 2 more cuts likely in the August and December meetings. There is however a risk that the exact timing may be pushed out depending on FX volatility, and also given our view that the risk-reward for USD/PHP is tilted higher from current levels. We also see a good chance that the BSP will cut the reserve ratio requirement once more by another 100bps by the end of 2025, bringing it to 4.00% from 5.00% currently. We also expect the BSP to intervene to smooth FX volatility at key USD/PHP levels including around 59.00 and if that breaks certainly the 60.00 levels

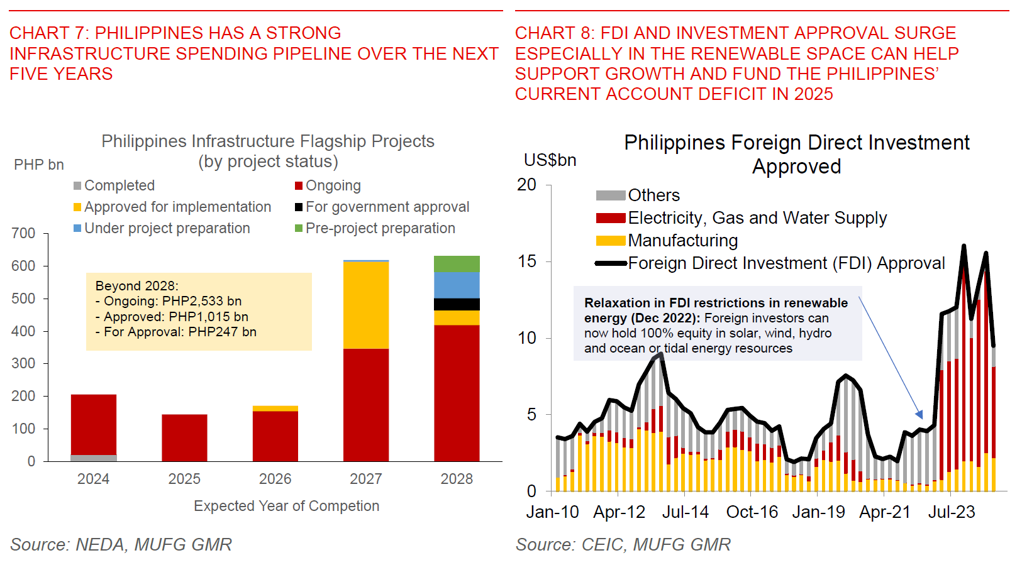

- Growth should pick up to >6% in 2025, helped by manageable inflation, the lagged impact of rate cuts, strong infrastructure pipeline, coupled with some impact from mid-term Congressional Elections. Besides manageable inflation and lower rates, other key positives for the Philippines growth and PHP which we have been highlighting include a strong infrastructure spending pipeline of close to 15% of GDP over the next 5 years. In addition, the mid-term Congressional elections should also help boost consumption especially in 1H2025. In addition, the surge in FDI approvals from around US$4bn in 2022 to close to US$16bn in 2024 helped by increasing project pipelines in the renewable space should not only help support investment activity through 2025, but importantly from an FX perspective, help to fund the current account deficit

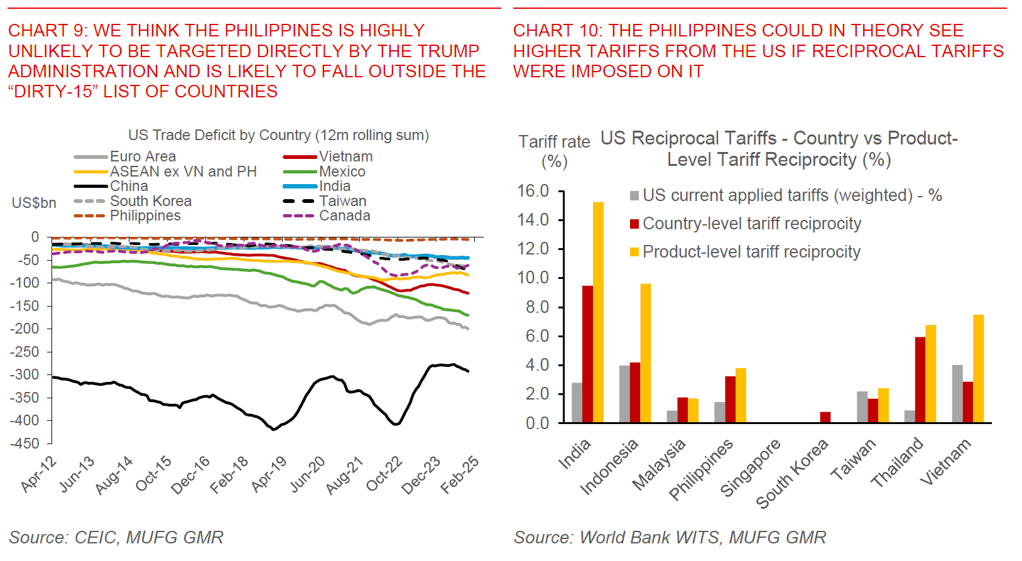

- On the global front, we continue to think that the Philippines is much less exposed to Trump’s tariffs, certainly relative to the likes of China, India and Vietnam. Nonetheless, the flipside is that the Philippines is unlikely to benefit from continued supply chain diversification due to higher tariffs on China, given the structure of its export basket. Our base case is that the Philippines will not be targeted directly by the Trump 2.0 administration including in upcoming reciprocal tariffs, in part because its trade deficit with the United States is very small certainly relative to other countries such as China, India and Vietnam. Nonetheless, the flipside is that the Philippines being more domestically-oriented and also having a more narrow goods export basket focusing on semiconductor testing and assembly will unlikely benefit from supply chain shifts due to these tariffs. Overall, we still think it is right to say that the Philippines is more insulated from Trump 2.0’s tariffs.

- What however weighs on PHP from an FX perspective is a larger current account deficit of around 4% of GDP or US$19bn in 2025. This widening in the current account deficit is driven both by our expectation for capital goods imports to pick up, coupled with some weakness in goods exports leading to a wider goods deficit. We think the surge in FDI approvals especially in the renewables space can help to partially fund this deficit but the size of the deficit is quite large and so we think there could be bouts of PHP FX volatility through 2025 especially if global risk sentiment turns sour.