Key Points

Several ASEAN FX has come under renewed pressure against the dollar following the 18 June FOMC meeting, most notably MYR (-1.8%) and THB (-1.7%), as a more hawkish Fed policy stance and reduced forward guidance reinforce a high US yield environment, sustaining USD strength through carry-driven demand. With Fed Chair Kevin Warsh stepping back from the dot plot, policy uncertainty has increased, which could lift term premia and keep US yields elevated in the near term.

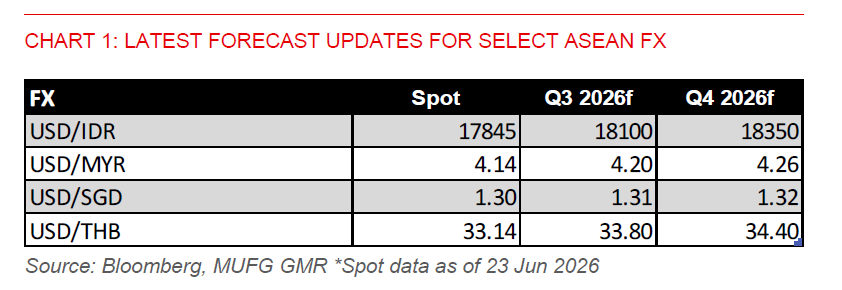

For the ringgit, our previous constructive view—anchored on narrowing rate differentials with the US and resilient manufacturing and electronics exports—remains intact over the medium term. The recent weakness instead reflects a shift toward US rate dynamics rather than any deterioration in domestic fundamentals. Against this backdrop, contained inflation and sustained fuel subsidies reduce the urgency for Bank Negara Malaysia to tighten policy, leaving MYR increasingly exposed as US-Malaysia rate differentials widen. This underpins a near-term bearish bias on the ringgit, although we expect macro fundamentals to reassert themselves once US rate pressures ease.

For the Thai baht, recent weakness despite lower oil prices highlights a decoupling from easing terms-of-trade pressures. Instead, the baht is now being weighed down by its low-yield profile and the Bank of Thailand’s growth-focused policy stance, which limits the scope for monetary policy tightening. Rising US yields have triggered a shift toward net foreign portfolio outflows from Thailand ($379mn net foreign outflows in June vs. $680mn net inflows in May), despite easing pressures from lower oil prices, reinforcing depreciation pressures and explaining the baht’s underperformance.

The rupiah has been supported by Bank Indonesia’s recent proactive policy tightening and FX support measures, but elevated US yields and domestic policy uncertainty around the government’s commodity export control plan are testing this buffer. In addition, MSCI has deferred its decision on Indonesian’s equity market classification till November. We expect further BI tightening to 6.25% by year-end to provide stronger cushion for the rupiah, helping to slow the pace of rupiah depreciation against the dollar.

SGD remains comparatively defensive under the MAS S$NEER framework, which dampens FX volatility and inflation expectations, but it is still likely to weaken modestly against the USD due to widening rates differentials in favour of the dollar.

Overall strategy remains USD-positive against selective ASEAN FX in the near term, particularly THB, MYR, and IDR, while favouring SGD on a relative basis given MAS tight S$NEER policy stance. We expect MAS to keep its tight policy stance unchanged at the July meeting, as resilient growth will likely allow the central bank to lean against inflation risks.