Please download PDF from the button above for all other contents for the following currencies.

Australian dollar // New Zealand dollar //Canadian dollar // Norwegian krone // Swedish Krona // Swiss franc // Czech koruna // Hungarian forint //Polish zloty // Romanian leu // Russian rouble // South African rand // Turkish lira // Indian rupee // Indonesian rupiah // Malaysian ringgit // Philippine peso //Singapore dollar // South Korean won // Taiwan dollar // Thai baht // Vietnamese dong // Argentine peso // Brazilian real // Chilean peso // Mexican peso // Crude oil // Saudi riyal // Egyptian pound

Monthly Foreign Exchange Outlook

DEREK HALPENNY

Head of Research, Global Markets EMEA and International Securities

Global Markets Research

Global Markets Division for EMEA

E: derek.halpenny@uk.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

E: lee.hardman@uk.mufg.jp

LIN LI

Head of Global Markets Research Asia

Global Markets Research

Global Markets Division for Asia

E: lin_li@hk.mufg.jp

JEFF NG

Senior Currency Analyst

Global Markets Research

Global Markets Division for Asia

E: Jeff_ng@sg.mufg.jp

EHSAN KHOMAN

Head of Commodities, ESG and Emerging Markets Research – EMEA

DIFC Branch – Dubai

E: ehsan.khoman@ae.mufg.jp

CARLOS PEDROSO

Chief Economist

Banco MUFG Brasil S.A.

E: cpedroso@br.mufg.jp

MAURICIO NAKAHODO

Senior Economist

Banco MUFG Brasil S.A.

E: mnakahodo@br.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

April 2023

KEY EVENTS IN THE MONTH AHEAD

1) BOJ TO TAKE THE LIMELIGHT IN APRIL

After advancing by 2.7% in February, the US dollar (DXY) renewed the decline that had taken place over the previous four months and fell by 2.3% in March. The banking sector turmoil has fuelled rate cut expectations by the Fed by year-end which was a key catalyst for US dollar weakness. The Fed’s liquidity support for banks could help stem the crisis but there will still likely be an impact on credit flows to the real economy. We have lowered further our USD forecasts over the forecast profile. With the G3 central banks not meeting in April, attention will be much more on the BoJ in April, especially given the meeting on 27th-28th April will be the first for incoming Governor, Kazuo Ueda who takes over from Haruhiko Kuroda on 9th April. We view this as a significant changing of the guard and expect the YCC policy framework engineered by Kuroda to be removed relatively quickly. There have been warnings from the new BoJ leadership over the inevitability of surprises in policy announcements when moving away from a framework like YCC and hence readers should view every BoJ policy meeting as ‘live’ with the potential for a scrapping of YCC. We have maintained our view of an end to YCC in Q2, either at the April or June meetings. We are sceptical of the rebound in USD/JPY in March proving sustainable going forward.

2 ) ANOTHER G10 CENTRAL BANK TO PAUSE

The Bank of Canada was the first G10 central bank to pause its tightening cycle in March and will likely be joined by the RBA in April with the guidance from the RBA clearly suggesting a pause at its meeting on 4th April. The RBNZ meets the following day and while a 25bp rate hike is expected, we suspect it will be accompanied by guidance that suggests more strongly the scope for a pause at the following meeting on 24th May. The Fed, ECB and BoE are now priced for 25bp rate hikes at probabilities of 60%; 90%; and 75% respectively for their meetings in May. Data on inflation, the jobs market and wages will remain key in April for future monetary policy deliberations and in that context, the NFP data on 7th April and the US CPI data on 12th April will be crucial in shaping expectations for the FOMC meeting on the 3rd May.

3 ) UPCOMING MARCH ACTIVITY DATA FROM CHINA

China’s official composite PMI continued to improve in March, suggesting a better set of March data for major macro indicators to be released in mid-April. Against the banking sector risks in DM markets, a relatively better situation in China likely further attracts capital inflows, and CNY will be supported by it subsequently in April. March exports could bring some stress on the currency, as implied by the weaker manufacturing PMI in March.

Forecast rates against the US dollar - End-Q2 2023 to End-Q1 2024

|

Spot close 31.03.23 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

JPY |

132.90 |

129.00 |

127.00 |

125.00 |

123.00 |

|

EUR |

1.0863 |

1.1000 |

1.1200 |

1.1400 |

1.1200 |

|

GBP |

1.2370 |

1.2640 |

1.2870 |

1.3030 |

1.2730 |

|

CNY |

6.8675 |

6.7500 |

6.6500 |

6.5500 |

6.4500 |

|

AUD |

0.6704 |

0.6800 |

0.7000 |

0.7200 |

0.7100 |

|

NZD |

0.6266 |

0.6300 |

0.6400 |

0.6600 |

0.6500 |

|

CAD |

1.3529 |

1.3600 |

1.3500 |

1.3200 |

1.3200 |

|

NOK |

10.457 |

10.091 |

9.7320 |

9.3860 |

9.5540 |

|

SEK |

10.355 |

10.182 |

9.911 |

9.561 |

9.6430 |

|

CHF |

0.9127 |

0.9090 |

0.9020 |

0.8950 |

0.8930 |

|

|

|

|

|

|

|

|

CZK |

21.589 |

21.270 |

20.710 |

20.260 |

20.540 |

|

HUF |

349.21 |

345.50 |

348.20 |

346.50 |

361.60 |

|

PLN |

4.3057 |

4.2730 |

4.1520 |

4.1230 |

4.2410 |

|

RON |

4.5514 |

4.5090 |

4.4460 |

4.3860 |

4.4820 |

|

RUB |

77.432 |

77.510 |

77.800 |

78.080 |

80.650 |

|

ZAR |

17.713 |

18.000 |

17.900 |

17.600 |

17.800 |

|

TRY |

19.185 |

20.250 |

21.750 |

23.000 |

23.500 |

|

|

|

|

|

|

|

|

INR |

82.173 |

81.500 |

80.500 |

79.500 |

79.000 |

|

IDR |

14990 |

15000 |

14800 |

14600 |

14400 |

|

MYR |

4.4130 |

4.4000 |

4.3000 |

4.2000 |

4.1000 |

|

PHP |

54.354 |

55.000 |

54.000 |

53.500 |

53.000 |

|

SGD |

1.3297 |

1.3400 |

1.3200 |

1.3000 |

1.2900 |

|

KRW |

1301.4 |

1270.0 |

1250.0 |

1230.0 |

1210.0 |

|

TWD |

30.479 |

30.200 |

29.900 |

29.600 |

29.300 |

|

THB |

34.065 |

34.250 |

33.250 |

32.250 |

31.250 |

|

VND |

23473 |

23500 |

23400 |

23300 |

23200 |

|

|

|

|

|

|

|

|

ARS |

208.98 |

240.00 |

265.00 |

315.00 |

370.00 |

|

BRL |

5.0631 |

5.2800 |

5.3400 |

5.4000 |

5.4200 |

|

CLP |

792.00 |

820.00 |

830.00 |

840.00 |

850.00 |

|

MXN |

18.047 |

18.600 |

18.800 |

19.000 |

19.000 |

|

|

|||||

|

Brent |

79.40 |

85.00 |

93.00 |

91.00 |

92.00 |

|

NYMEX |

74.61 |

81.00 |

88.00 |

86.00 |

87.00 |

|

SAR |

3.7527 |

3.7500 |

3.7500 |

3.7500 |

3.7500 |

|

EGP |

30.762 |

32.200 |

33.800 |

34.500 |

34.900 |

Notes: All FX rates are expressed as units of currency per US dollar bar EUR, GBP, AUD and NZD which are expressed as dollars per unit of currency. Data source spot close; Bloomberg closing rate as of 4:30pm London time, except VND which is local onshore closing rate.

US dollar

|

Spot close 31.03.23 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

USD/JPY |

132.90 |

129.00 |

127.00 |

125.00 |

123.00 |

|

EUR/USD |

1.0863 |

1.1000 |

1.1200 |

1.1400 |

1.1200 |

|

Range |

Range |

Range |

Range |

||

|

USD/JPY |

124.00-140.00 |

122.00-138.00 |

120.00-136.00 |

118.00-134.00 |

|

|

EUR/USD |

1.0300-1.1300 |

1.0500-1.1500 |

1.0600-1.1600 |

1.0700-1.1800 |

MARKET UPDATE

In March the US dollar weakened against the euro in terms of London closing rates, moving from 1.0612 to 1.0863. In addition, the dollar weakened versus the yen, from 136.15 to 132.90. The FOMC, at its meeting in March hiked the fed funds rate by 25bps to 4.75%-5.00%, following 450bps since March of last year. The FOMC has also continued with its policy of reducing its securities holdings with QT ongoing at a pace of USD 95bn worth of UST bonds (USD 60bn) and MBS (USD 35bn) of balance sheet reduction each month. However, this was dramatically offset by balance sheet expansion to provide loans and liquidity for the banking sector

OUTLOOK

After advancing by 2.7% in February, the US dollar (DXY) depreciated in March by 2.3% fuelled a huge shift in rate hike expectations triggered by the collapse of two regional banks in the US. When Fed Chair Powell presented his semi-annual testimony to Congress, the message was more tightening would be needed, which prompted the markets to price in a total of 100bps of more tightening this year. After the bank failures and the delivery of a 25bp rate hike, the markets now expect nearly 50bps of easing by year-end. This pricing suggests to us that markets are positioned for another bout of market turmoil. Some of that easing may come out of the market over the short-term although it does seem quite likely that we will see further market volatility of some kind before the end of the year. The Fed’s action in creating a liquidity window to accept US Treasury securities, Agency securities and MBS at par value in exchange for cash has cut off the risk of deposit flight based on these securities being held at a loss after the huge sell-off over the last year.

But even with no renewed turmoil, we believe there is a good chance the FOMC will now pause. The updated dots profile implies one further 25bp rate hike which is still a clear risk. If the jobs and inflation data remain firm and we see no additional turmoil, the FOMC could hike. But there is less justification now for further action. Financial conditions have tightened – the St. Louis Fed Financial Stress Index jumped to its highest level since the GFC when the covid period is excluded. Lending by banks could now slow as banks ensure they reduce the risk of deposit flight. Inflation is also set to slow with services (rents in particular) looking likely to slow over the coming months to add to slowing goods inflation. Wages have also slowed with signs of a pick-up in the supply of labour. The labour force increased by 1.7mn in the three months to February, which will help curtail wage growth going forward.

The developments in March reinforce our view of a weaker US dollar going forward. Our profile is relatively conservative to reflect the likely bouts of risk-aversion that lie ahead that will see increased volatility and corrections stronger for the dollar, in particular versus the higher-beta G10 and EM currencies. The potential for greater caution over extending credit will likely add to disinflationary pressures and reinforce the likely move lower in inflation from here

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

Policy Rate |

4.83% |

4.88% |

4.38% |

3.63% |

3.13% |

|

3-Month T-Bill |

4.69% |

4.50% |

4.25% |

3.63% |

3.13% |

|

10-Year Yield |

3.47% |

3.50% |

3.25% |

3.50% |

3.38% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

We have taken back our extra hike that we put in last month. We are entering the period where the data (a quick CPI slide in Q2/Q3 plus job losses will likely start to stack up) will give the Fed cover to pause. Either way we are relatively indifferent if the Fed hikes one more time or not. In our view the cycle is coming to an end. The credit tightening along with ongoing QT will feel like a few hikes over the course of 2023. That said, as we saw in March, if it’s a close call, but markets have a hike priced in, the Fed will likely deliver on it in May. Yet the risk that other rate sensitive sectors (CRE, PE/private credit etc) start to see cracks in Q2 is also high. We have moved our first cut to September (with the first cut at 50bps not just a 25bp adjustment) and then see scope for more cuts into year-end. Overall, we view what happened in March as having a lasting effect on general credit conditions. Where the rates shock turned into a potential credit crunch as banks become risk averse (along with slower economic activity turned recession) will likely hit cashflows and loan holdings (and eventually lead to defaults). (George Goncalves, US Macro Strategy)

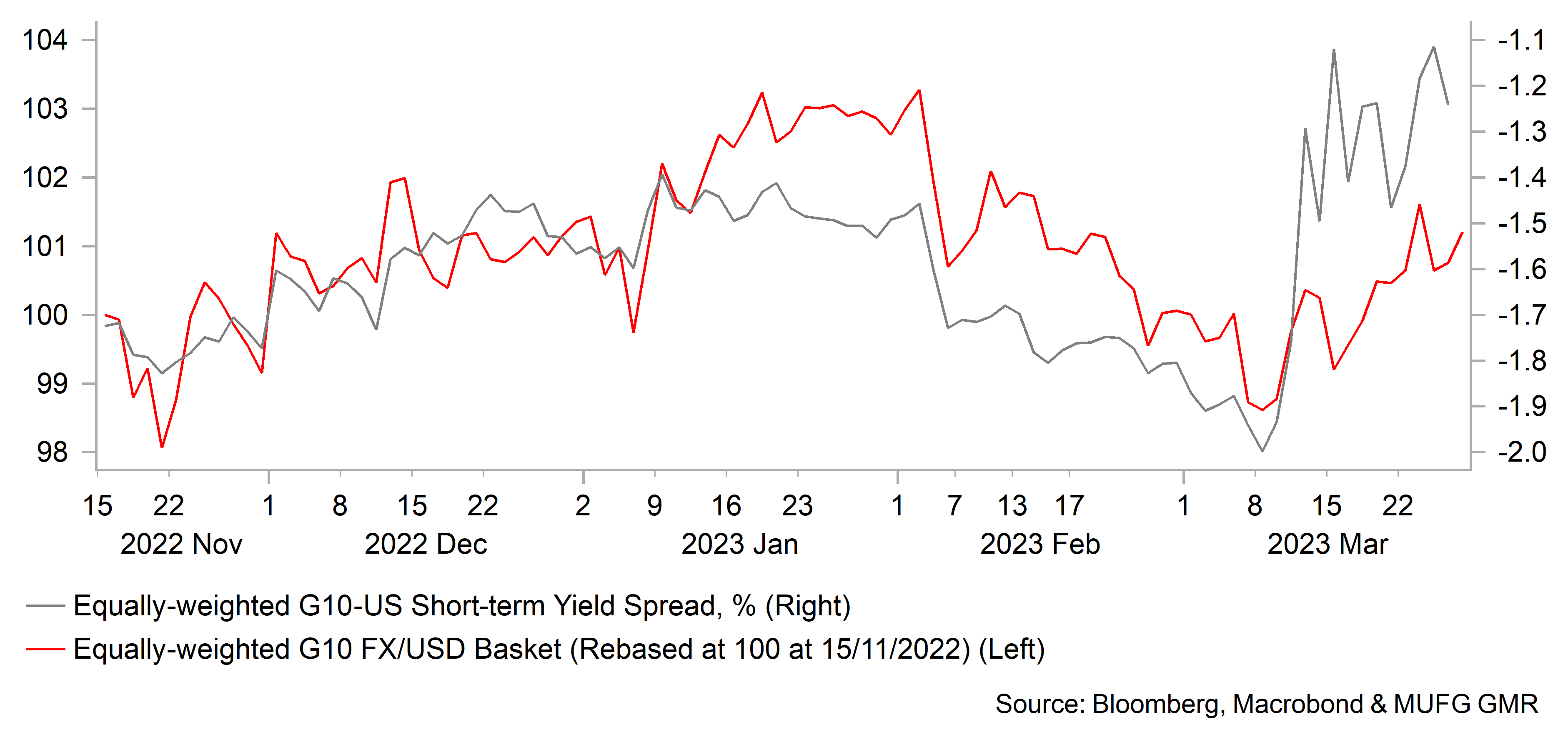

Sharp dovish Fed rate hike repricing weighs on USD

DXY VS. SHORT-TERM YIELD SPREADS

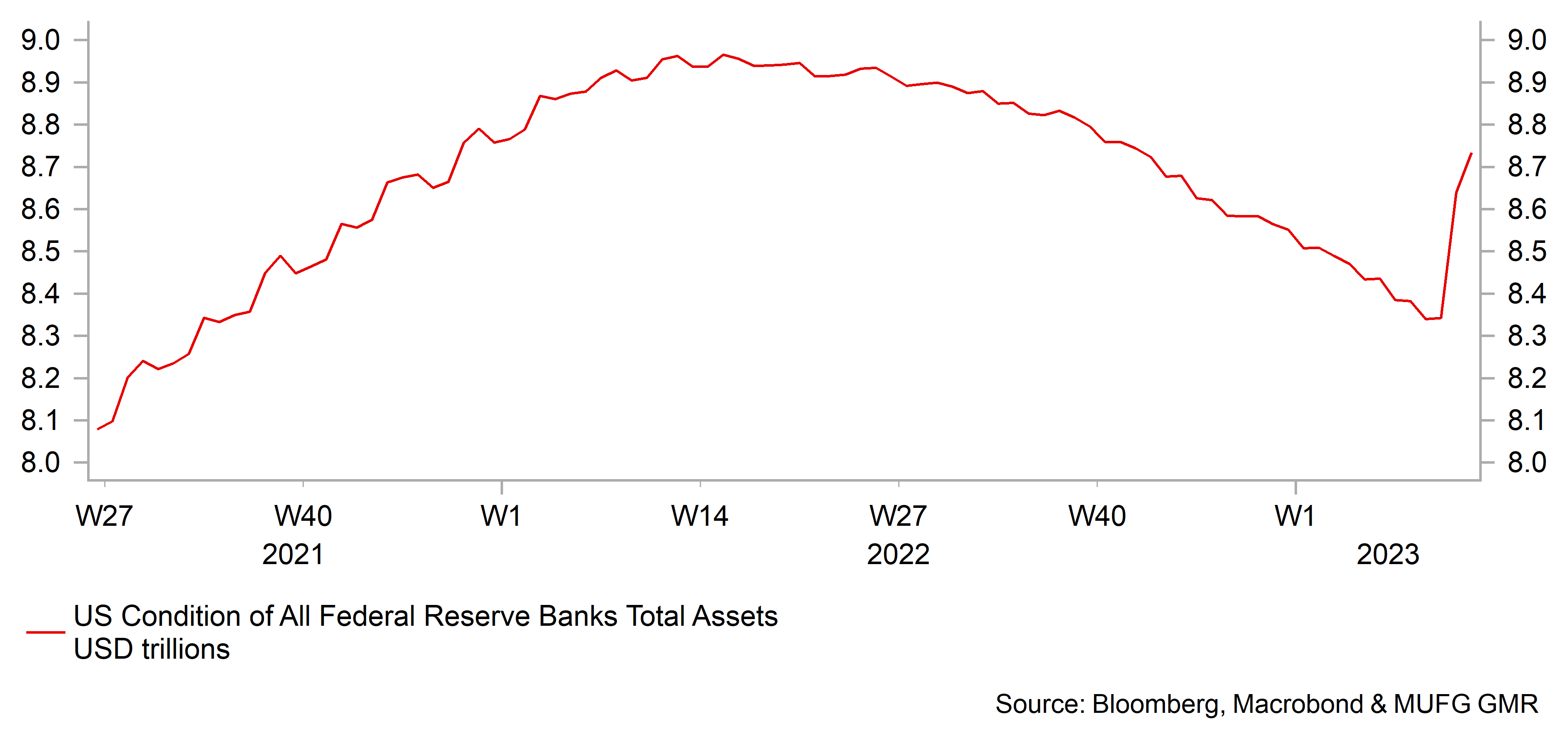

Liquidity support for banks results in expansion of Fed’s balance sheet

SIZE OF FED’S BALANCE SHEET

Japanese yen

|

Spot close 31.03.23 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

USD/JPY |

132.90 |

129.00 |

127.00 |

125.00 |

123.00 |

|

EUR/JPY |

144.37 |

141.90 |

142.20 |

142.50 |

137.80 |

|

Range |

Range |

Range |

Range |

||

|

USD/JPY |

124.00-140.00 |

122.00-138.00 |

120.00-136.00 |

118.00-134.00 |

|

|

EUR/JPY |

137.00-149.00 |

136.00-149.50 |

135.00-150.00 |

134.00-150.00 |

MARKET UPDATE

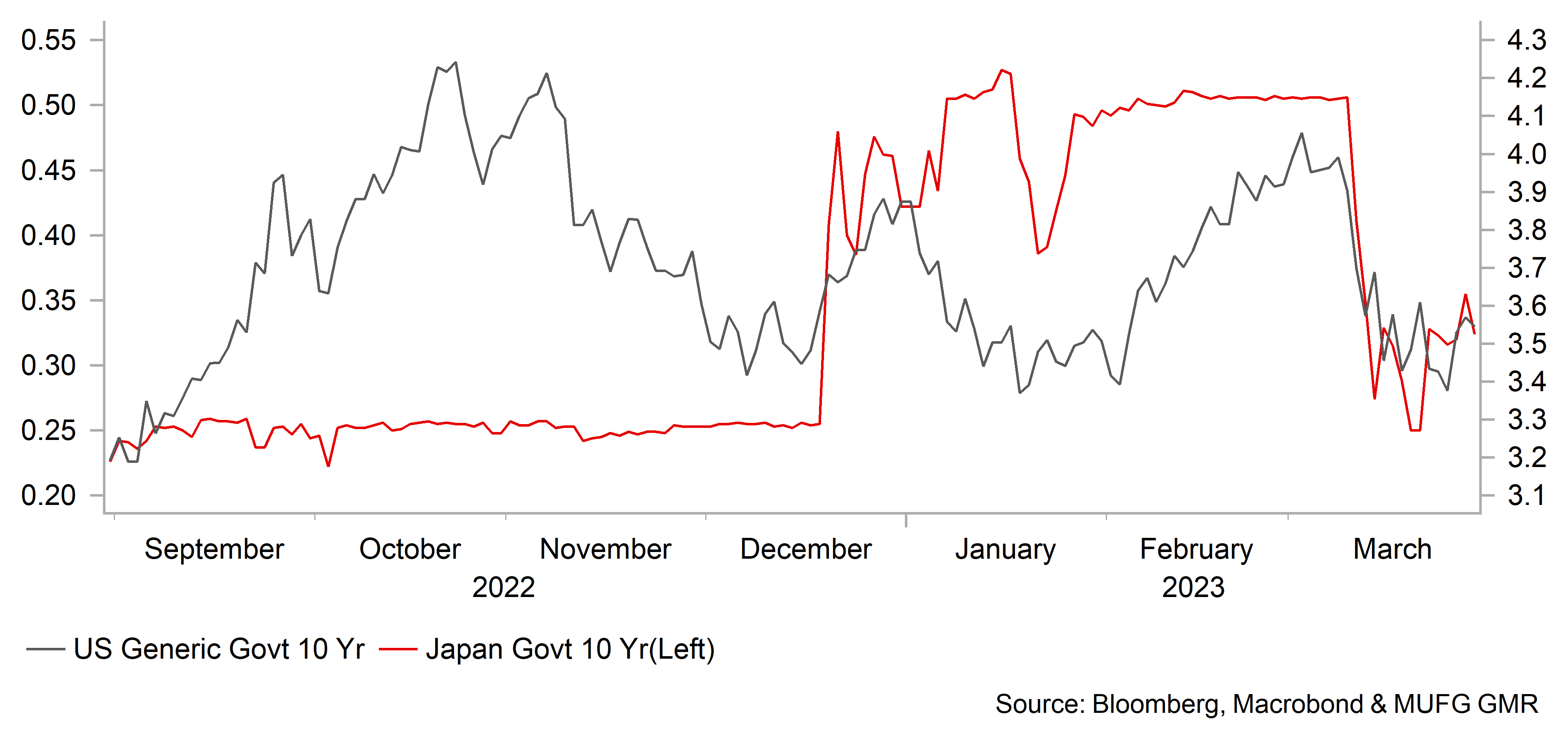

In March the yen strengthened substantially versus the US dollar in terms of London closing rates from 136.15 to 132.90. The yen strengthened only very marginally versus the euro, from 144.48 to 144.37. The BoJ at its meeting in March, Governor Kuroda’s last, announced an unchanged policy stance with the key policy rate at -0.10% and YCC maintained, restraining the 10-year yield within a range of +/-50bps around zero percent. The 10-year JGB yield retreated from the 0.50% upper limit following the banking sector turmoil and the drop in global yields

OUTLOOK

The yen surged in value in March primarily fuelled by the onset of financial market turmoil due to the collapse of US regional banks and the near-collapse of Credit Suisse. There was a remarkably sudden shift from 8th March onwards when the news began to break of trouble at Silicon Valley Bank. On that day, USD/JPY peaked at just below 138.00 and then fell to levels below 130.00 before stabilising. The move in USD/JPY coincided with Fed policy rate expectations swinging from a market pricing of +100bps of tightening by year-end to -90bps of monetary easing by 24th March. Both are extremes and whether the Fed hikes again and/or cuts this year will partially be dependent on whether further bank failures emerge in the coming weeks. But even with no further problems there is now a greater probability of recession in the US and hence a greater probability that the Fed has reached its terminal policy rate. This development only reinforces our forecast profile of further declines in USD/JPY as the entire 2022 move higher is retraced.

A change of leadership at the BoJ will officially take place in April with incoming Governor Ueda commencing on 9th April. The turmoil in the markets has eased the upward pressure on the 0.50% ceiling for the 10-year JGB yield but the fundamental backdrop in Japan still points to the likely removal of the YCC policy framework. Increased subsidy support from the government helped bring overall nationwide YoY CPI lower, from 4.3% to 3.3% in February. However, the core-core measure accelerated from 3.2% to 3.5%, the highest level since January 1982. Japan’s trade union confederation, Rengo, confirmed the annual shunto wage negotiations reached an agreement to raise base pay before bonuses of 2.3%, up from just 0.5% a year ago. When smaller companies are included the national wage increase will be lower but the increases are clearly significant and will likely lead to the BoJ inflation forecasts to the published in April being raised.

The turmoil in financial markets due to banking sector uncertainties could mean the BoJ waits longer before removing YCC. We had estimated June as a possible time for scrapping YCC. If it is later, we still expect its removal this year given the prospects of higher levels of inflation. The yen is set to continue strengthening going forward and there are risks of more abrupt moves stronger if there are further episodes of banking sector problems that fuels renewed risk aversion

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

Policy Rate |

-0.10% |

-0.10% |

-0.10% |

-0.10% |

-0.10% |

|

3-Month Bill |

-0.25% |

-0.15% |

-0.05% |

0.05% |

0.05% |

|

10-Year Yield |

0.35% |

0.70% |

0.60% |

0.50% |

0.40% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The dramatic plunge in global yields in response to the problems that emerged in the US regional banking sector and the near failure of Credit Suisse has seen the 10-year JGB yield decline as well. In March, the 10-year yield fell 16bps to close at 0.35%. It was the largest one-month decline in the 10-year yield since YCC was introduced in 2016. The reason for such a decline based on domestic factors was certainly not as compelling with the core-core YoY CPI rate accelerating to 3.5% in February, the highest level since 1982. But declining inflation globally will also be reflected in Japan and the substantial upward pressure on JGB yields should not be as prevalent going forward. That might be the perfect time for the BoJ to remove YCC without creating too much volatility. Based on what has happened globally and based on the probability that policy rates have peaked or are close to peaking, we would expect a jump in JGB yields to be brief following an end to YCC before retracing back lower as inflation pressures ease. The risk to this view may now be more skewed toward the BoJ delaying a removal of YCC for longer

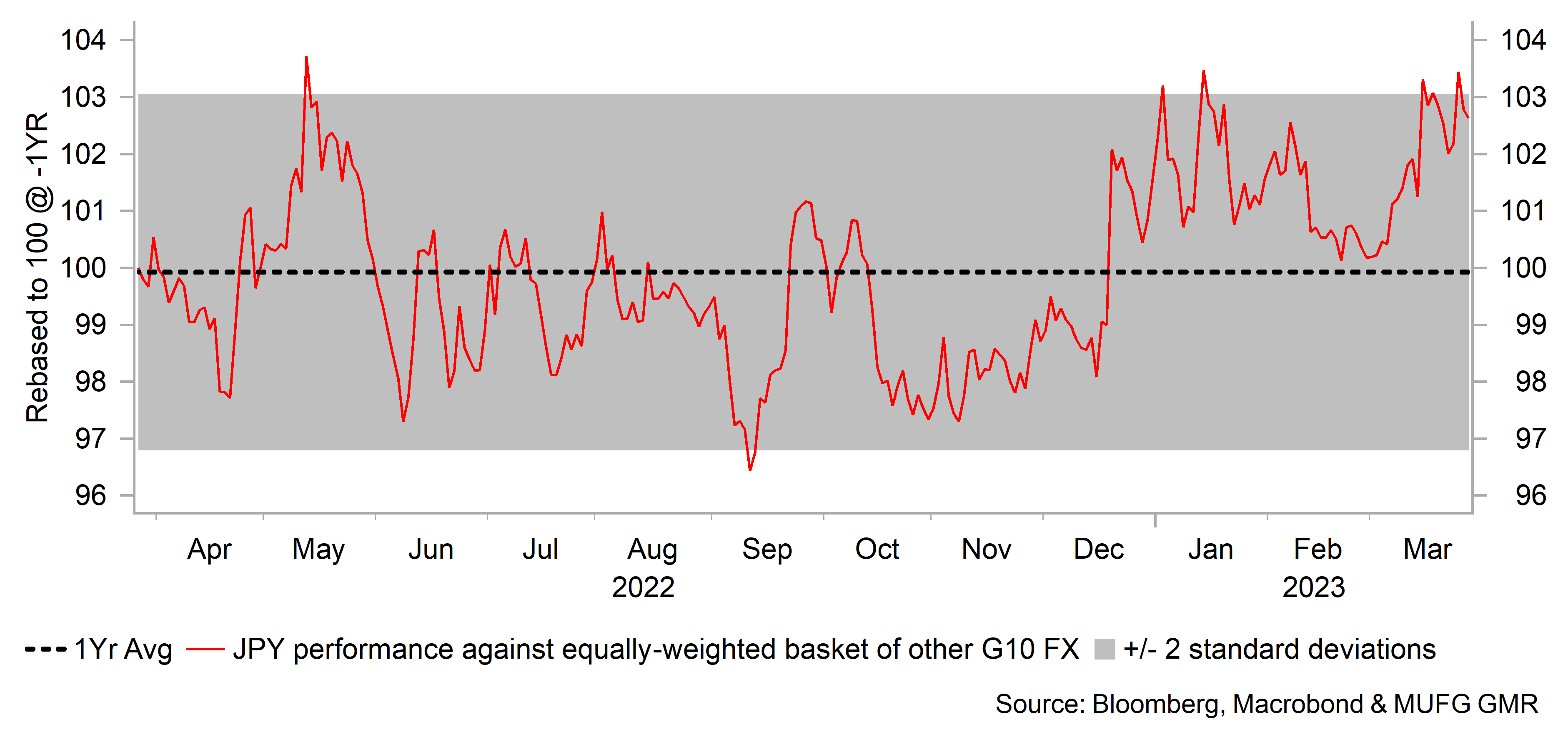

Rising yields outside of Japan have weighed down on JPY again

PERFORMANCE OF JPY VS. OTHER G10 FX

Banking fears trigger demand for the JPY

UST BOND VS JGB 10-YEAR YIELDS

Euro

|

Spot close 31.03.23 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

EUR/USD |

1.0863 |

1.1000 |

1.1200 |

1.1400 |

1.1200 |

|

EUR/JPY |

144.37 |

141.90 |

142.20 |

142.50 |

137.80 |

|

Range |

Range |

Range |

Range |

||

|

EUR/USD |

1.0300-1.1300 |

1.0500-1.1500 |

1.0600-1.1600 |

1.0700-1.1800 |

|

|

EUR/JPY |

137.00-149.00 |

136.00-149.50 |

135.00-150.00 |

134.00-150.00 |

MARKET UPDATE

In March the euro strengthened versus the US dollar in terms of London closing rates, moving from 1.0612 to 1.0863. The ECB at its meeting in March raised the key policy rate by 50bps to 3.00% following 300bps of tightening since last year. That was the most aggressive tightening in a year by the ECB and will be augmented by QT going forward. The ECB commenced QT in March with a EUR 15bn per month reduction in APP planned through to June

OUTLOOK

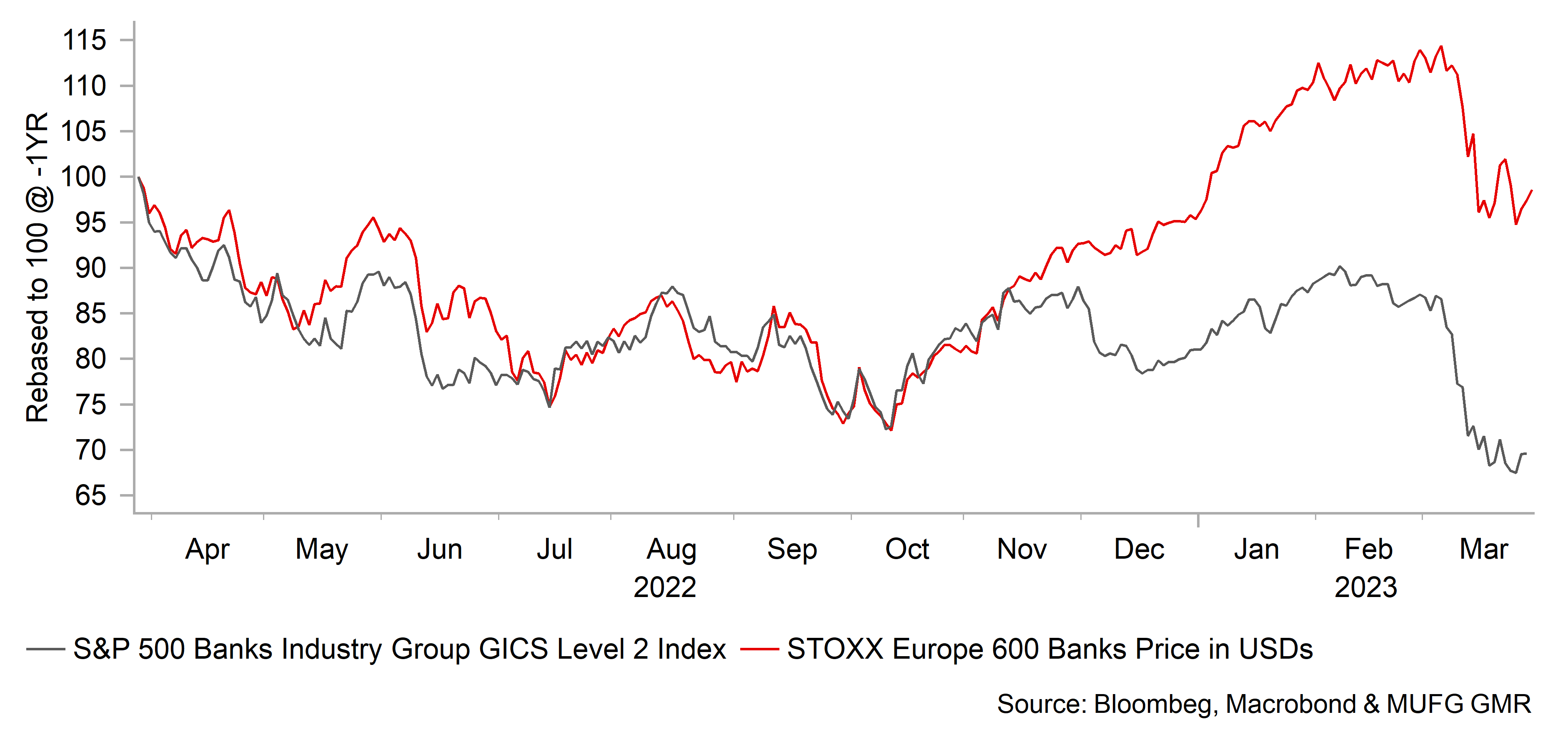

The euro advanced notably in March with the near-collapse of Credit Suisse having limited impact on broader sentiment in Europe. Indeed, while the Euro Stoxx 600 Bank Index closed 14.1% down in March, on a year-to-date basis ended March 3.9% higher. In contrast, the S&P 500 Bank Index is 19.8% lower in March, and 13.8% lower ytd. The near collapse of Credit Suisse was dealt with promptly with the SNB providing strong support for UBS to manage the integration of Credit Suisse through a EUR 100bn liquidity window and a EUR 9bn loss guarantee (after an initial EUR 5bn loss for UBS). Investors ultimately liked the deal and there was an overall recovery in sentiment. However, risks could turn higher again. The euro-zone has 2,400 small/medium-sized banks under national supervision but investors view euro-zone supervision and regulation as more vigorous and hence currently risks are deemed smaller in the euro-zone relative to the US. By contrast, the US has 4,277 small/medium-sized regional banks (FDIC data). The ECB did emphasise in March that it stood ready to take action to ensure ample liquidity if this became needed.

That commitment from the ECB came at the monetary policy meeting when the ECB went ahead with its well-telegraphed plan to hike by 50bps, taking the deposit rate to 3.00%. The guidance did change however and now the ECB believe that “the elevated level of uncertainty reinforces the importance of a data-dependent approach to the Governing Council’s policy rate decisions” in contrast to the explicit guidance of a 50bp rate hike at the February meeting. ECB rhetoric has continued the indicate the probability of more rate hikes to come – ECB President Lagarde stated after the banking turmoil that there would be no trade-off between fighting inflation and supporting banks. That promise however can only go so far in our view and there are likely macro implications from this in terms of reduced credit into the real economy that will in turn reduce inflation risks. Nonetheless, assuming there are no additional episodes of crisis with banks, the ECB will likely raise rates once or maybe twice further by 25bps on each occasion.

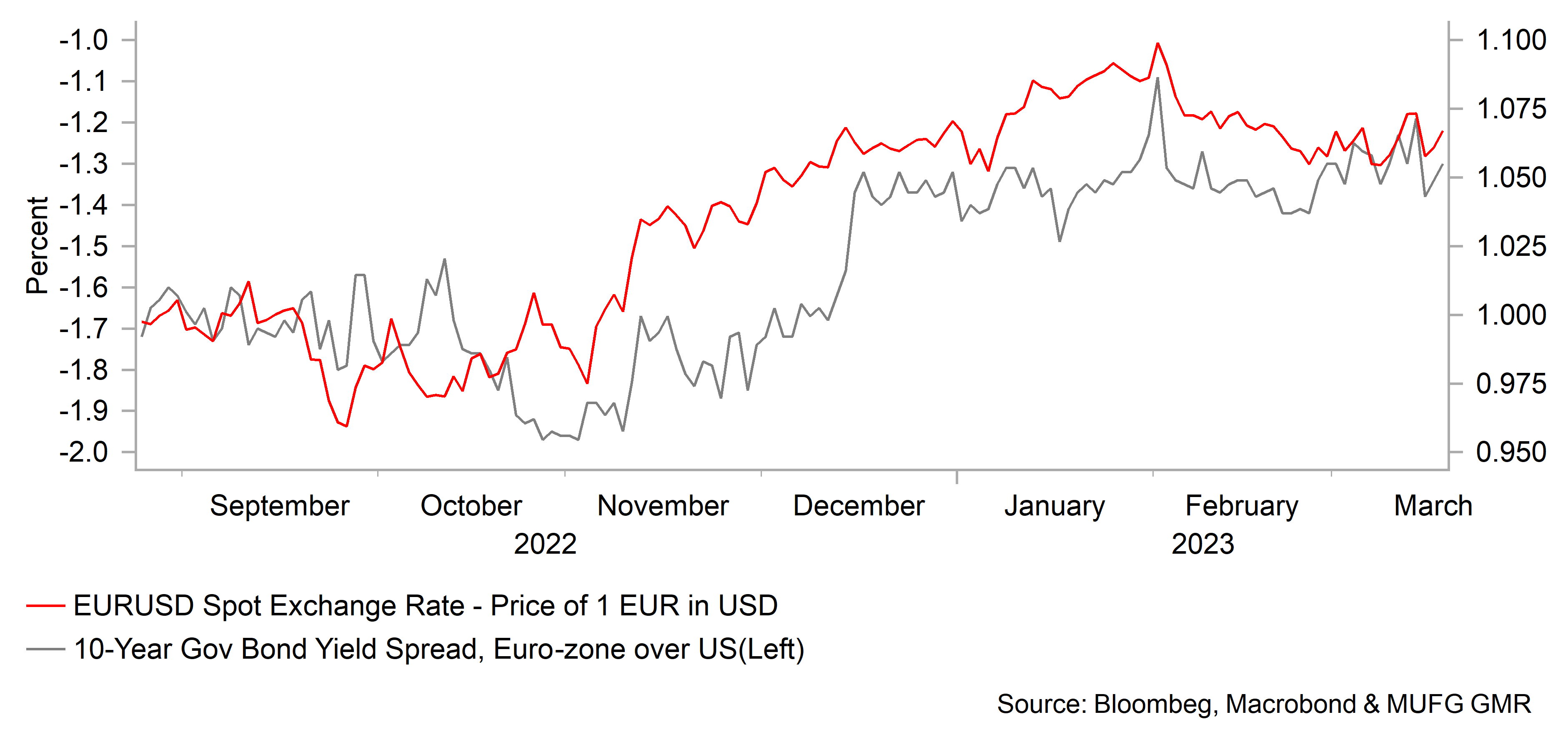

The outcome of the increase banking sector turmoil has been a narrowing of the spreads between the euro-zone and the US. The 2yr and 10yr bond spreads are now consistent with EUR/USD trading between 1.1000-1.1500. The banking sector outperformance, the beginnings of the reversal of last year’s energy ToT shock all point to building support for EUR/USD and a move higher through to end-2023

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

Policy Rate |

3.00% |

3.00% |

3.25% |

3.25% |

3.00% |

|

3-Month Bill |

2.71% |

2.90% |

2.70% |

2.50% |

2.30% |

|

10-Year Yield |

2.29% |

2.50% |

2.40% |

2.20% |

2.00% |

The 10-year German bund yield fell sharply in March, by 36bps to close at 2.29%. As was the case elsewhere, yields fell sharply due to the increased turmoil in the US regional banking sector and due to the near-collapse of Credit Suisse. While the ECB did raise the policy rate as expected, by 50bps, there was a change in guidance with the ECB no more data-dependent on future decisions. We previously assumed a further 50bps of tightening and we maintain that view although there is a greater risk of the ECB falling short of that and only hiking once more. That will be dependent on whether we get further crises of confidence in banks or not. The inflation backdrop does look set to improve with favourable base effects set to take annual CPI notably lower. The flash CPI estimate for March showed a sharp drop from 8.5% in February to 6.9%. Most ECB officials have stated that the ECB needs to separate the fight between inflation and measures to ensure financial market stability. Of course that separation is only feasible for so long and if financial market turmoil was to escalate on a more sustained basis, yield levels are likely to be lower than we assume

US banks were underperforming prior to SVB collapse

EUROPEAN VS. US BANKS EQUITY PERFORMANCE

Higher yields in the euro-zone are offering more support for the EUR

EUR/USD VS. LONG-TERM YIELD SPREAD

Pound Sterling

|

Spot close 31.03.23 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

EUR/GBP |

0.8782 |

0.8700 |

0.8700 |

0.8750 |

0.8800 |

|

GBP/USD |

1.2370 |

1.2640 |

1.2870 |

1.3030 |

1.2730 |

|

GBP/JPY |

164.40 |

163.10 |

163.50 |

162.90 |

156.50 |

|

Range |

Range |

Range |

Range |

||

|

GBP/USD |

1.1800-1.2800 |

1.2000-1.3000 |

1.2100-1.3200 |

1.2200-1.3400 |

MARKET UPDATE

In March the pound strengthened against the US dollar in terms of London closing rates from 1.2116 to 1.2370. However, the pound weakened very modestly against the euro, from 0.8759 to 0.8782. The BoE at its meeting in March raised the official Bank rate by 25bps to 4.25%, following 390bps of rate hikes in this tightening cycle. The BoE commenced QT in November last year and completed in January the sales of Gilts purchased under the emergency purchase program following the turmoil last year when a poorly delivered fiscal plan caused a crisis of confidence

OUTLOOK

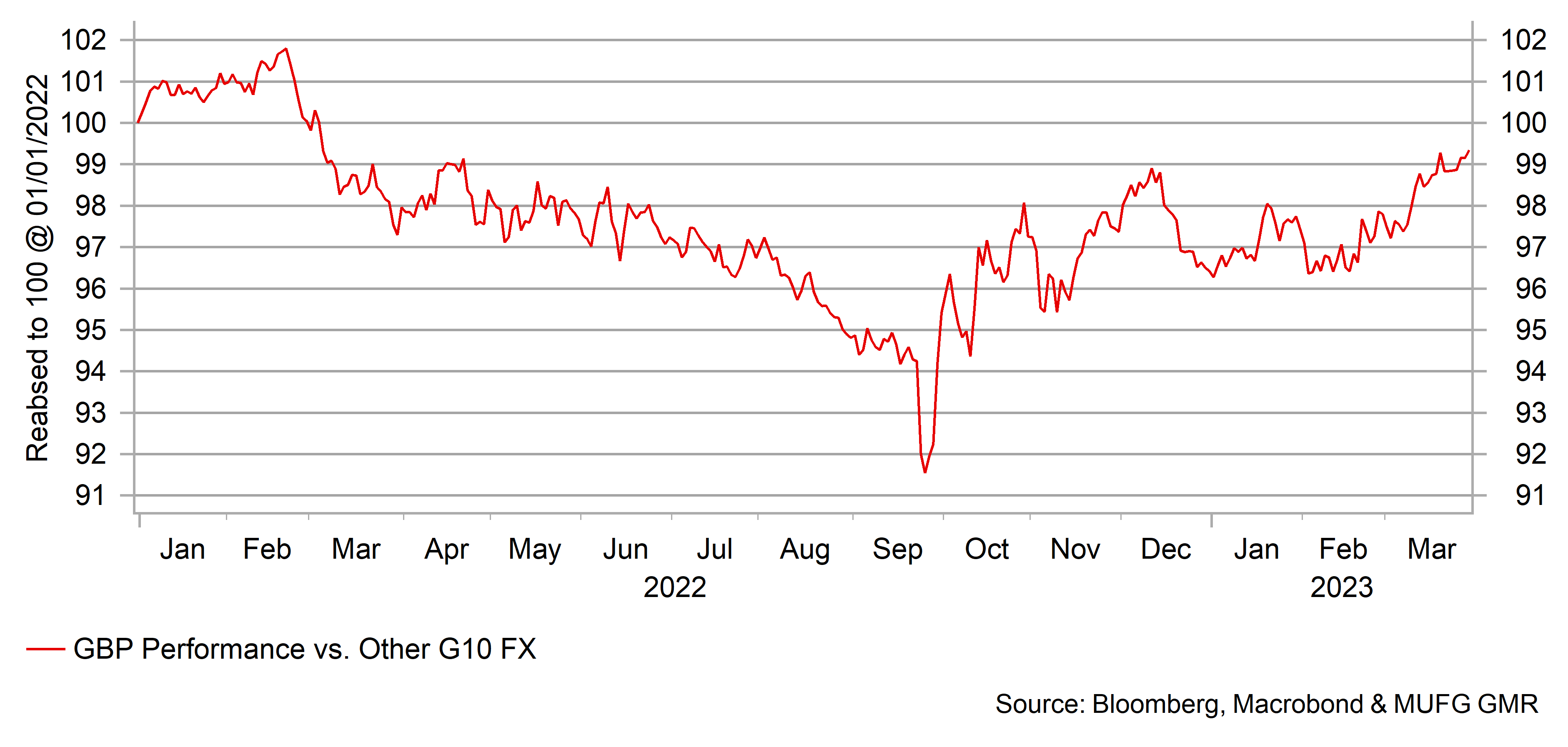

The pound ended March as the best performing G10 currency on a year-to-date basis which we believe reflects the degree of pessimism that was priced into the pound following last year’s political instability and the turmoil in the Gilt market. PM Rishi Sunak has restored some political stability as has Chancellor Hunt. The budget presented in March was viewed as balanced with some giveaways but also offset by tax increase measures like the increase in the corporation tax from 19% to 25%. Importantly, the budget, due to lower inflation, provided some additional fiscal space in order to offer higher public sector wages that looks likely to bring an end to some of the strike actions within the NHS and transport. Finally, a deal on the Northern Ireland Protocol, even without DUP support, has helped lift optimism of better UK-EU relations going forward. All of these factors have helped change the political landscape relative to the end of last year.

The turmoil in banking sector stocks did not stop the MPC from hiking at its meeting in March and the guidance on the possibility of hiking again if inflation pressures are stronger was maintained. UK bank stocks declined by a similar extent to Europe and a little less than in the US. The Financial Policy Committee (FPC) also met in March but saw no need to alter the counter-cyclical buffer and repeated that the UK banking sector was resilient. However, the turmoil in bank stocks in March could well have implications for the flow of credit going forward and with inflation also set to slow noticeably over the coming months, we expect the BoE to now pause and ultimately end its tightening cycle. M4 money supply data for February did reveal tighter credit conditions were already developing prior to the banking sector turmoil. Net lending by UK Monetary Financial Institutions declined by GBP 4.7bn, the largest contraction since December 2011. Lower energy prices will also start to lower annual CPI more clearly going forward with a large base effect kicking in in Q2. The government’s budget included a forecast of annual inflation falling to 2.9% by the end of this year.

With the dollar set to weaken as the Fed pauses and the US economy weakens, we are maintaining our view of GBP/USD moving up to levels just over 1.3000. That level does also imply some outperformance versus non-dollar currencies as falling inflation helps UK consumer sentiment which was hit harder and given the potential for some further improvement in UK-EU relations

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

Policy Rate |

4.25% |

4.25% |

4.25% |

4.00% |

3.50% |

|

1-Year Yield |

4.03% |

4.00% |

3.90% |

3.60% |

3.20% |

|

10-Year Yield |

3.49% |

3.60% |

3.40% |

3.20% |

3.00% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

The banking sector turmoil in March was the primary driver of the sharp decline in the 10-year Gilt yield which fell 34bps to close at 3.49%. The move was similar to elsewhere and reflected the initial safe-haven demand and then the pricing of less monetary tightening going forward. We are maintaining our view that the BoE’s terminal rate will be the level reached in March – 4.25%. Granted the risk to this view if there are no further bouts of banking sector ructions is that the BoE hikes again but even without further bank problems, the outlook for inflation should be consistent with a pause. The guidance from the MPC is a further rate hike is conditional on inflation pressures being stronger than anticipated. The MPC was partly compelled to act given the CPI data the day before the meeting was stronger than expected. Goods inflation remains elevated at 13.4% while services inflation accelerated but was weaker than the BoE had assumed. With the FOMC potentially cutting in Q3 and Q4 and with UK growth weaker than elsewhere we believe the BoE will have scope to ease its monetary stance by year-end. This scenario and the potential for weaker credit growth should result in 10-year drifting gradually lower.

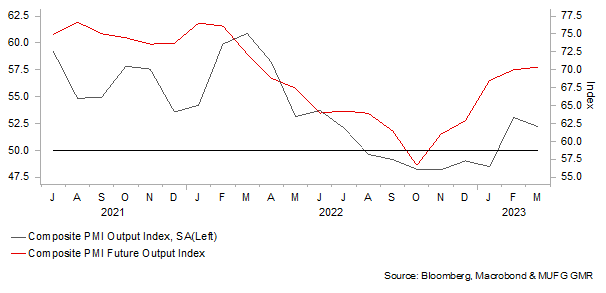

Leading indicators help to ease UK recession risk

UK PMI SURVEYS

GBP has outperformed at start of this year

PERFORMANCE OF GBP VS. OTHER G10 FX

Chinese renminbi

|

Spot close 31.03.23 |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

USD/CNY |

6.8675 |

6.7500 |

6.6500 |

6.5500 |

6.4500 |

|

USD/HKD |

7.8498 |

7.8300 |

7.8100 |

7.8000 |

7.8000 |

|

Range |

Range |

Range |

Range |

||

|

USD/CNY |

6.6000-6.9500 |

6.5000-6.8500 |

6.4000-6.7500 |

6.3000-6.6500 |

|

|

USD/HKD |

7.8100-7.8700 |

7.7900-7.8500 |

7.7800-7.8400 |

7.7700-7.8300 |

MARKET UPDATE

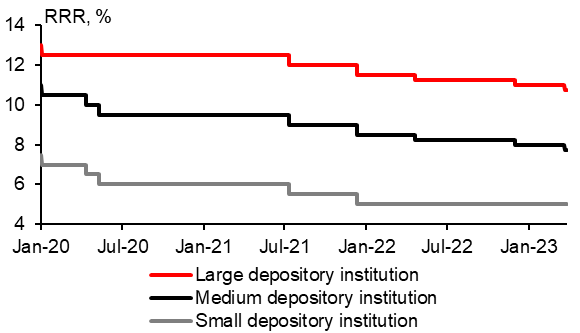

In March the Chinese yuan appreciated by 1.0% against the US dollar to 6.8675. PBOC kept its 1-year MLF rate unchanged at 2.75% on 15th March and held 1-year and 5-year LPRs unchanged at 3.65% and 4.30% respectively on 20th March. On 17th March, PBOC announced a cut to the reserve requirement ratio (RRR) for all banks, except those that have implemented a 5% RRR, by 0.25 percentage point, effective from 27th March, bringing the weighted average RRR level for the whole banking system to 7.6%.

OUTLOOK

China’s March PMIs implied that the overall economy may be picking up steam in March, with composite PMI increasing further to 57 from February’s 56.4. Non-manufacturing PMI surged to 58.2 from 56.3 in February, construction and services PMIs improved to 65.6 and 56.9 respectively in March as well. The improvement of construction PMI was consistent with the recent improvements in the real estate sector. However, the manufacturing PMI fell a bit to 51.9 in March from February’s 52.6, implying possible weak export growth for the month. Continued positive developments were seen in the real estate sector. A report released by the Beike Research Institute on 20th March indicated that the average mortgage rate for a first-time buyer in a hundred Chinese cities edged slightly down from February’s 4.04% to 4.02%, the lowest since 2019 in March. And the processing time of mortgages also was accelerated. The report said that the average process time in a hundred cities was reduced to 21 days in March, the fastest pace since 2019. In light of these, we expect improvements in March data for macro indicators released in mid-April. Still, domestic employment was a weak spot, with the surveyed urban jobless rate and youth jobless rate (aged 16 to 24) worsening to 5.6% and 18.1% respectively in February. We expect the government to roll out further stimulus approaches to improve the situation, as the government vowed to put employment as its policy priority, setting a goal to create 12 million new urban jobs in 2023 (up from 2022’s 11 million). This year’s college graduates are expected to reach 11.58 million people.

The stronger equity inflows helped strengthen CNY in March, the net foreign institutional investment in China equities increased to USD5,169mn in March from February’s USD1,398mn. We maintain our view of a trend appreciation of CNY against the US dollar for the rest of this year, due to a potential stronger capital inflow and better sentiment towards the China market. China will deliver more attractive performance in both absolute and relative terms in the performances of economic fundamentals and equities. However, due to the recent incidents of SVB and other financial institutions, we expect a potential tighter liquidity condition in DMs compared with before, which could add an extra layer of constraint on economic development, and a subsequently more pessimistic exports outlook for China. Hence we revise USD/CNY to 6.65 (from 6.60) for Q3 end, and revise USD/CNY to 6.55 (from 6.5) for Q4 end.

INTEREST RATE OUTLOOK

|

Interest Rate Close |

Q2 2023 |

Q3 2023 |

Q4 2023 |

Q1 2024 |

|

|

Loan Prime Rate 1Y |

3.65% |

3.65% |

3.65% |

3.65% |

3.65% |

|

MLF 1Y |

2.75% |

2.75% |

2.75% |

2.75% |

2.75% |

|

7-Day Repo Rate |

2.00% |

2.00% |

2.00% |

2.00% |

2.00% |

|

10-Year Yield |

2.86% |

2.95% |

3.00% |

3.05% |

3.10% |

* Interest rate assumptions incorporated into MUFG foreign exchange forecasts.

China’s 10-year government bond yield fell 6bps to 2.85% at the month end of March. China’s bond yields extended their declines after the announcement of RRR cut on 15th March due to induced better interbank funding condition. Looking ahead by assessing the various sub-PMI indexed of prices in March, CPI inflation may weaken further in March. Non-manufacturing input price sub-PMI index declined to 50.3 in March from February’s 51.1; non-manufacturing sales price sub-PMI index declined to a contractionary 47.8 in March from February’s 50.8; manufacturing producer price sub-PMI index declined to 48.6 in March as well. Domestic inflationary pressures have eased significantly lately, and the risk of deflation is getting higher. Against a still quite moderate pace of economic recovery, uneven recovery, a further falling inflation likely keeps monetary policy moderately loose stance so to better support the economy and prevent risks. We see room for China’s 10-year government bond yield to further decline moderately in near term.

PBOC cut RRR in March 2023 to support recovery

PBOC ANNOUNCED RRR CUT LAST MONTH

Source: CEIC, MUFG GMR

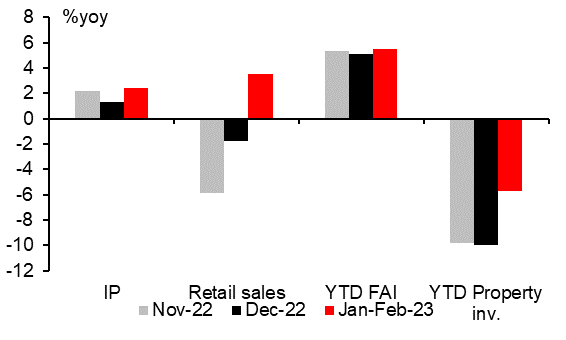

Improvement in year-over-year growth was broad-based for China’s major indicators in both supply and demand sides

JAN-FEB DATA CONFIRMS A MODERATE RECOVERY FOR 2023

Source: CEIC & MUFG GMR