Key Points

Please click on download PDF above for full report

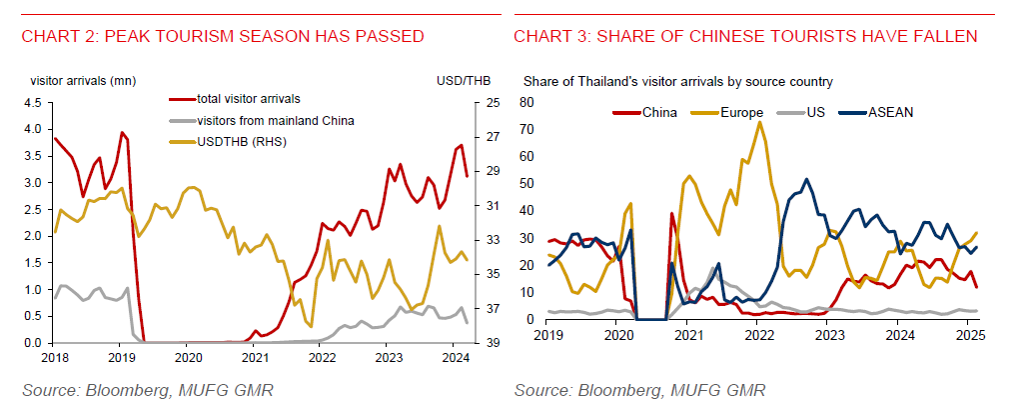

- The earthquake in Thailand on 28 March will weigh heavily on the tourism industry, at a time when safety concerns over the kidnapping of a Chinese actor have already affected visitor arrivals from China. Indeed, Chinese tourists have fallen to 0.37mn in February, which was just 55% of what it was a year ago and about 35% of the pre-Covid level in February 2019. Before Covid, Chinese tourists accounted for about 27.5% share of total visitor arrivals in 2019. But this share has fallen to just 18.3% of the total (on a past 12-month basis) as of February.

- The negative impact on Thailand’s visitor arrivals could start to show up over the coming weeks, which will hurt the outlook for the accommodation and food services industry. In addition to that, property purchases, especially at the high-end segment, could also slow, compounding an already fragile property sector. The accommodation and food services industry, along with the real estate services industry, accounted for about 10% of the country’s total employment. Negative spillover effects on employment in these sectors will also dampen domestic private consumption growth.

- The Thai Hotels Association has predicted that visitor arrivals could decline by up to 15% or possibly even more in the next couple of weeks. Assuming that tourist arrivals would fall by 10%yoy during the lull tourism season over the next 6 months, we estimate that the potential economic impact could be up to 0.7ppt. We have lowered our forecast for Thailand’s GDP growth to 2.2% in 2025, from 2.8% previously, having also taken into consideration potential monetary policy easing to help provide support for consumers and businesses.

- With the natural disaster likely to pose additional hit to Thailand’s economy, we look for the Bank of Thailand to shift to a dovish stance, lowering the policy rate by another 25bps to 1.75% at the 30 April meeting to provide much needed support for growth. Moreover, Thailand’s headline inflation has been lacklustre, at 1.1%yoy in February, hovering near the lower bound of the central bank’s 1%-3% inflation target range. Core inflation has also been subdued at just 1%yoy in February, reflecting weak domestic demand. Also, in response to the crisis, the Bank of Thailand has instructed state banks to offer financial assistance and to provide liquidity to help support businesses.

- The natural disaster has also come at a time when Thailand’s economy will be facing US reciprocal tariff hikes. Thailand has a positive tariff differential of about 5% with the US. And if the US also takes into account value added tax, currently at 7% in Thailand, US could potentially impose up to 12% of tariff hikes on imports from Thailand. In this scenario, we estimate that Thailand’s GDP could be cut by about 0.3ppt.

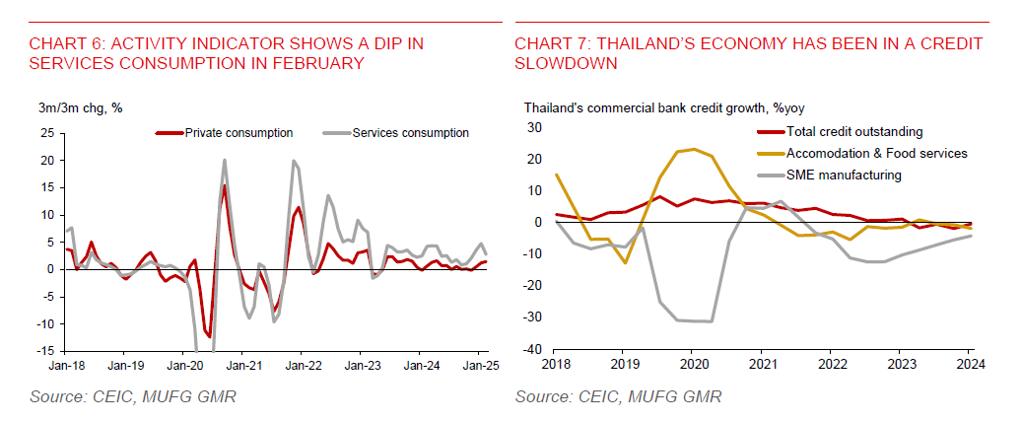

- Latest activity data also shows economic weakness in February. Private consumption slowed to 0.9%mom from 1.3%mom in January, while services consumption notably fell 1.3%mom from a 2% increase in January, in part reflecting a slowdown in tourist arrivals and related spending.

- Thai authorities have commented that financial services and payments systems are working normally following the earthquake. They have also sought to assure investors that fundamentals of corporates listed on Thai stock exchange are still sound. Nonetheless, there will be implications for financial markets. While Thailand’s SET index appears to be inexpensive, we remain cautious about the outlook for Thai equities, as company earnings could be impacted by both domestic and external trade headwinds. Tourism and leisure category accounted for about 1.7% of Thailand’s SET index as of end-March.

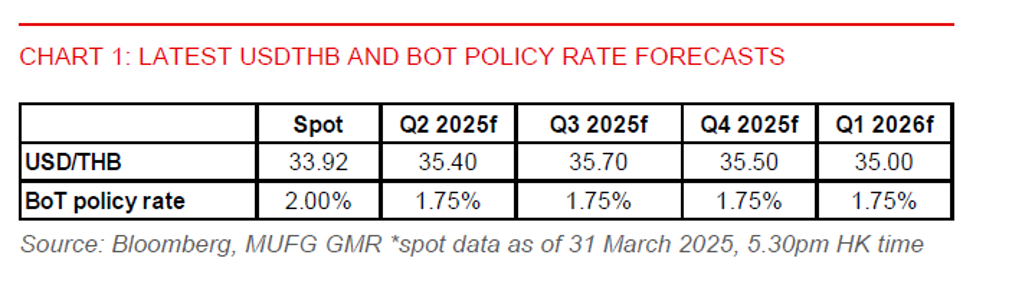

- In terms of our outlook for the Thai baht, we think its resilience may not last over the coming months. For now, rising gold prices and weak oil prices have provided support. Also, Thailand’s foreign reserves have risen to $247.1bn, while the current account was 2.4% of GDP in Q4, underpinned by tourism recovery. This brought the current account surplus to 2.1% of GDP in 2024, up from 1.5% of GDP surplus in 2023. That said, we forecast USDTHB to rise to 35.400-level against the US dollar this quarter, given a weaker outlook for domestic demand, tourist arrivals, and potential negative spillover effects from a weaker Chinese yuan.