China’s buoyant reopening is not yet spilling over into other EMs

Macro focus

Despite China’s GDP topping 9.1% on a sequential basis in Q1 2023 on a robust reopening, EM ex-China as a whole remains lacklustre. We highlight two key factors. First, the Chinese reopening has been less about infrastructure spending that historically channels effectively into other EMs, and more domestically contained thus far. Second, EM outperformed markedly against its US dollar beta in 2022 (driven by earlier rate hikes and steep real rate differentials), but since the US dollar peaked in October 2022, EMs have given up this outperformance as it appears the US dollar is more expensive than EMs are cheap – put differently, starting points matter, with EM resiliency against a stronger US dollar in 2022 signalling less potential on a weaker US dollar in 2023. Looking ahead, we acknowledge that the initial phase of the Chinese recovery is driven by consumption and the services sectors, and thus not benefitting EMs through the export angle (just yet), but we are convicted that the 2009 and 2016 China recovery playbook is on, but more a H2 2023 story (see here).

FX views

The upcoming FOMC decision this week could be pivotal for the US dollar (USD) and with it EM FX. Some officials, like Presidents Goolsbee and Bostic, have said that they do not expect a recession, and need to stay focused on inflation, but still want to take a more “prudent” approach. Whether a sign of increased inflation tolerance or a greater substitution from rate hikes to credit tightening, either are negative for the currency. From an EM FX perspective, declining rate volatility has been helpful in keeping the USD at bay. We believe this is key, reflecting how the USD is not responding as much to renewed expectations for the Fed to raise rates nor elevated US recession probabilities. This highlights how there is less fear of the Fed or US hard landing risks – core sources of comfort for EM FX.

Week in review

Consistent with the communication it provided recently, Hungary initiated policy normalisation by lowering the top end of its interest rate corridor – the overnight lending rate – by 450bp to 20.50%. Turkey and Russia both kept their policy rates unchanged at 8.50% and 7.50%, respectively, in line with our (and consensus) expectations. Inflation in Poland decreased from 16.1% y/y in March to 14.7% y/y in April on weaker food inflation and strong base effects. Finally, Qatar is expanding its LNG carrier fleet according to reports, booking slots for the next five years at major South Korean shipbuilding yards for a total order of 100 new carriers.

Week ahead

This week is set to see Czech Republic hold rates at 7.00%, inflation in Turkey to ease by 5.9ppts to 44.6% y/y in April and EM EMEA PMI readings for April. Beyond EMs, we expect a fairly busy week ahead in global markets, as both the FOMC (set to deliver a 25bp hike and signal a pause, but use language that would keep the optionality to adjust the rate path in either direction) and the ECB (set to deliver a 25bp and bring back forward guidance tied to incoming data) will release monetary policy decisions.

Forecasts at a glance

Whilst EMs continue to grapple with much the same themes at the turn of the year, we view the outlook as a tale of two halves in 2023. A fading boost from reopenings, a global manufacturing cycle downturn and tighter financial conditions are lumpy headwinds that will weigh on EM prospects in the first half of 2023. However, China’s zero COVID policy exit, the eventual end of rate hikes and a US dollar peak, all offer significant tailwinds to the EM complex in the second half of 2023 (see here). Whilst EMs continue to grapple with much the same themes at the turn of the year, we view the outlook as a tale of two halves in 2023. A fading boost from reopenings, a global manufacturing cycle downturn and tighter financial conditions are lumpy headwinds that will weigh on EM prospects in the first half of 2023. However, China’s zero COVID policy exit, the eventual end of rate hikes and a US dollar peak, all offer significant tailwinds to the EM complex in the second half of 2023 (see here).

Core indicators

While the cycle is still positive, March witnessed retrenchment in EM capital flows, down to USD9.4bn, with investors beginning to take a more cautious approach to EM assets as an early year rally ebbs.

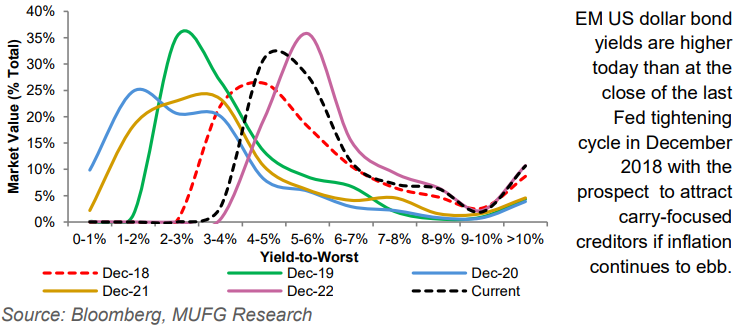

CHART OF THE WEEK: FED YELLS “JUMP” AND EM’S ASKS “HOW HIGH”

EM CURRENCY VOLATILITY VS UST 3 MONTH 2 YEAR SWAPTION VOLATILITY