Emerging markets derailed by higher for longer developed market rates

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

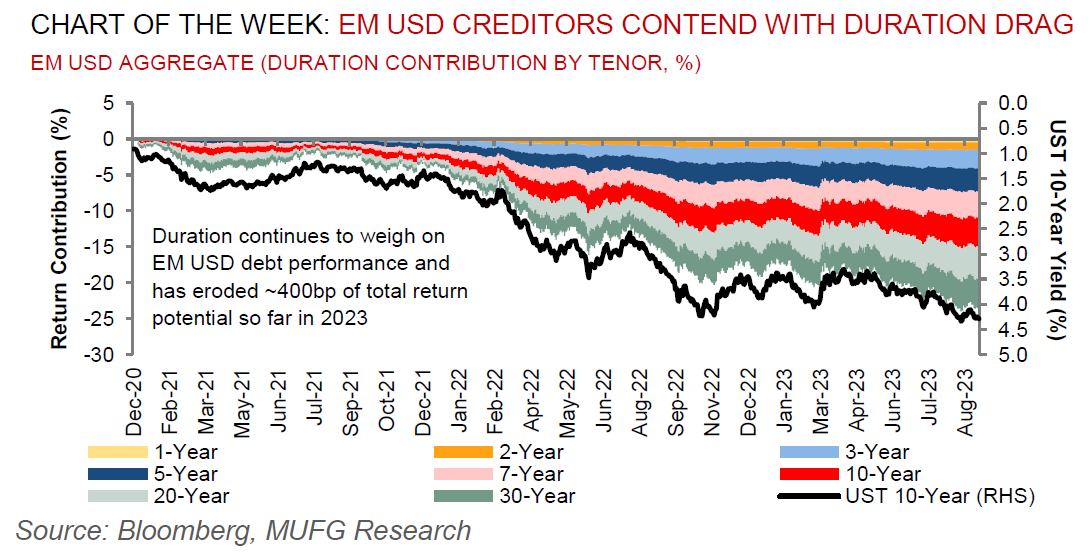

The ”higher for longer” narrative is evoking parallels to the 1990s, when tepid growth, rising debt defaults and a slew of FX devaluations loaded EM creditors with large losses. Carry has managed to insulate EM credit from higher US Treasury yields, yet the outlook remains firmly associated with US financial conditions. With US rates trading as if they are still in a bear market, we are cautious on the near-term EM outlook until we see signs of US weakness that allows the Fed to dial down its hawkish rhetoric.

FX views

The backdrop of higher for longer rates that also keep the USD supported, we view that spot returns for high-carry, cyclical EM currencies are increasingly becoming more tactical. Put differently, carry accrual may be best implemented through relative value, risk-neutral expressions. On the local side, the pace of policy easing will continue to be an important differentiator and, so far, BRL and MXN look to be the most insulated from real carry erosion and are also supported by resilient domestic economic growth.

Trading views

There was the hope that a type of self-correcting mechanism will exist for higher rates. But our view is that the market will have to live with it. The vol in EMFX is lower that we would have expected with worries over authorities supporting their currencies a key reason perhaps. Thailand is at an interesting point with nearly all cyclical factors working against it right now.

Week in review

Czech Republic and Hungary held interest rates. Poland’s September inflation rose 8.2%y/y. Meanwhile, Saudi Arabia revised its medium-term budget balances – to run deficits on expansionary fiscal stance.

Week ahead

Rates setting meetings in Poland (MUFG and consensus: 25bp cut to 5.75%) and Romania (MUFG and consensus on hold at 7.00%). September’s inflation data will be out in Turkey (MUFG: 62.3% y/y; Consensus: 61.6% y/y).

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to IIF data, investors withdrew USD4.5bn from EM assets last week – USD3.6bn and USD0.9bn from equities and bonds, respectively.