Brace for impact as EMs will struggle under Trump 2.0

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

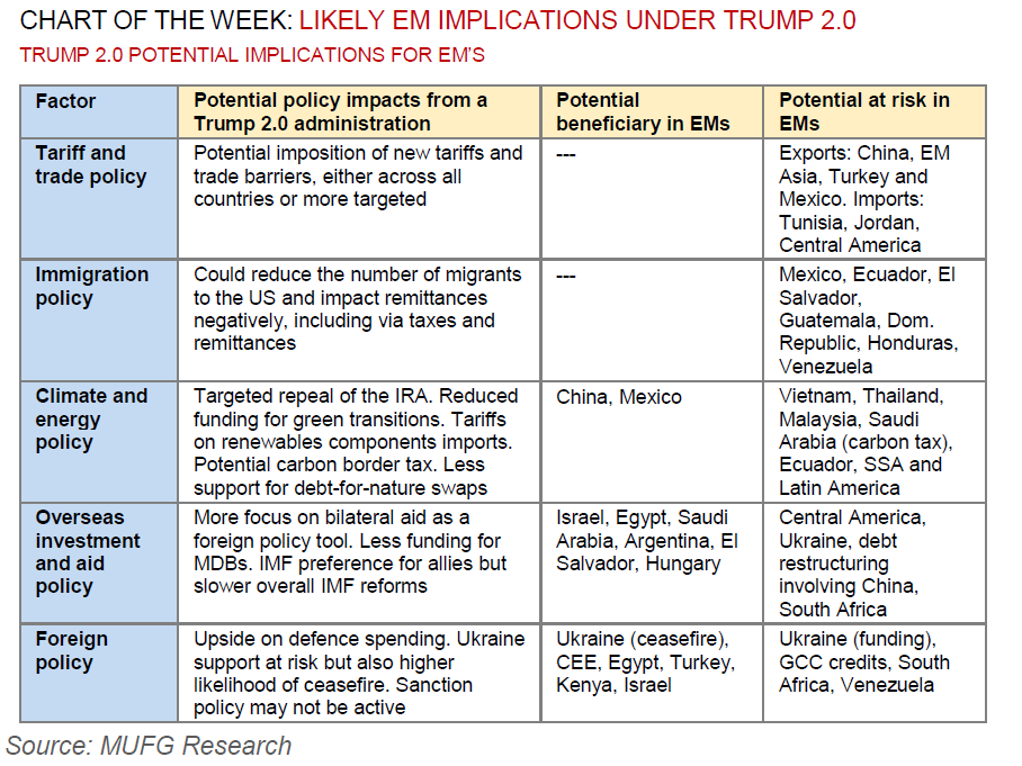

The recent EM asset sell-off has coincided with a rise in the probability of a Republican victory in this week’s US presidential elections across prediction markets. Investors seemingly are focused on both the extent to which a Republican victory is already reflected in global markets and the potential for further cross-asset moves on the actual election result. Looking past the fog of uncertainty, what is clear is that the combination of greater use of US industrial policy and higher-for-longer under a Trump 2.0 is unfavourable for EMs as it crowds-out investment and capital inflows. Buckle up, put your helmet on and brace for further EM volatility ahead – the whiplash could be severe (and immediate). Markets are likely to have enough information within a few hours of polls closing to trade the likely presidential winner – even if sources take longer to make the call.

FX views

Emerging market currency performance has been mixed over the past week ahead of the US election. The election outcome will be pivotal for EM FX performance, while Fed policy update to take back seat in week ahead. The BCB is under pressure to deliver a larger hike to support the BRL amidst fiscal concerns. The CZK and PLN have been supported by paring back of investor pessimism over growth in Europe.

Week in review

The IMF released its regional Economic Outlook for the Middle East and Central Asia on 31 October, updating its growth projections for the region. For MENA, GDP growth is now expected at 2.1% in 2024, down from the 2.7% projected in April, and the 2025 forecast has been lowered to 4.0% from 4.2%. Dubai’s 2025-27 budget, was released last week and was the largest on record – allocating AED272bn (USD74bn) primarily toward infrastructure to drive growth. Real GDP growth in Hungary contracted for the third quarter, and weakened in the Czech Republic for the same period. Inflation in Poland edged higher in September, pushing rate cuts to 2025.

Week ahead

This week, there will be rates meetings in Poland (MUFG and consensus: on hold at 5.75%), the Czech Republic (MUFG and consensus: -25bps to 4.25%) and Romania (MUFG and consensus: on hold at 6.50%). Additionally, CPI data will be released in Turkey (MUFG: 48.5% y/y; consensus: 48.3% y/y).

Forecasts at a glance

Growth across the EM universe is set to stabilise as domestic fundamentals offset external drags, with some rotation from the largest to smaller EMs. Inflation and interest rates are both “over the hump” – disinflation is progressing, and the decline in rates will continue and broaden for the remainder of 2024.

Core indicators

The latest weekly IIF flow data signalled that EM securities witnessed inflows of USD0.3bn in the week ending 1 November. The breakdown suggests that equities drove the inflows (USD0.4bn) whilst debt (USD-0.1bn) fell over the week.