To read the full report, please download the PDF above.

Higher-for-longer narrative is testing EM resilience

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

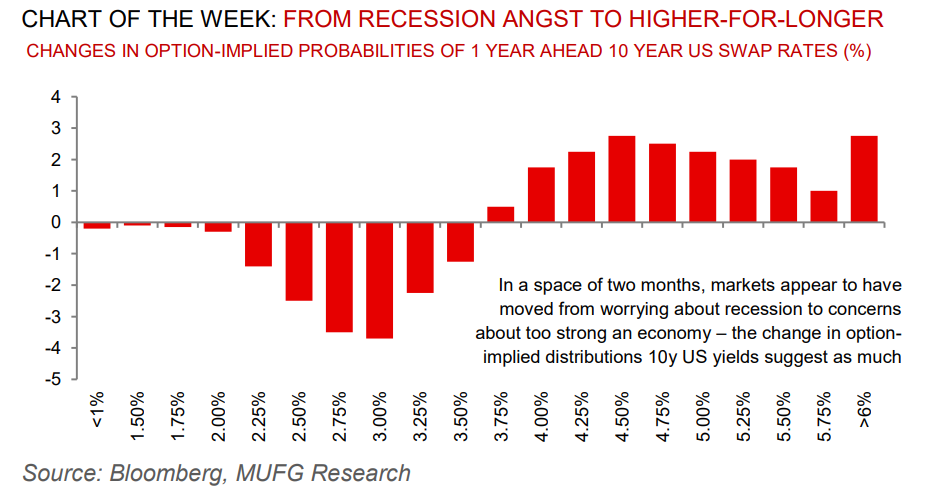

Not long after the what appeared the start of the EM monetary easing cycle led by LatAm in July (see here and here), heightened sensitivity surrounding the sharp steepening of the US yield curve, as well as sluggish Chinese growth, is seeing EM central banks join their DM peers in pushing back and erring on the side of prudence. We highlight three takeaways for EMs post the August sell-off. First, while total returns were largely eroded by the sharp move higher in US yields, spreads were relatively resilient, reflecting lower sensitivity to China growth compared with other EM assets. Second, a flight to quality but with notable exceptions on the back of idiosyncratic developments in the likes of Turkey. Third, stronger summer technicals, driven by negligible EM USD issuance in August. Looking ahead, with the market narrative moving towards DM rates remaining higher for longer, EM total returns will remain heavily conditional on the trajectory of US yields. From a spreads standpoint, the relative resilience in August, combined with the scope for higher H2 2023 issuance, which needs to be absorbed, should limit the scope for further spread compression.

FX views

It has been another mixed week for EM FX performance that has seen our MUFG EM FX index fall back towards last month’s year to date lows against the USD. The mixed price action suggests that market participants are not yet convinced that policy stimulus measures rolled out by policymakers in China will be sufficient to drive a significant improvement in the economic outlook. The latest policy step was the decision to lower the FX RRR by 2ppts to 4.0%. It sends a clear signal that domestic policymakers do not want a repeat of the period between 2015 and 2016 when CNY weakness contributed to heavy capital outflows. As we saw at the end of last year, if the stimulus measures prove successful in restoring confidence in China’s growth outlook they could provide an important bullish turning point for EM FX.

Trading views

Overall the pieces are starting to fall in place for EMFX to perform well this month. Global growth is being downgraded enough to see peak rates in developed markets while at the same time not being bad enough to prompt recessionary fears. This is a perfect if somewhat delicate combination and it also provides a platform for EM carry to do well especially as the fall in FX implied vols shows little sign of turning around. Though given the importance of RMB to the EM FX basket we need this to play ball. The carry in turkey alongside a strong move by the CBRT makes us positive on the currency.

Week in review

Turkey’s Q2 2023 GDP came in at 3.8% y/y, while Turkey’s August inflation surged to 58.9% y/y. Meanwhile, Poland’s August inflation fell but remained above expectations. Qatar’s Q2 2023 GDP came in lower at 2.7% y/y; while Hungary’s policy decision was in line with its monetary policy normalisation.

Week ahead

In the week ahead, we have rates meetings in Israel (MUFG and consensus: on hold at 4.75%) and Poland (MUFG and consensus: -25bp to 6.50%). Meanwhile, South Africa will release both Q2 2023 GDP (MUFG and consensus: up 1ppt to 1.2% y/y) and balance of payments data (MUFG -2.1%; consensus -2.3%)

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to data from the IIF, EM Fund flows have slowed and in the week ending 1 September, EM funds recorded the fifth consecutive week of net outflows of USD1.6bn - USD1.4bn and USD0.2bn withdrawn from EM equity and bond funds, respectively.