To read the full report, please download the PDF above.

Navigating the potholes under higher for longer DM rates across the EM complex

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

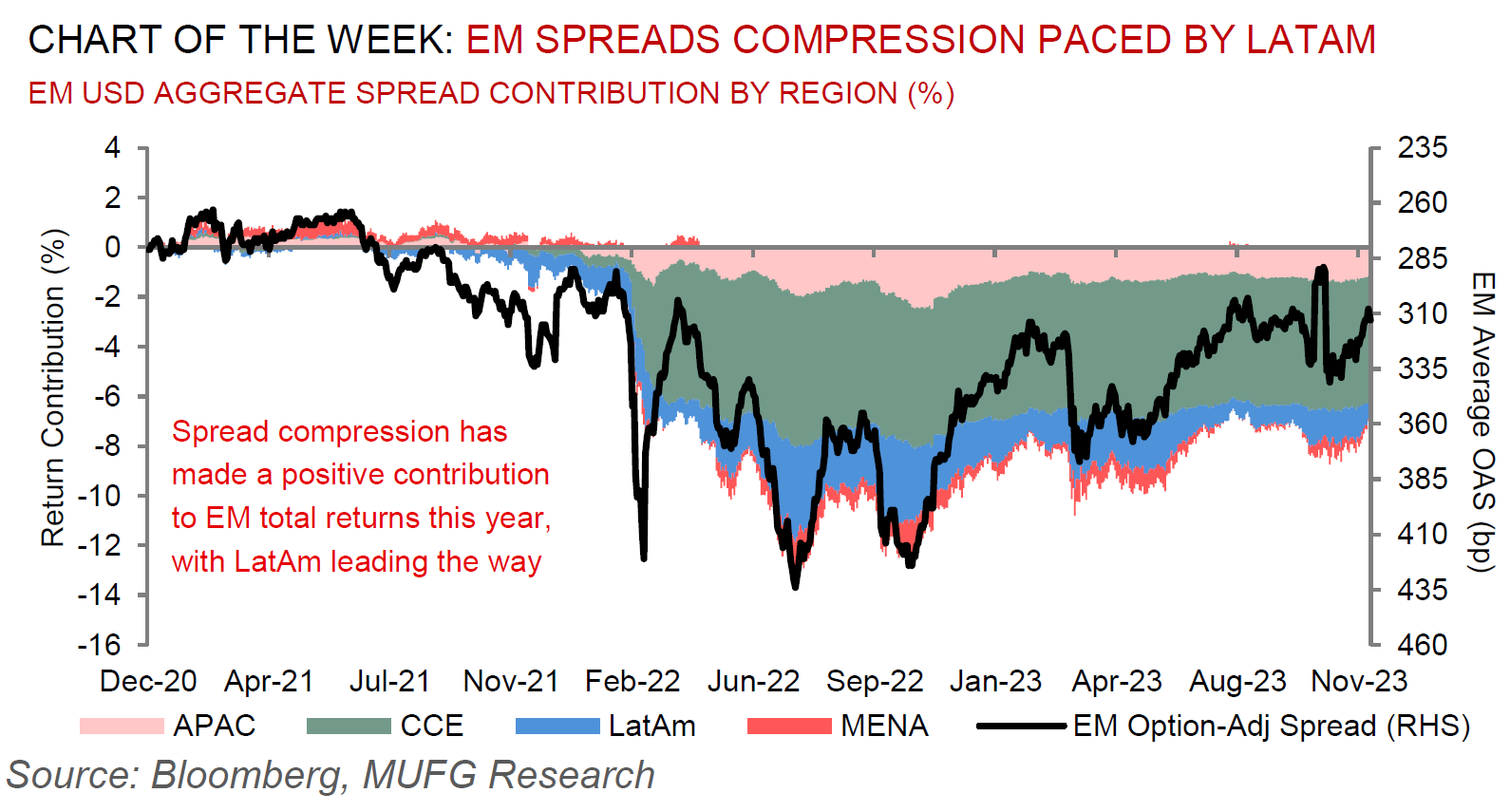

The November rally has brought year-to-date total returns in the EM complex well into positive territory. The main reason for the spread resilience among most EM sovereign USD bonds is their significant improvement in external vulnerabilities since the creation of the asset class. There are more countries in the index, and many of them have relatively low external debt and higher reserves. This group has seen spreads trading in a relatively tight range within one standard deviation this year. A number of sovereigns that do have higher external vulnerabilities quickly lost market access in a “low growth, high rates” world. While the recent market pricing of lower US Treasury yields has been helpful to countries with higher external vulnerabilities, they also remain the most vulnerable if risk sentiment suddenly turns. Indeed, this year has seen a group of sovereigns in the Sub-Saharan Africa (SSA) region hovering in and out of distressed levels depending on market conditions (we define that as USD bond spreads above ~1,000bp), and while it is not our base case that they will lose market access, they remain the most vulnerable should the macro backdrop turn less friendly. Under the scenario where the Fed cuts the policy rate in early 2024, in line with our US rates strategist call, we see room for further spread compression coming from EM distressed credits.

FX views

Emerging market currencies have continued to lose upward momentum against the USD over the past week even as US yields have fallen to fresh lows. NFP report is provide important test of recent dovish repricing of Fed policy expectations and USD has proven more resilient to falling US yields over past week.

Trading views

The market seems to be pricing a hard landing scenarios, but this does not seem evident in vol markets. A steady NFP will see us try to engage in EM longs once again.

Week in review

Bank of Israel remained on hold, but reduced growth forecasts for 2023 and 2024. Poland CPI came in at 6.5% y/y. Turkey’s Q3 GDP data surprised to the upside, printing at 5.9% y/y, while the November CPI slowed to 61.6% y/y.

Week ahead

In Poland, we expect the NBP to remain on hold. November CPI data in Hungary and Turkey will be in focus, with the central bank expecting to see further easing in sequential inflation.

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

EM inflows totalled USD1.1bn in the week ended 01 December, with inflows into equities and bonds at USD1.1bn and USD0.01bn, respectively.