To read the full report, please download the PDF above.

Ten questions for 2024

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

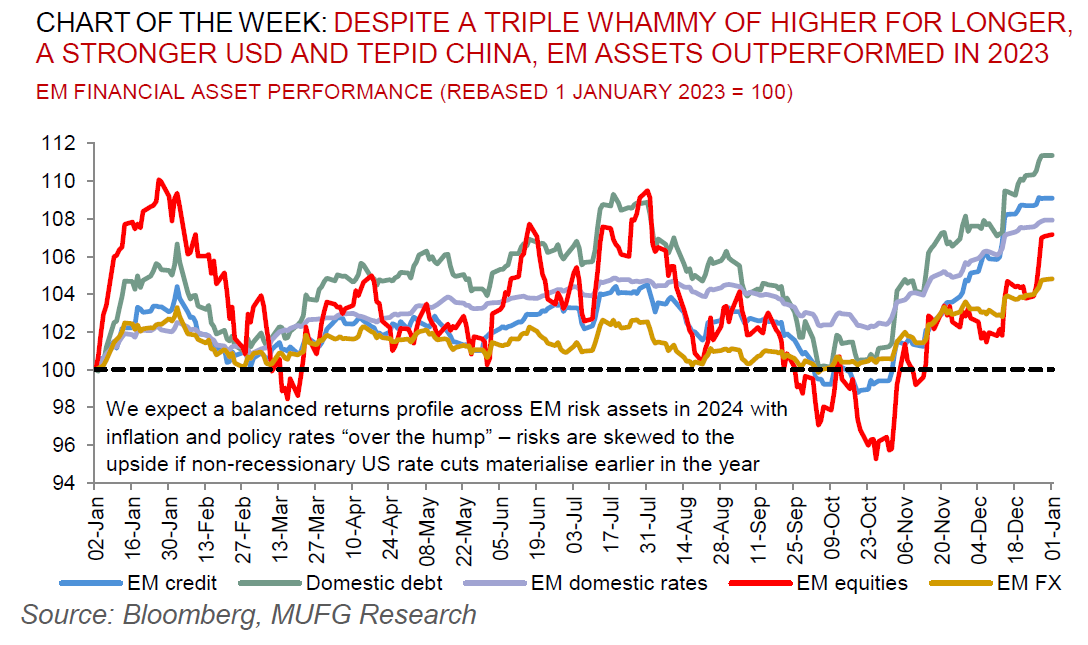

We wish all of our clients a happy, healthy and prosperous 2024. In the first EM EMEA Weekly of this year, we examine what we believe are the ten most important macro questions for 2024. Please see here for our comprehensive EM 2024 outlook.

FX views

EM FX have suffered setback at the start of the new calendar year giving back gains recorded over the holiday period. Fed rate cut expectations as soon as March are pared back, while speculation over slower pace of QT intensifies. Fed decision to slow QT would boost demand for high beta EM FX.

Trading views

A reversal of year ahead trades plus weak PMIs has seen funders get hurt once again. It’s a new year but not a new theme in Chinese asset underperformance. Given the inflation backdrop post COVID, it is little wonder that all the foreign money has not returned to EM bond markets – this may be the time when this changes, and thus we are cautiously optimistic.

Week in review

Inflation in Poland surprised to the downside in December whilst inflation rose in Turkey during the same month.

Week ahead

Rates meetings to be held in Poland and Romania. Inflation for December will be released in Egypt, Czech Republic, Hungary, Romania, Russia and Ukraine. Finally, current account data for November will be released for Turkey.

Forecasts at a glance

Growth across the EM universe is set to stabilise as domestic fundamentals offset external drags, with some rotation from the largest to smaller EMs. Inflation and interest rates are both “over the hump” – disinflation is progressing, and the decline in rates will continue and broaden in 2024 (see here).

Core indicators

EM securities attracted around USD43.4 bn in November 2023 – with inflows into equities and bonds at US14.8bn and USD28.6bn, respectively.