Declining headline, persistent core bodes ill for the inflation (and rates) outlook

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

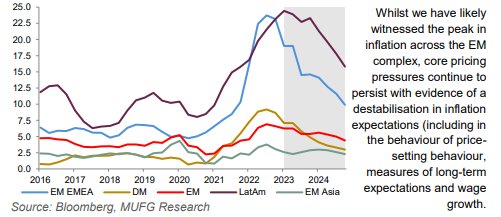

Despite some cause for optimism on the outlook for EM EMEA growth with our nowcast model pointing to a trough in economic activity in Q1 2023 (see here), it is difficult to extend that optimism to inflation. On the positive side, headline inflation rates across EM EMEA have (finally) started to decline, driven by strong base effects in energy and food inflation. However, notwithstanding the declining trend, inflation data in EM EMEA has continued to surprise to the upside in recent months, driven by stronger-than-expected core inflation dynamics. Even if one takes a relatively optimistic view on the outlook for global inflation, the ongoing rise in underlying inflationary pressures and the de-anchoring of inflation expectations in EM EMEA economies are reasons to expect high inflation to prove more persistent. Given the strength of underlying inflationary pressures, our front-end interest rate views are more hawkish than market pricing across most of the region (notably for the CEE-4, Egypt, Russia and Turkey) and do not anticipate any rate cuts until 2024.

FX views

Emerging market currencies have strengthened on the whole against the USD over the past week although our MUFG EM FX index is still trading just below year to date highs from earlier in the year. Emerging market currencies have derived support from last week’s less hawkish policy update from the Fed that has reinforced market expectations that it has reached the end of their hiking cycle. While the Fed did not explicitly signal that it had paused their hiking cycle, we believe there is a higher hurdle now for further hikes in the near-term.

Trading views

While we think carry trades could unwind it is hard to go against such a strong trend, better is to put on paid rates positions in some local markets. Turkish elections may be very closely watched by locals but contagion to broader EM universe should be limited for now, big positive reaction may have some effect but that is a month or more down the line.

Week in review

Despite growth worries and banking angst in the developed markets, April PMI manufacturing data in EM EMEA countries improved over the previous month reading. Meanwhile, Turkey's April inflation came in at 43.7% y/y, from 50.5% in March, below our (and consensus) expectations, owing to a larger-than-expected fall in the energy component. The Czech National Bank (CNB) kept rates on hold at 7.0% as expected with a hawkish bias. Finally, Fitch downgraded Egypt to B (negative) from B+ (negative) citing high uncertainty on the exchange rate trajectory and reduced external liquidity buffers.

Week ahead

This week we will have rates decisions in Poland (MUFG and consensus on hold at 6.75%) and Romania (MUFG and consensus on hold at 7.00%). April CPI data will be released in Hungary, the Czech Republic, Romania Egypt and in Russia – all of which are set to show headline inflation easing last month (albeit core remaining elevated in most places). Beyond EMs, the main data print that investors will be focusing on will be the US CPI release on 10 May.

Forecasts at a glance

Whilst EMs continue to grapple with much the same themes at the turn of the year, we view the outlook as a tale of two halves in 2023. A fading boost from reopenings, a global manufacturing cycle downturn and tighter financial conditions are lumpy headwinds that will weigh on EM prospects in the first half of 2023. However, China’s zero COVID policy exit, the eventual end of rate hikes and a US dollar peak, all offer significant tailwinds to the EM complex in the second half of 2023 (see here).

Core indicators

According to IIF data, EM funds witnessed minor weekly outflows to the tune of USD0.9bn, with the bond outflows at USD0.5bn and equity outflows at USD0.4bn in the week ending 5 May.

CHART OF THE WEEK: PEAKING BUT HIGHER-FOR-LONGER ON INFLATION