When visibility is low and volatility is high, EM carry prevails

Macro focus

The external picture continues to be uncertain with DMs struggling to balance disinflation and financial stability – keeping global macro visibility low and volatility high. For EMs, the complex is set to benefit from the pivot of relative growth momentum with a rebounding China and surprisingly resilient Europe. As EM central banks generally are not constrained by financial stability concerns and the focus is still on inflation, we believe a similar disappointment on the monetary policy front is also a risk, with so many rate cuts already priced in across EM yield curves. Thus, relatively high front end rates both in nominal and real terms compared to DM as well as a benign US dollar outlook argue for EM carry trade in high-yielders in a foggy macro environment. Notably, EM carry supremacy is clear in positive real rate EMs that also act as a buffer with an extra risk premium, namely, most of LatAm, South Africa, India and Indonesia.

FX views

The recent rebound for EM currencies against the USD has lost upward momentum at the start of this month following on from strong gains recorded during the second half of March. There has though been a wide divergence in performance amongst emerging market currencies. One constant has been the continued underperformance of the RUB which is well course to be the worst performing emerging market currency for the second consecutive month.

Trading views

Coming back from extended holidays the first observation is how large a rally EM has had over the last few weeks. A couple of currencies, like ZAR, have needed supportive action on the domestic front to rally. However, for most it has been a case of global betas and the fall in the USD terminal rate as the key driver. We think FX is taking its cues from vols and equities. The narrative of the US landing seems to have gone full circle, and the market may be getting too complacent on US landing stories while under-pricing Chinese reopening ones. Also, local stories are taking place that merit consideration such as the Turkish election and SARB’s actions to hike rates

Week in review

The EM EMEA composite PMIs for the month of March 2023 improved marginally, while continuing to remain in the expansionary side. Credit rating agency Fitch upgraded Saudi Arabia’s long-term foreign currency issuer default rating to A+ from A keeping the outlook stable. In line with the consensus and our expectations, the National Bank of Romania (NBR) kept the policy rate on hold at 7.00%, leaving rates unchanged for the second consecutive meeting after 11 successive hikes since October 2021. Finally, the National Bank of Poland (NBP) kept the policy rate unchanged at 6.75% for the seventh consecutive month, in line with our (and consensus) expectations.

Week ahead

In the coming week, March inflation data will be published across the region, in the Czech Republic, Egypt, Israel, Hungary, Romania and Russia. Bar Egypt (which is being challenged from acute FX weakness), we anticipate headline inflation to fall in all jurisdictions driven by base effects and lower energy prices (although with differing degrees of speed). Beyond EMs, a key focus this week will be towards the US CPI and retails sales releases on 12 and 14 April, respectively.

Forecasts at a glance

Whilst EMs continue to grapple with much the same themes at the turn of the year, we view the outlook as a tale of two halves in 2023. A fading boost from reopenings, a global manufacturing cycle downturn and tighter financial conditions are lumpy headwinds that will weigh on EM prospects in the first half of 2023. However, China’s zero COVID policy exit, the eventual end of rate hikes and a US dollar peak, all offer significant tailwinds to the EM complex in the second half of 2023 (see here).

Core indicators

While the cycle is still positive, March witnessed retrenchment in EM capital flows, down to USD9.4bn, with investors beginning to take a more cautious approach to EM assets as an early year rally ebbs.

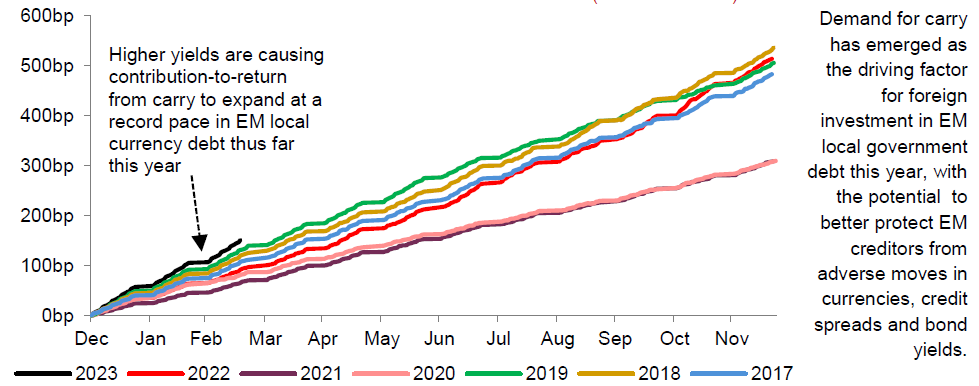

CHART OF THE WEEK: HIGHER CARRY CUSHIONS EM LOCAL BONDHOLDERS

EM LOCAL GOVERNMENT CARRY CONTRIBUTION-TO-RETURN (BASIS POINTS)