The start of EM rate cuts is being overshadowed by the sell-off in US rates

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

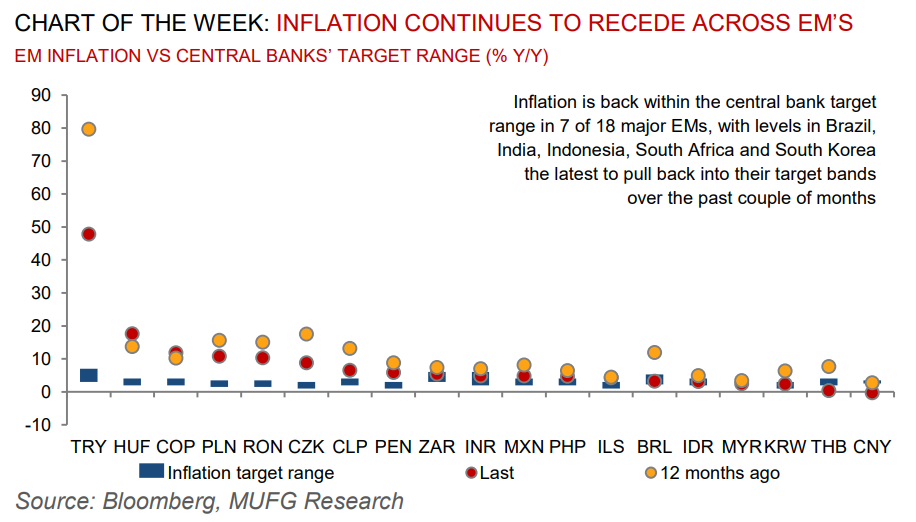

Markets have for some time priced a swift start to easing cycles in EMs, with a particular focus on LatAm, where ex-ante real rates are the highest, and inflation is coming off relatively quickly. At the end of July, Chile became the first major EM central bank to lower its official target rate, followed by Brazil (see here and here). While this is typically a good time for EM receivers, the bear steepening of the US curve is a headwind, at least for the backend of EM curves, and especially in countries where rate cuts are not imminent yet. Historical lessons of US late cycle bear steepening moves suggest that the current US bear steepening is already relatively extended, though curves were not as inverted in the past. As such, EM risks still abound.

FX views

While EM FX had been resilient to the initial rebound in the USD following the last US CPI print, this has been less true more recently with USD strength more concentrated against EM FX. Also, even if EM FX outperformed following last week’s CPI print, a considerable part of the rally faded as US rates moved higher post-reading. We believe this has likely been driven by a confluence of (i) concerns of faster-than-expected EM carry erosion, (ii) downside risks to the global growth outlook driven by a tepid China and (iii) upside risks to global inflation from higher commodity prices.

Week in review

Headline inflation in the Czech Republic fell in July, driven by base effects in food and energy inflation, but core inflation also fell. Meanwhile, headline inflation for July also declined in Hungary owing to lower food prices. Finally, headline inflation in Romania for July surprised to the downside but core came in sticky reflecting wage pressures resulting from Romania's tight labour markets.

Week ahead

In the week ahead, July inflation statistics will be released in Israel and the final print of Poland’s July inflation data will be released. Additionally, Q2 2023 GDP for Romania, Hungary, Poland and Israel are set to be released.

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to data from the IIF, July recorded the second largest monthly inflows into EM funds this year – EM funds received USD32.8bn from foreign investors – USD17.6bn into EM equities and USD15.2bn into EM bonds.