EM performance in 2024 and first glance into 2025

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

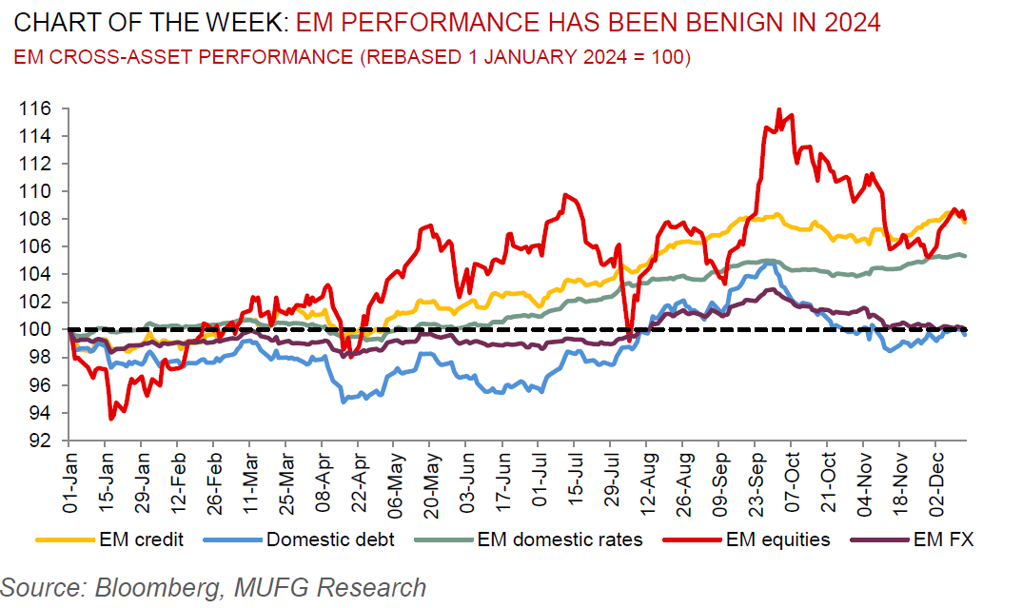

2024 has been a year dominated by a range of themes, with global and local factors capturing the markets’ attention along the way, including elections, the beginning of policy rate cuts in developed markets (DM), China stimulus, the carry trade unwind, recession concerns and geopolitics. Amidst this confluence of drivers, emerging markets (EM) have generally held up quite well, but with divergences across both asset classes and EM regions. Looking into 2025, we expect many of the largest EMs to slow, including all of the BRIC (Brazil, Russia, India and China) economies. However, we expect rebounds in a number of EMs that have undergone sharp macroeconomic adjustments and/or military conflict including Argentina, Egypt, Israel, Saudi Arabia and to a lesser extent the Central East European (CEE) economies. From a cross-asset perspective, we envisage equities – especially in more shielded from volatility economies – as best placed for 2025’s plethora of challenges, with EM FX to be pressured by tariffs and a strong US dollar.

FX views

Emerging market currencies have mostly weakened against the USD over the past week despite some renewed optimism over China stimulus. The USD has strengthened broadly over the past week even as the US rate market has moved to more fully price in another Fed rate cut this week after the release of softer inflation data (CPI and PPI) for November. Market expectations for a slower pace of Fed easing next year alongside the threat of US tariffs hikes being put in place continue to encourage a stronger USD. The Fed’s more cautious stance over further easing stands in contrast to the ECB who left the door wide open for further rate cuts next year at last week’s policy meeting. CZK and PLN strengthen vs. EUR as ECB plays catch up while CNB slows pace of easing.

Week in review

Inflation readings for November have been released across Egypt, Israel, Russia, Hungary, Czech Republic, Romania, and Poland. Heading into 2025, a rise in trade tariffs impacts both supply and demand, complicating the effects on inflation with much conditional on how these developments affect exchange rates. Separately, the UAE and Kuwait have announced that the countries will introduce a domestic minimum top-up tax of 15% from 2025.

Week ahead

This week, there will be MPC meetings in Hungary (MUFG and consensus: on hold at 6.50%), the Czech Republic (MUFG and consensus: on hold at 4.00%) and Russia (MUFG: +100bp to 22.00%; consensus: +200bp to 23.00%).

Forecasts at a glance

Growth across the EM universe is set to stabilise as domestic fundamentals offset external drags, with some rotation from the largest to smaller EMs. Inflation and interest rates are both “over the hump” – disinflation is progressing, and the decline in rates will continue and broaden for the remainder of 2024.

Core indicators

The latest monthly IIF flow data signalled that EM securities attracted USD19.2bn in November driven by a divergence between and equity and debt markets. The breakdown suggests that debts drove the inflows (USD30.4bn) whilst equities (USD-11.1bn) fell over the week.