IMF praises EMs amidst a cautious global outlook with rising debt levels a risk

Macro focus

The IMF’s latest bi-annual World Economic Outlook (WEO) released last week emphasised areas of caution for the global economy, with the attention on risks stemming from developed markets (DM) banking sector instability and sticky core inflation. For emerging markets (EM), the IMF was more upbeat, stating that sovereigns remain resilient with areas of growth outperformance, ebbing strains on commodity importers and fiscal reform momentum. Yet, as we catalogued last summer, rising debt servicing costs and refinancing risks leave the prospects for debt distress among speculative-grade issuers (see here). While more systemically important EMs are well insulated by healthier balance sheets, sizable reserve buffers and less overvalued currencies, in a cascade of EM credit events, the negative impact of the whole could be larger than the sum of the parts.

FX views

Emerging market currencies have regained upward momentum against the USD over the past week, continuing to benefit broadly from the ongoing weakening of the USD. The USD’s bearish momentum has been reinforced over the past week by economic data releases that have supported expectations for a sharper slowdown in both US growth and inflation. A further supportive factor for emerging market currencies this year has been the improving cyclical momentum for China’s economy. The release tomorrow of the latest GDP report for Q1 is expected to confirm that China’s economy started to bounce back strongly after the removal of COVID restrictions late last year.

Trading views

Our cautious stance on EM was a bit of an opportunity cost with falling US price pressures and better ex-US growth. This is helping set up an environment for carry trades, with bond volatility now back to the lows catching up to equity and FX. It is hard to go against complacency without a catalyst as these trends can go for much longer than one expects – wait for the catalyst to come, but in the meantime go with trends where rates are high, and/or CBs on your side. As for clear catalysts that would make us change our mind. There are several we could point to but ultimately they all lead to the same thing. That is an increase in implied vols. Another way of saying vol markets expecting (or being prepared to pay) for higher vol going forward.

Week in review

Saudi Arabia’s inflation rate edged lower by 0.3ppt to 2.7% y/y in March, with further downward pressure expected on higher base effects in food. Egypt’s inflation rate rose by 0.6ppt to 32.6% y/y in March on the EGP weakness and higher food prices. Bahrain returned to the market issuing a USD1bn 7 year sukuk and a USD1bn 12 year bond at 6.25% and 7.75%, respectively – the first market issuance since 2021. Russia’s headline inflation eased to 3.5% y/y in March from 11.0% y/y in February, on the back of strong base effects, mainly resulting from an exceptionally large jump in the CPI base following the post-invasion price shock in March. Finally, inflation rates in Czech Republic, Hungary and Romania all marked a slowdown in March.

Week ahead

In a thin week ahead, headline inflation in South Africa is set to ebb lower by 0.2ppts to 6.8% y/y in March – though core inflation continues to be a concern (set to rise by 0.2ppts to 5.4% y/y). Beyond EMs, US data should remain in focus in this week, though the calendar looks somewhat less busy compared to the previous week. Preliminary US PMIs on April 21 will likely be watched closely given some recent hard data softness, though we do expect some emphasis on initial jobless claims as well. China's data (Q1 2023 GDP, and March IP and retail sales) will likely be a more important driver of price action for EM assets over the coming week, to the extent that it suggests further widening between China's and the US growth outlooks.

Forecasts at a glance

Whilst EMs continue to grapple with much the same themes at the turn of the year, we view the outlook as a tale of two halves in 2023. A fading boost from reopenings, a global manufacturing cycle downturn and tighter financial conditions are lumpy headwinds that will weigh on EM prospects in the first half of 2023. However, China’s zero COVID policy exit, the eventual end of rate hikes and a US dollar peak, all offer significant tailwinds to the EM complex in the second half of 2023 (see here).

Core indicators

While the cycle is still positive, March witnessed retrenchment in EM capital flows, down to USD9.4bn, with investors beginning to take a more cautious approach to EM assets as an early year rally ebbs.

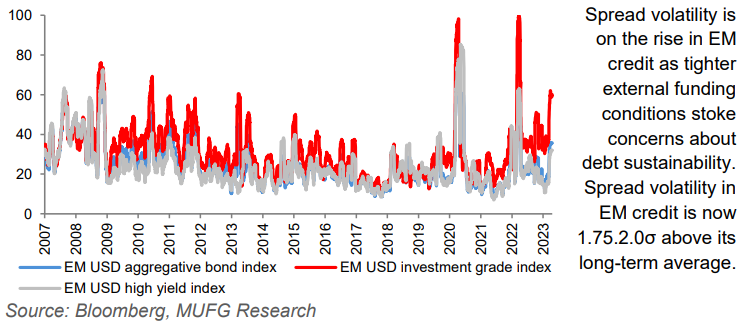

CHART OF THE WEEK: FUNDING RISK STOKES EM SPREAD VOLATILITY

EM CREDIT SPREAD VOLATILITY (30 DAY REALISED)