A window of calm for emerging markets

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

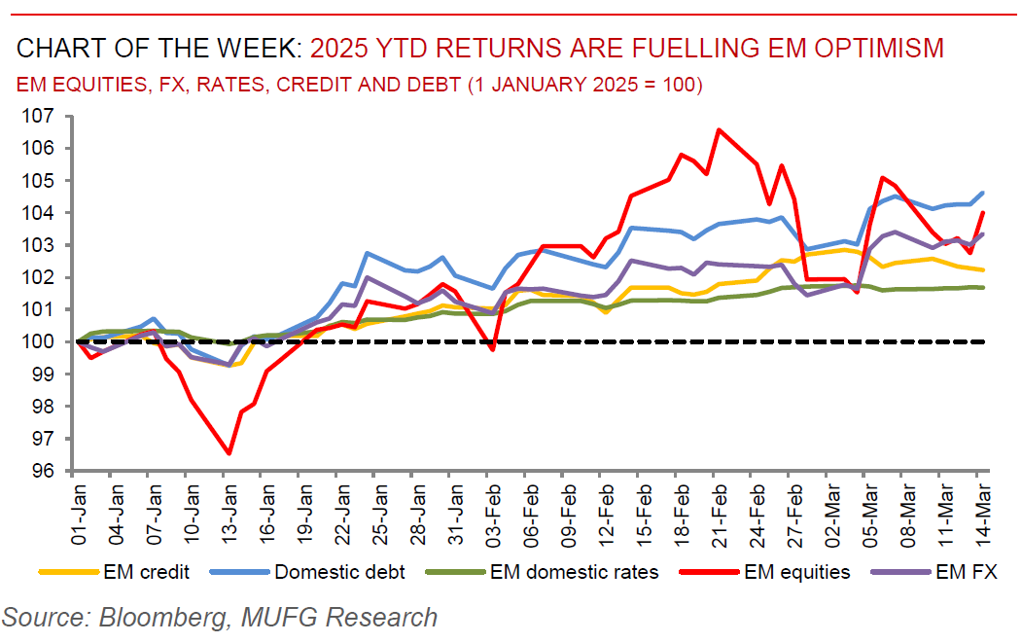

Notwithstanding the abundance of risks surrounding rising trade tensions and tectonic geopolitical shifts, emerging markets have largely taken this in stride. A window of calm is prevalent across emerging markets with every major cross-asset – EM credit, domestic debt, domestic rates, equities and FX – higher year-to-date. From one lens this is comprehensible, given how the recent rollercoaster of developments has led the market to look through the noise from many tariff headlines. Having said that, this setting does not sit contentedly and we are cautious to downplay US policy risks given the looming deadlines in the coming months. Tariffs as a negotiating strategy may merely be a small part of the narrative and instead, the US administration could lean towards being more hawkish on trade via implementation in coming months, especially if these become an critical component of the fiscal toolkit. Taken together, today’s window of calm across emerging markets may be turn out to be merely a false sense of security.

FX views

Emerging market currencies have continued to rebound against the USD at the start of this year, and they are currently on track for their best quarterly performance since Q4 2020 following the negative COVID shock. Stronger China growth and consumption plans provide support for LatAm FX, and USD/MXN drops back below 20.000 after Trump administration welcomes Mexico’s decision not to retaliate to US tariffs. The weaker USD and lower US yields are providing a tailwind for emerging market currencies. Building fears over slower US growth in response to heightened policy uncertainty and trade tariffs have hurt business and consumer confidence.

Week in review

S&P upgraded Saudi Arabia’s credit rating to A+ from A (stable outlook) for the first time in two years, citing “the institutional settings having strengthened in the context of socioeconomic reforms and transformation under Vision 2030 and are now in line with most peers rated in the A category”. According to press reports, a draft of the long-awaited Kuwaiti debt law has been approved by the Council of Ministers and is now pending sign-off by HRH Emir Sheikh Mishaal Al-Ahmad Al-Jaber Al-Sabah – this paves the way for sovereign debt issuance, and by implication a likely transformative project spending drive. The IMF board has approved the fourth review of Egypt’s Extended Fund Facility (EFF) programme with an immediate disbursement of USD1.2bn. The National Bank of Poland (NBP) kept its key policy rate unchanged at 5.75%, in line with our (and consensus) expectations. Finally, a host of inflation readings for February were released across Egypt, Hungary, Russia, Romania, Poland and Israel.

Week ahead

This week, there will be rates meetings in South Africa (MUFG and consensus: -25bps to 7.25%) and Russia (MUFG and consensus: on hold at 21.00%). There will be also be CPI data released in South Africa (MUFG: 3.3% y/y; consensus: 3.4% y/y).

Forecasts at a glance

The external backdrop for EM has shifted abruptly – the soft-landing pro-risk environment and pricing of non-recessionary Fed cuts has given way to concerns around tariff risks (and likely retaliatory action), higher-for-longer US rates and a strong US dollar. This sets the stage for a challenging EM backdrop in 2025. There are dimensions that could make Trump 2.0 less disruptive. Given the reduced direct trade exposure of the Chinese economy to the US and expectations that there will be a monetary and fiscal response by Chinese policymakers to offset the tariff growth shock, the economic and financial market disruptions will, on aggregate, be less severe than Trump 1.0.

Core indicators

The latest monthly IIF flow data signalled that EM securities attracted USD15.9bn in February 2025 driven by USD18.1bn into debt markets, while equities faced USD2.1bn in outflows.