To read the full report, please download the PDF above.

Implications of rising oil prices for emerging markets – winners and laggards

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

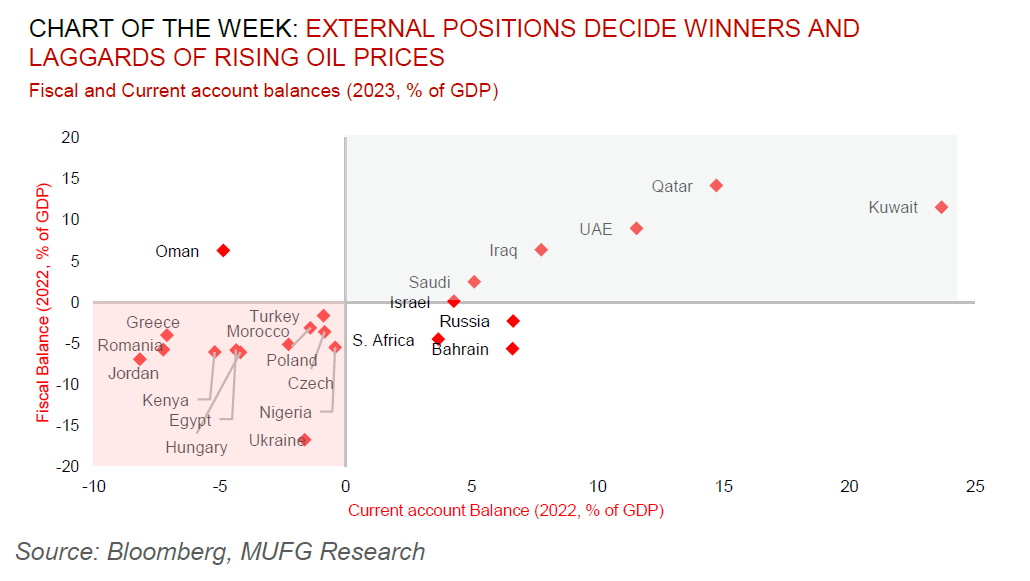

Oil prices have become an important differentiator of EM performance as they stand close to 30% higher since the end of June. There are ample moving parts to know where oil prices will go from here, but as we have recently catalogued, whilst tight fundamentals suggest that the gravitational tilt for prices are to the upside, we maintain our year-end 2023 and 2024 Brent crude target of USD84/b and USD87/b, respectively, with a surge back north of USD100/b – albeit within striking distance – not our base case scenario (see here and here). From an EM perspective, the winners are recognisable – major net oil exporters (GCC region, Colombia, Malaysia Nigeria and Russia) – with higher energy prices boosting the terms of trade, improve balance of payments positions and give a lift to lift to floating exchange rates where they are present. On the flipside, many major EMs are net importers of fuel (CEE region and most of EM Asia) stand to lose from higher oil prices, through a deterioration in external account positions, driving-up production costs for manufacturers and dampening demand by squeezing real incomes through higher inflation.

FX views

It has been a mixed week for EM FX. LatAm and Asian currencies have outperformed supported by an easing of investor pessimism over the outlook for China’s economy and stronger pushback from Chinese policymakers against CNY weakness. Retail sales (+4.6%Y/Y) and industrial production (+4.5%) both picked up in August although weakness in fixed asset investment (+3.2% YTD y/y) and property investment (+-8.8% YTD y/y) continued. It provided the first tentative signs that policy stimulus is beginning to help stabilise growth in China. However, the scale of the improvement has not yet been significant enough to trigger a bigger reversal of the recent weakening trends for China related currencies. USD/CNY has dropped back below the 7.3 level after strong pushback from domestic policymakers as well.

Trading views

We feel the move by ECB last week is a good signal to start entering EM trades but against Euro (and GBP) rather than USD. We feel enough conviction that the peak in rates is starting to come through and we may have a sweet spot for EM where we can still talk about soft landing alongside peak rates. This may not last too long especially if the data starts falling too quickly but for now a window exists. This is buffeted by the growing belief that the picture in China is not as negative as the sentiment surrounding the country. This argument is made on both fronts, not necessarily that the data is improving but just it is much better than the excessive pessimism that exists with regards China. The big risk to this is the rising yields especially in the US.

Week in review

Russia raised its key interest rate by 100bps to 13.00%, in a bid to contain inflation and the Russian Rouble’s (RUB) slide. Romania’s August inflation remained the same as previous month on a y/y basis at 9.4%. Israeli inflation rose by a robust 0.8ppts to 4.1% y/y led by base effects in fuel.

Week ahead

In the week ahead, we have a rates meetings in Turkey (MUFG: 31.00%; consensus: 30.00%), Egypt (MUFG and consensus on hold at 19.25%), and South Africa (MUFG and consensus on hold at 8.25%). Meanwhile, August’s inflation data will be released in South Africa (MUFG and consensus: 4.8% y/y). Beyond EMs, it’s a busy week for rate decisions in DMs, with eyes on the Fed, Bank of Japan and Bank of England.

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to data from the IIF, foreign institutional investors sold USD15.5bn worth of EM assets in August 2023 – the largest amount in 2023 – led by outflows around Chinese equities, accentuating the country’s economic challenges, amid scepticism over sluggish measures to stem the economic slowdown.