Assessing EM performance in the second half of 2023 – macro optimism, micro trepidations

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

The macro developments across the EM space over the last couple of years has offered a number of optimistic themes, stemming from (i) early hikes ahead of the Fed (see here); (ii) rising EM growth differentials (see here); and (iii) a growing independence from Chinese economic cycles (see here). Such optimism should offer the robust tailwinds for EM assets to outperform. Yet, EM asset performance remains unambiguously weak relative to DMs. It is the micro that continues to concern. A major dimension of the “EM vs DM” theme is the issue surrounding corporate competition. Recent trade data unmasks this well with EM corporates facing an uphill challenge in competing against DM multinationals. On net, whilst the EM macro leans towards the global backdrop being more hospitable today after a peak in inflation and rapidly approaching cutting cycles, the micro notion of corporate competition will continue to present headwinds.

FX views

Emerging market currencies have continued to rebound against the USD over the past week as they extend their advance further above the lows from the end of last month. The USD has lost upward momentum as the Fed first signalled and then left rates on hold last week – the first time the Fed has not raised rates at an FOMC meeting since the current tightening cycle began in March of last year. The slower pace of hikes highlights that the Fed is becoming more cautious over the need for further hikes and wants more time to assess incoming data.

Trading views

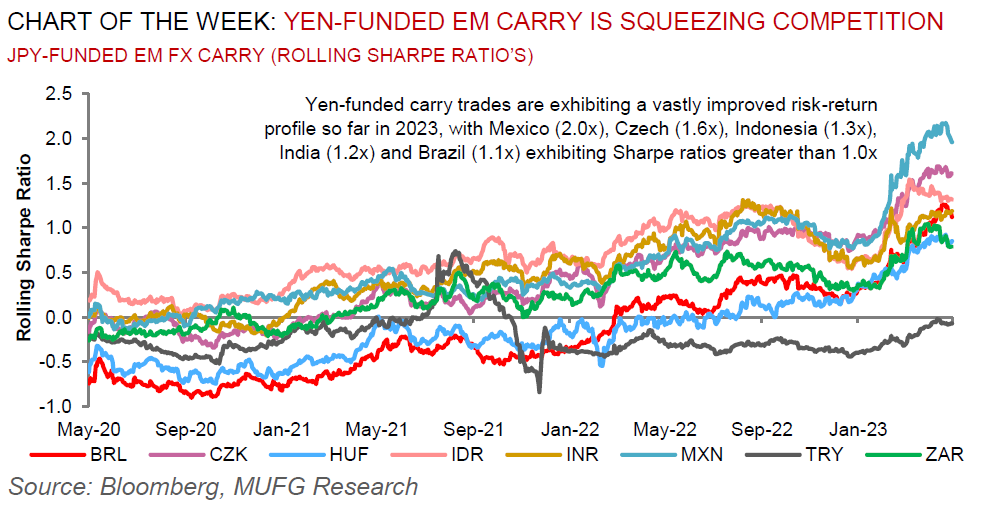

Risk premium has shifted slightly in the last week but overall the big picture or trend has not changed significantly. The moves by China on rate cuts as well as a lot of talk on further stimulus measures has seen some two-way risk enter the well populated long USD/CNH trade as witnessed by the large outside reversal price action during last week. EMFX carry trade continues to do well and with VIX making fresh multi-year lows, it is hard to go the other way as much as risk bears like searching for narratives. Granted, investors may state that selling risk when VIX is down here is a good strategy but reality is that many of those same investors have been looking at reasons to sell risk for the most part of the year.

Week in review

The May headline inflation for Czech Republic, Israel, Poland, as well as Romania slowed, all on base effects and lower sequential price growth in the region in May, with the energy-related components likely registering the largest contributions to these declines whilst core inflation also slowed down on our estimates. These readings will easing the pressure on central banks to hike further, while equally raising hopes for a dovish tilt.

Week ahead

It is an important week for central bank decisions in EM EMEA, with rates meetings in Hungary (MUFG and consensus on hold at 13.00%), the Czech Republic (MUFG and consensus on hold at 7.00%), Turkey (MUFG and consensus hike by 11.50% to 20.00%) and Egypt (MUFG and consensus on hold at 18.25%). In addition, inflation data for May will be released in South Africa (MUFG 6.3% y/y; consensus 6.5% y/y).

Forecasts at a glance

Whilst EMs continue to grapple with much the same themes at the turn of the year, we view the outlook as a tale of two halves in 2023. A fading boost from reopenings, a global manufacturing cycle downturn and tighter financial conditions are lumpy headwinds that will weigh on EM prospects in the first half of 2023. However, China’s zero COVID policy exit, the eventual end of rate hikes and a US dollar peak, all offer significant tailwinds to the EM complex in the second half of 2023 (see here).

Core indicators

According to IIF data, weekly inflows to EM assets totalled USD1.6bn in the week ended 16-Jun – USD1.1bn in form of equities and USD0.5bn in form of debt.