BRICS summit preview – will a "BRICS+" bloc accelerate de-dollarisation?

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

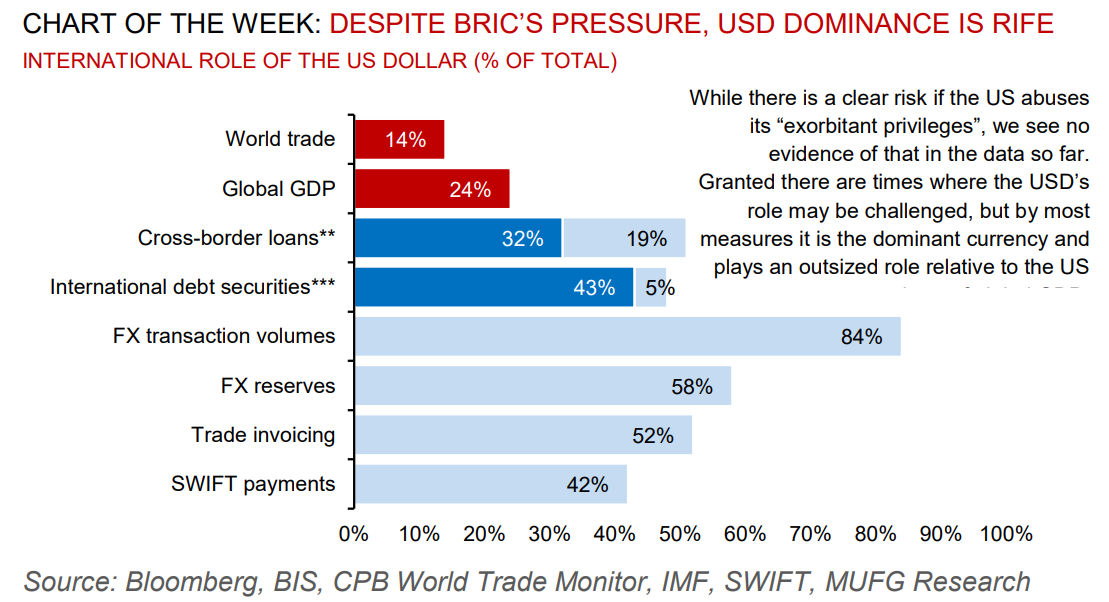

The BRICS grouping of major emerging markets – Brazil, Russia, India, China and South Africa – is holding its fifteenth summit between 22-24 August. The top of the summit’s agenda will be anchored on (i) an expansion of the blocs members (23 countries are interested in joining according to South African officials); (ii) greater use of local currencies to settle trade between each other; and (iii) prospects of a BRICS currency which may have the potential to challenge the dominance of the US dollar. Whilst any “BRICS+” grouping could bring into question the speed and scale with which member countries adopt commercial and financial systems outside of the US dollars domain, we hold conviction in our previous examination that being fed up with the US dollars dominance is old hat, and it will remain the world’s currency of first resort, in our view (see here).

FX views

Emerging market currencies have continued to weaken against the USD over the past week. It has resulted in our MUFG EM FX index giving back all of the year to date gains against the USD. There have been two main drivers of the recent sell-off for emerging market currencies. Firstly, market participants are becoming more concerned over the economic slowdown in China. The second driver of emerging market currency weakness has been the recent adjustment higher in US yields at the long-end of the curve that has helped to encourage a stronger USD.

Week in review

The People’s Bank of China (PBoC) cut the 1-year LPR (loan prime rate) by 10bp to 3.45% and left 5-year LPR unchanged at 4.20% on 21 August, which was below market expectations of 15bp cuts to both 1-year and 5-year LPR following the 15bp MLF rate cut on 15 August. The Bank of Russia announced an unscheduled key rate meeting on 14 August and hiked its key rate by 350bp to 12% – it refrained from including the phrase “the Bank of Russia holds open the prospect of a further increase at its next meeting" as in previous statements, signalling that last week’s outsized hike is at least partially front-loading the hiking cycle that we (and consensus) had expected. Finally, Q2 GDP growth was mixed across the CEE4, with Czech Republic and Romania recorded sequential increases, whilst Poland and Hungary recorded sequential decreases.

Week ahead

In the week ahead, a rates meeting is scheduled in Turkey on Thursday – where we expect the CBRT to raise its repo rate by 250bp to 20.0% (consensus 20.0%). Also, headline and core CPI will be released in South Africa – we expect a decline in in the former to 5.1% y/y (consensus 5.1% y/y) and a flat reader in the latter at 5.0% y/y (consensus 4.9% y/y).

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to data from the IIF, EM funds recorded three straight weekly net outflows with an outflow of USD7.1bn in the latest week, led by equities (USD6.6bn), with the outflows from Chinese equity funds hitting a record USD4.0bn.