To read the full report, please download the PDF above.

Stagflationary pressures in Israel warrants a cautious policy stance

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

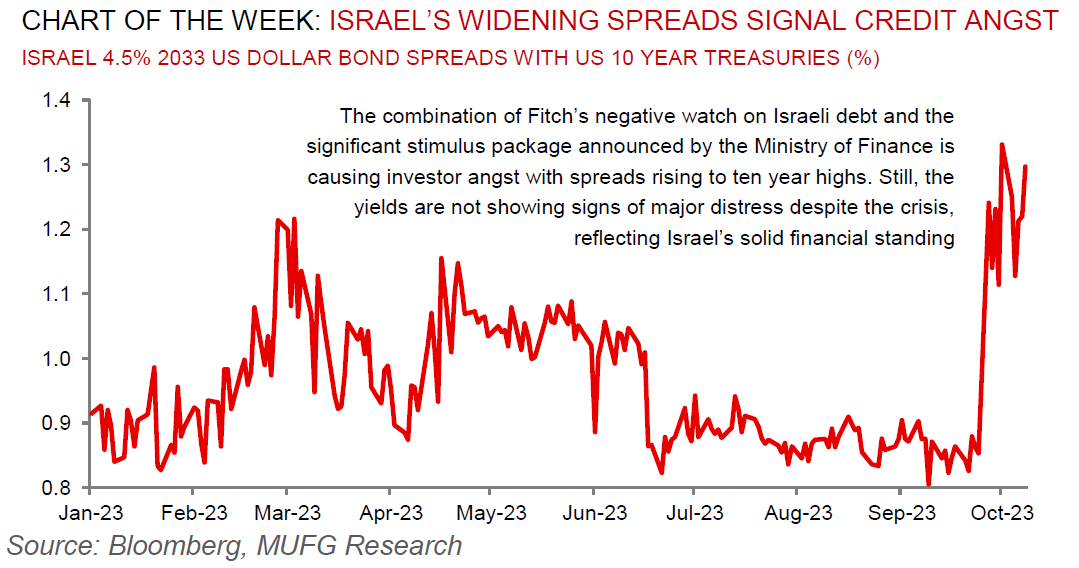

With the Israeli – Hamas conflict entering its third week, our conviction holds that we are considering this as a stagflationary shock to the Israeli economy – a deteriorating growth outlook, juxtaposed against elevated inflation pressures stemming from rising fiscal expenditures as well as weaker currency passthrough effects. In line with our (and consensus) forecasts, the Bank of Israel (BoI) kept rates unchanged at 4.75% today, in a bid to contain risks and the backdrop of significant Shekel weakness. While we view that financial stability risks and economic vulnerabilities are lower than during previous episodes of escalating geopolitical tensions – owing to Israel’s stronger balance of payment position, large stock of FX reserves and anticipated overseas inflows – we nevertheless believe the BoI will maintain a cautious policy stance. Thus, while the market has been pricing in rates cuts for the forthcoming meetings, we expect the BoI to only begin rate cuts by Q1 2024 to support the recovery. At the current juncture, the likely strategy to offer economic support is likely to be channelled via fiscal policy (not monetary policy) that will work with shorter lags.

FX views

It has long been said that “Swissy never lies”. When the Swiss Franc (CHF) is appreciating, it is generally a sign of market angst, and it tends to be a reliable indicator of safe-haven flows. These characteristics have already been on display in the weeks since the escalation of conflict in the Middle East, and we expect his to continue to be a dependable gauge of market sentiment and an effective hedge in the case of further escalation. Overall, notwithstanding the burgeoning geopolitical risks facing currency markets, EM FX continues to struggle amid a plethora of uncertainties notably around China being stuck in a low gear. Some have proven more resilient in the face of a strong US dollar over the past couple of months – most of LatAm FX still stands out, even if the tailwinds are not what they used to be.

Trading views

The price action in overall DXY and EM FX is a lot more disappointing for USD bulls than bears. The data continues to be strong in the US, yields made fresh highs, geopolitical risks and oil remain high yet overall EM trades well. Likes of high yield pairs like HUF, ZAR and BRL and all enjoying solid gains since the strong NFP print this month. The one outlier is MXN which is trading more in line with historical correlations to US yields and really struggling to rally meaningfully even with higher oil. Overall with little data to guide Fed pricing much until the latter part of the week and a fed blackout, we feel EM FX recovery could continue for a few days depending how geopolitical risk escalates. This is particularly concerning if ground troops enter as risk premiums will undoubtedly go up. For us oil making new high will be the key barometer.

Week in review

September inflation accelerated in Nigeria and South Africa. Meanwhile, Egypt was downgraded by S&P by one notch to "B-" and Moody's and Fitch Ratings have placed Israel's ratings on review for downgrade.

Week ahead

This week is an important one for central banks across the EM complex, and we expect it to be marked by significant rate divergence. There will be rates meetings in Israel (see macro focus section), Hungary (MUFG -75bp to 12.25%; consensus -50bp to 12.50%), Russia (MUFG and consensus +100bp to 14.00%) and Turkey (MUFG and consensus +500bp to 35.00%).

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to the IIF data, EM securities suffered an outflow of USD13.8bn in September 2023 – second consecutive month of overall outflows across the EM complex. Recent market turmoil around the future path of monetary policy, along the increasing sovereign yields have made a dent on the performance of non-resident outflows across the EM complex. Chinese equities have continued to suffer an outflow, totalling around USD4.4bn in September.