To read the full report, please download the PDF above.

Rocky start to 2024 for EMs but prospects remain hopeful

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

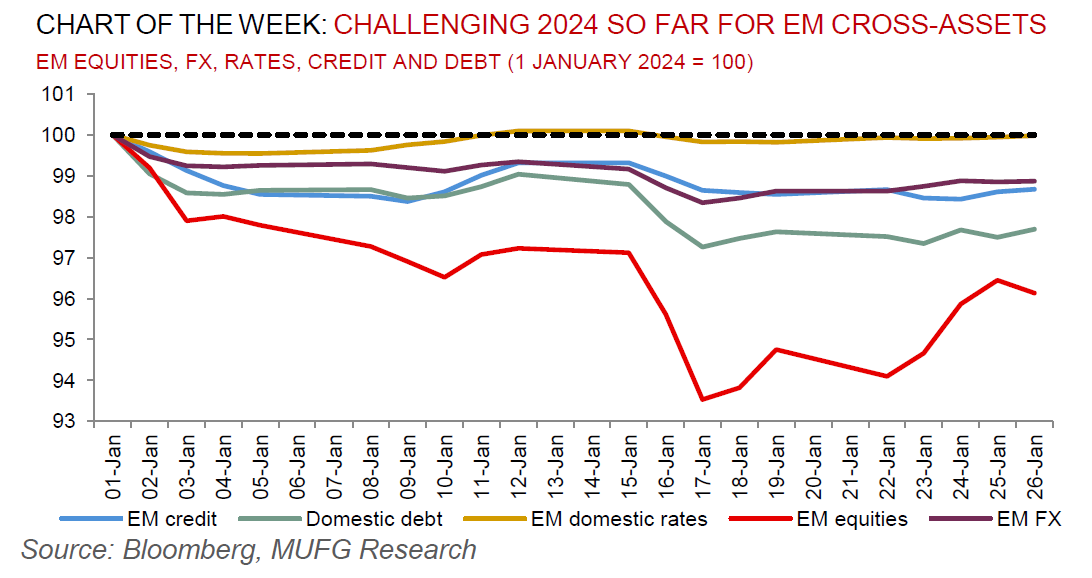

The safety cushion of an upcoming Fed easing – which acted as a powerful trigger for the search of global duration late last year – has ceased to exert a significant downward pressure on global yields. Whilst there are many factors behind this, the commonality remains that US economic resilience continues to filter through global markets. This has challenged EM cross-asset returns in January. Yet, after two years of battling what could be called a “great inflation” threat, the squeeze from tight financial conditions is easing, the lower global cost of funding is promising and the prospects of a coveted Fed pivot have brightened. This, in itself, is suffice in our view to remain hopeful about EM prospects in 2024 and anticipate another positive year in terms of EM cross-asset returns (see here).

Trading views

Last week, while equities and other risk assets performed well, for EMFX it was a case of short term volatility but like before mean reversion coming back quickly. We feel this week could be different with the Fed giving guidance over how likely March looks for the first cut. If we can end the week with March Fed cut pricing at 75% we think that is going to be quite a bullish signal.

Week in review

Moody’s upgraded Qatar’s credit rating to Aa2 while South Africa’s inflation surprised to the downside. Meanwhile, policy rate was left on hold in South Africa at 8.25% ,while in Turkey, CBRT raised interest rates by 250bps to 45.00%.

Week ahead

EM interest rate decisions are expected from Hungary (MUFG and consensus: 100bp rate cut to 9.75%) and Egypt (MUFG and consensus: on hold at 18.75%). Annual GDP for 2023 is expected in Poland at 0.5% y/y.

Forecasts at a glance

Growth across the EM universe is set to stabilise as domestic fundamentals offset external drags, with some rotation from the largest to smaller EMs. Inflation and interest rates are both “over the hump” – disinflation is progressing, and the decline in rates will continue and broaden in 2024 (see here).

Core indicators

EM funds saw net weekly outflows worth USD0.3bn in the week ended January 19 – equities and bonds at US0.2bn and USD0.1bn, respectively.