To read the full report, please download the PDF above.

How much space do EM central banks have to cut rates?

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

LEE HARDMAN

Senior Currency Analyst

Global Markets Research

Global Markets Division for EMEA

T: +44(0)20 577 1968

E: lee.hardman@uk.mufg.jp

PAUL FAWDRY

Head of Emerging Markets FX Desk

Emerging Markets Trading Desk

T: +44(0)20 577 1804

E: paul.fawdry@uk.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Macro focus

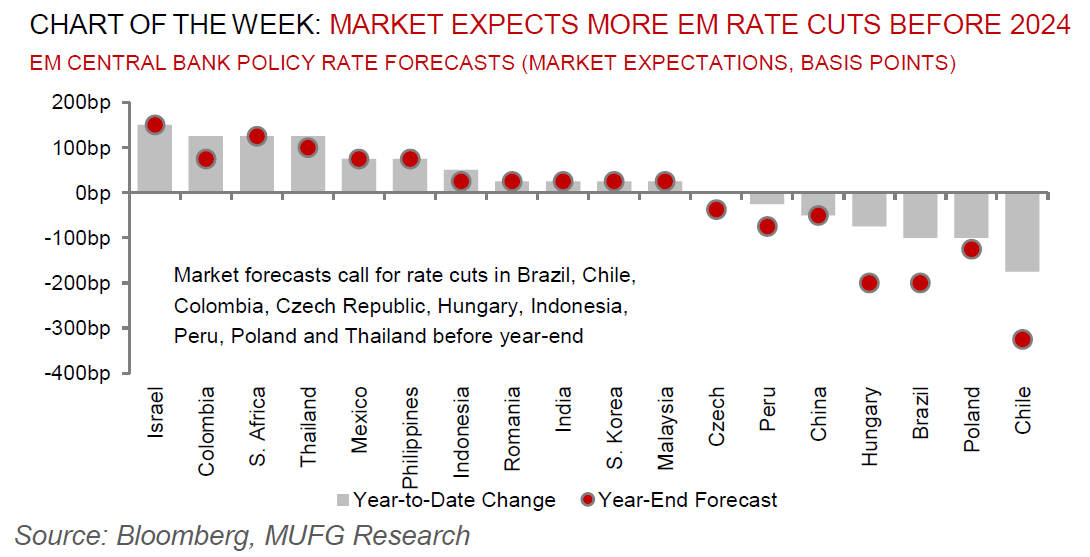

Major emerging markets have shown remarkable resilience thanks to early and significant monetary policy tightening and a favourable external backdrop for commodity producers. However, there are some differences between investment grade (IG) countries, which have been quite resilient versus high yielding (HY) countries, which have been stressed and frontier markets, where some countries have lost access to markets completely. Going forward, despite EMs kicking-off with bold rate cuts back in July (see here and here), two factors are now curbing optimism about the speed of EM easing. First, a tightening in global financial market conditions – higher-for-longer DM policy rates and US 10-year yields – along with a resurgent US dollar have accelerated EM capital outflows. Second, the rebound in oil prices – along with a jump in food prices for some – has stalled EM headline disinflation. The reaction of EM asset prices to these pressures has been surprisingly modest so far; since July, market pricing of EM policy rates has risen 30bp less than for the US, EM FX has weakened 5% and EM credit spreads have seen limited widening. On net, tighter global financial conditions and higher commodity prices suggest EM caution – not hawkishness.

FX views

The broad US dollar (DXY) index has been broadly unchanged over the last month despite re-accelerating and mostly divergent data. From an EM FX perspective, as EM central banks respond to a more erratic medium-term CPI profile and EM currencies lose some of their appreciation momentum, policymakers appear to be becoming more aware of the potential effect of further local currency depreciation on the CPI path.

Week in review

Last week, Hungary eased policy rate by 75bps to 12.25%; while Russia hiked by 200bps to reach 15.00%, in a bid to curb the currently elevated levels of inflationary pressures and bolster a weak RUB. Turkey hiked by 500bp to 35.00%, adding to a cumulative 2,150bps of rate increases since the central bank policy-flip that followed May’s elections.

Week ahead

This week will see South Africa publish its mid-term budget plan on 1 November. Rate meetings will be held in Egypt (MUFG: 100bp to 20.25%; consensus: on hold) and the Czech Republic (MUFG and consensus: on hold at 7.00%). Inflation data for October will be released in Poland and Turkey. GDP for Q3 2023 will be released in the Czech Republic. Finally, PMIs from various EM EMEA economies will be released throughout the week.

Forecasts at a glance

In a world of tightening global financial conditions and questions about the liquidity implications of the now-finalised US debt ceiling, we see a degree of macro risks for EM economies in H2 2023, with external funding requirements the central concern. We expect EM growth to trough this year but remain below potential in the 2024 recovery. The silver lining is that subdued growth should cap inflation, facilitating monetary policy easing where external balances allow.

Core indicators

According to the IIF data, in the week ending 27 October, EM funds recorded the thirteenth consecutive week of net outflows (USD5.6bn).