- The BoE remains deeply divided over the persistence of inflationary pressures. Various comments at the last meeting seemed to open the door to easing but the data flow has been mixed since then and there has been no attempt from officials to lay more groundwork in public for a move. We still lean towards a cut next week, just about, but it’s a close call. Any reduction in rates would likely come with hawkish guidance in what would likely be a gradual and cautious start to the easing cycle.

- Survey data this week reinforced the sense that the euro area expansion has lost steam in recent months. It’s clear that the German industrial sector continues to act as a brake on overall activity. However, recovering household real incomes will provide support and our base case is that the euro area recovery will continue, albeit at a muted pace.

BoE preview – A deeply divided MPC

We are sticking with view that there will be a cut at next week’s meeting, but it’s a close call. Last time out, in June, it was noted that the decision to remain on hold was “finely balanced”, and that remains the case. We’d expect a cut, if indeed there is one, to be a hawkish one with an emphasis that policy will remain restrictive (while a hold would probably be dovish with some more guidance that easing is on its way).

After the messaging in June we thought that BoE officials might use speeches after the election blackout period to further tee up an initial move – but the opposite has been true. Particularly notable was an intervention from Huw Pill, the BoE’s chief economist, who highlighted that there are “upside risks” to his assessment of inflation persistence. In the room Pill also talked about the economy’s “speed limit” several times, suggesting that there may be some concern around inflationary pressures generated by the UK economy’s upshift since the start of the year.

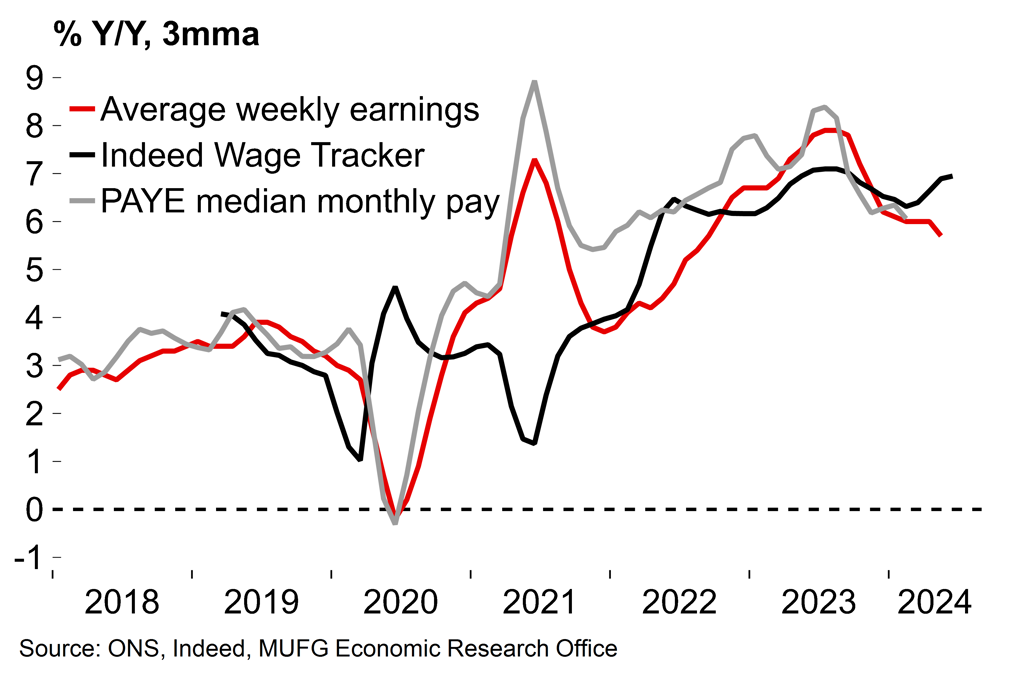

In terms of data, there haven’t been any significant shocks since the last meeting, but on balance there’s been more ammunition for the hawks. While headline inflation remained at 2% in June, bang on target, the core and services components did not budge either (remaining at 3.5% and 5.7% respectively). Pay growth edged down a little, but progress is slow and, at 5%+, it is still far from being consistent with the inflation target. The headline inflation rate remains on course to rise again later in the year as declines in energy costs slip out of the calculation, while the latest PMI survey highlighted that global shipping disruption linked to the Red Sea crisis is pushing up manufacturing input costs.

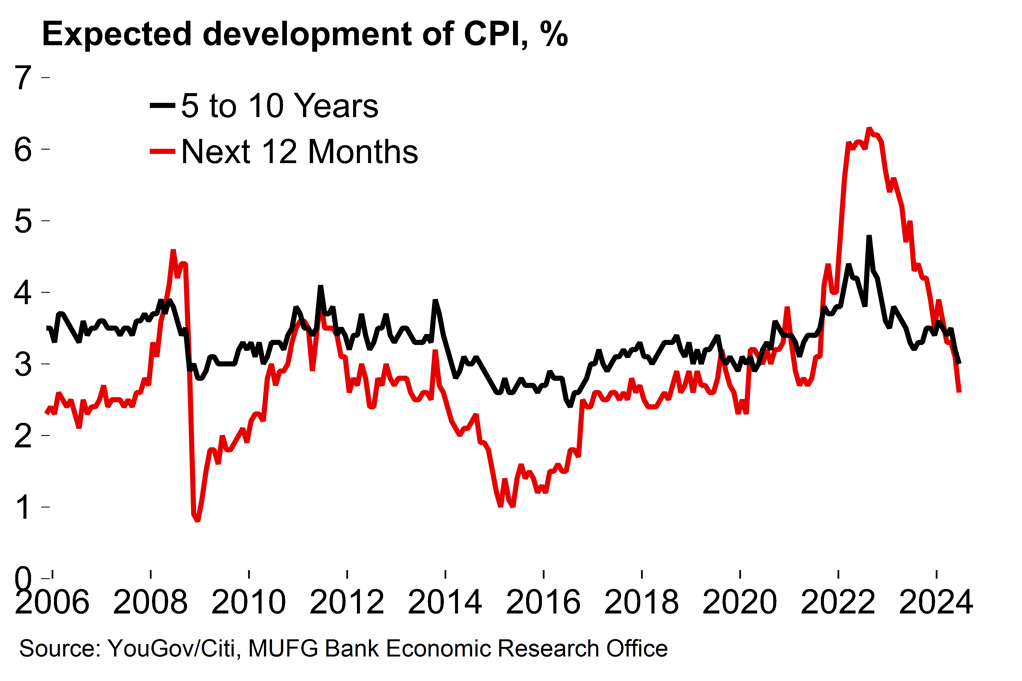

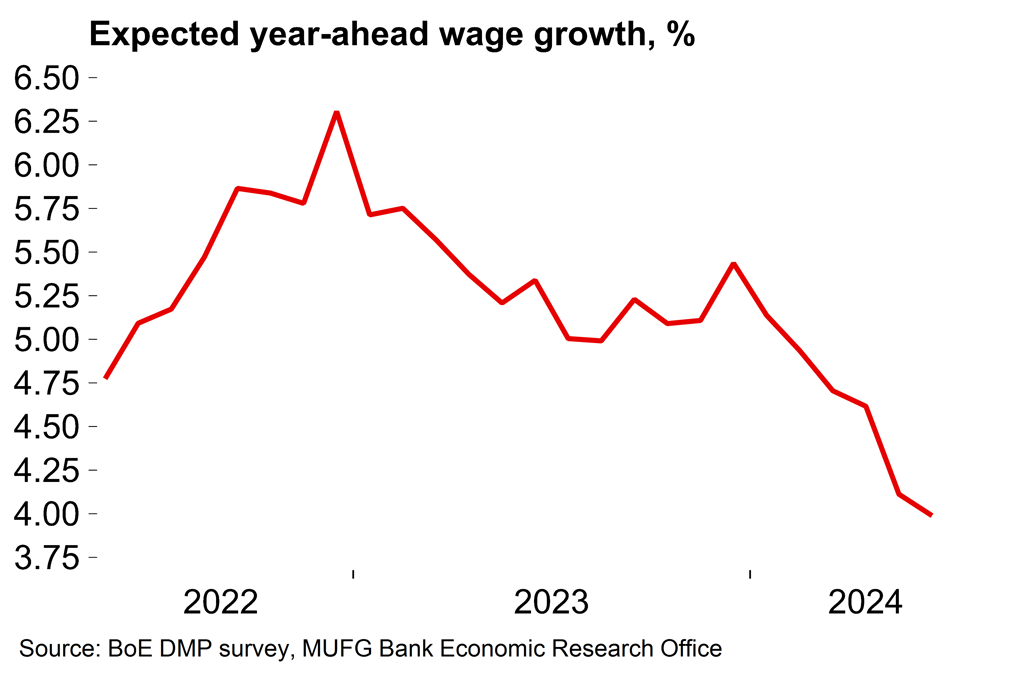

But we don’t believe there’s been any reason to declare that the underlying, domestic disinflationary process has come to a halt. The (small) upside surprise on inflation was largely driven by the volatile hotel component. The PPI services gauge continued to ease in Q2, pointing to lower pipeline pressures, in line with the trends from survey indicators. On high nominal pay growth, this likely still reflects the catch-up process after the loss of purchasing power during the inflationary shock – surveys point to slowing nominal pay growth and inflation expectations remain well-anchored. Stronger sterling is also supportive of lower price pressures ahead.

On the growth backdrop, the UK economy is certainly ticking along nicely. But we think the headline growth figures in H1 will have been temporarily boosted by the fading impact of public sector strike action. It’s also clear now that consumers are reacting to better real income conditions by increasing savings: the household saving ratio risen steadily over recent quarters to 11.3% in Q1 (2019 average: 5.5%). Yes, that could mean upside risks to growth further down the line if it’s reversed, but for now surveys suggest that this trend will continue, limiting demand pressures. We also expect tax rises will be announced in the autumn as the new government looks to expand its fiscal leeway.

Chart 1: The services component remains sticky

Chart 2: Nominal pay growth is uncomfortably high

A data-dependent BoE could go either way, but we still feel that there is a something of an easing bias overall. Policymakers could easily have sat on their hands ahead of the election this month given political sensitivities but instead chose to open the door wider to a cut with changes to the statement language and minutes. That felt significant. Perhaps there is a sense that it’s better to get ahead of the curve and then take stock rather than playing catch-up later. The dovish shift in US rates expectations over recent weeks (a Fed cut in September is now fully priced in) may also provide encouragement to some officials to start things moving on this side of the Atlantic.

Whatever happens next week, the BoE is still edging closer to easing policy – Pill acknowledged that it’s a question of “when rather than if” – but the MPC is clearly very divided on the persistence of underlying inflationary pressures. If there is a cut next week, it may well come with a 5-4 vote split (and without the backing of the BoE’s chief economist), while the degree of division points to a gradual and cautious start to the rate cut cycle.

Chart 3: Nothing to worry about when it comes to inflation expectations

Chart 4: The DMP survey suggests wage pressures are easing

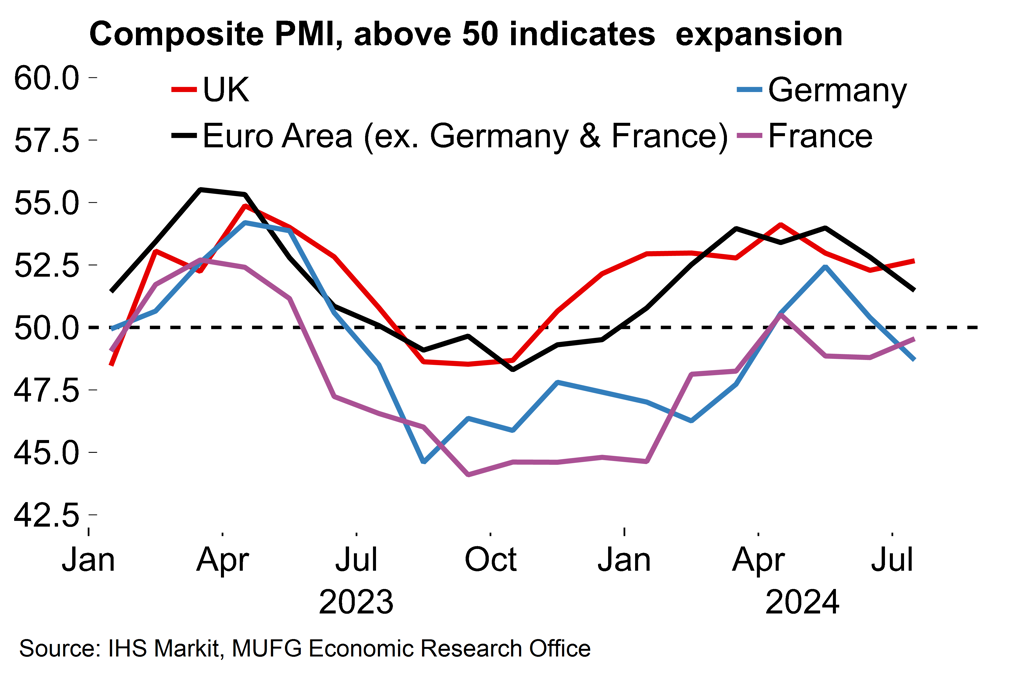

July’s PMIs suggest that the euro area recovery is losing steam

Survey data this week highlighted that the euro area recovery remains fragile. The flash composite euro area PMI slipped from 50.9 to 50.1 in July, a 5-month low, indicating stagnation. We are tracking Q2 GDP at 0.2% Q/Q (the first estimate will be released next week) which would be a slowdown from 0.3% at the start of the year. It’s still early days but these July PMI numbers suggest that the euro area economy would do well to eke anything better than 0.2% in Q3. This means that risks are tilted to the downside around our current forecast for annual average growth of 0.7% in 2024 (and the ECB’s June projection for 0.9% certainly looks optimistic).

Weakness is mostly driven by the manufacturing sector – and that of Germany in particular. The German economy continues to act as a brake on activity in the euro area as a whole and there is little indication of any reversal in fortunes. This week also saw the reliable German ifo survey surprise to the downside with a further decline in the expectations gauge. German industry is plagued by a range of long-term structural issues which include comparatively higher energy costs, shortages of skilled workers and increased competition for auto exports from China. Over the short-term, concerns about future US tariffs are likely also weighing on sentiment, as well as policy uncertainty in France.

However, at 51.9, the latest PMIs suggests that the euro area services sector remains in reasonable shape and we believe that the ongoing recovery in real incomes will provide a floor to overall growth going forward. Indeed, German consumer confidence showed a healthy bounce this week. We’d also note that there may also be some residual seasonality in the services PMI numbers which have followed a similar pattern for three years now with a strong start to the year before the numbers tail off. Our base case is that the euro area recovery will continue, but it will be a middling recovery.

Chart 5: Signs of fading euro area growth momentum

Chart 6: Is there some residual seasonality in the PMI?

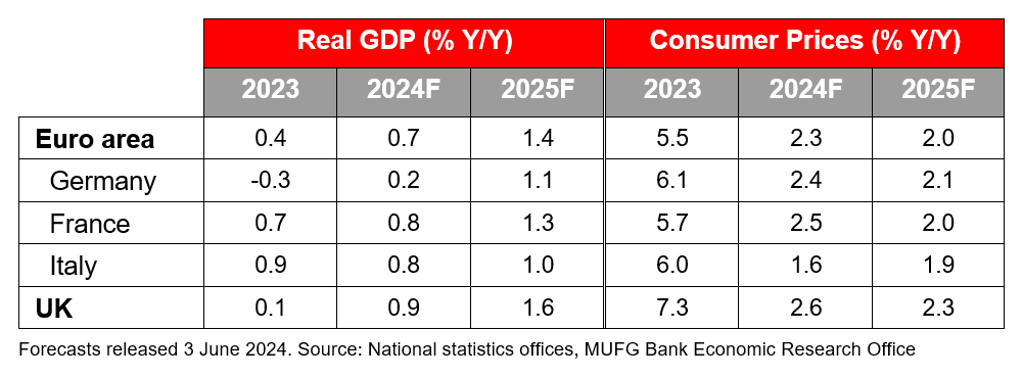

MUFG European Macro Outlook: Key points

- The euro area economy expanded by 0.3% Q/Q in the first quarter of the year, with all the major national economies growing at a faster-than-expected rate. The UK economy started the year strongly (0.7% Q/Q). While we look for slower growth rates in Q2, the recent uptick in momentum may well mark an inflection point after an extended period of stagnation. Broader growth conditions are set to continue to improve over coming months as real incomes recover and central banks start to ease policy.

- Nevertheless, it’s likely to be a case of moderate recovery this year rather than a rapid rebound. Business surveys have reinforced that message. The ECB followed through with its well-signposted cut in June, but the relatively hawkish tone suggested that policymakers remain wary about the inflation outlook. Monetary policy is set to remain in restrictive territory for some time. Meanwhile, many governments will need to make fiscal consolidation efforts after expansive spending in recent years, and structural pressures are set to continue to weigh on European manufacturing. For these reasons we do not see growth sustainably exceeding potential this year or next. We expect average growth of 1.4% in the euro area in 2025 and 1.6% in the UK.

- Despite small recent upside surprises in monthly inflation figures we expect that the disinflation process will reassert itself in H2 this year. Forward-looking survey indicators point to easing price pressures, household inflation expectations are well-anchored and there are mounting signs of increased slack in labour markets. We expect annual average euro area headline inflation will ease from 2.3% in 2024 to 2.0% next year. We expect a similar path in the UK, albeit with rates remaining slightly higher (2.3% in 2024).