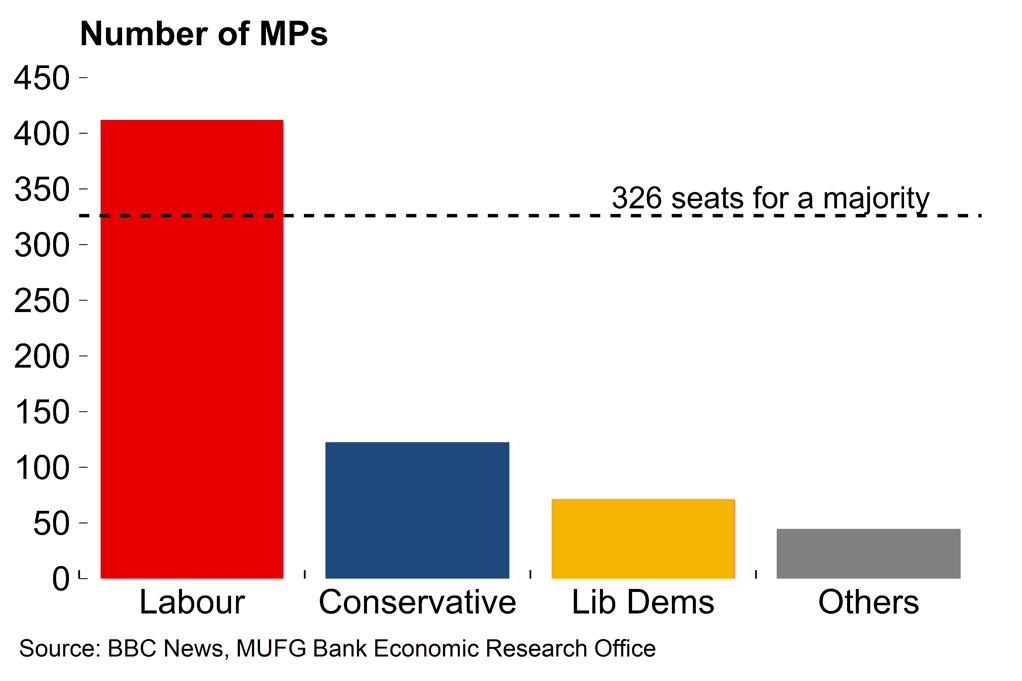

- The Labour party won a landslide majority at yesterday’s UK election. This was expected and market reaction was minimal. Any radical policy shift is unlikely based on the party’s current proposals, which centre on some growth-friendly tweaks to planning reform and modest capex expenditure. To our minds, the most significant change is that a new government with a sizeable majority heralds a return to relative calm and stability after the turbulence of the Brexit years.

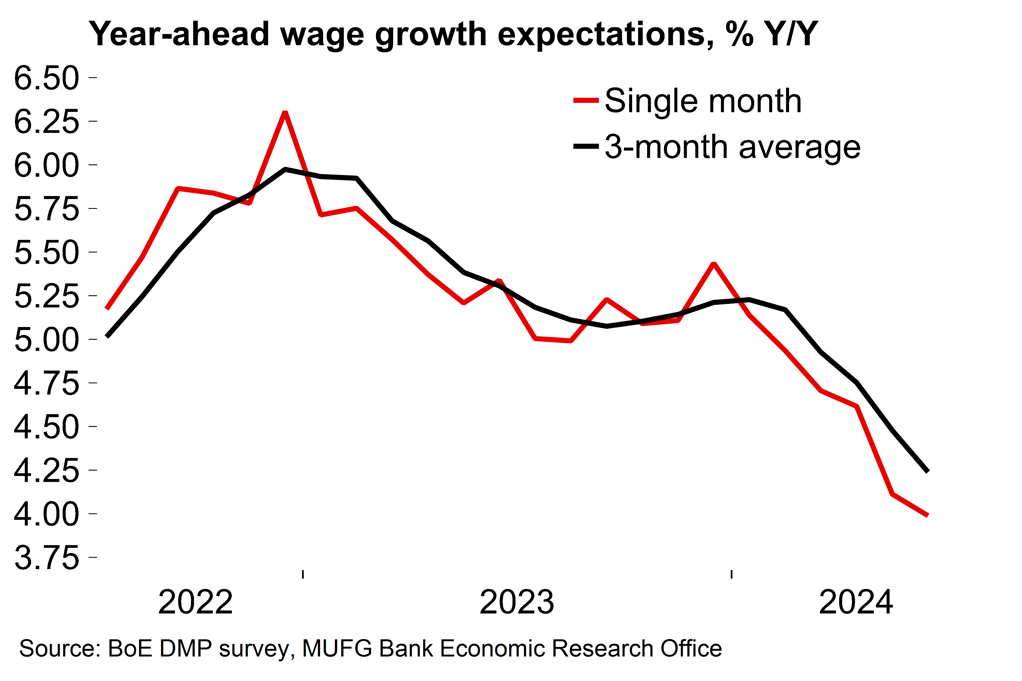

- The BoE may now feel free of political sensitivities around the election and policymakers could use speeches over coming weeks to firm up guidance around the timing of the initial rate cut. Closely-watched survey data this week pointed to continued easing of wage pressures which supports our view that the first cut will come at the next meeting in August.

**We have released our mid-year global macro update – see here**

A big Labour win, as expected

The Labour party won a landslide victory at yesterday’s UK election. With two seats yet to declare, Labour have 412 MPs and a 174-seat majority. The Conservative party now has just 121 MPs, a loss of 250. The Liberal Democrats, now with 71 MPs, gained 63 seats. Nigel Farage, the architect of Brexit, is now an MP for the first time. In another indication of rising right-wing populist sentiment in Europe, his Reform party achieved 14.3% of the national vote (but just 4 seats). However, the overall election result was in line with polling estimates and there was minimal market reaction.

Large majority, modest ambitions

Labour’s victory was achieved with a relatively small vote share (33.7%) under the UK’s first-past-the-post electoral system. There were some notable gains in long-held Conservative seats but the average margin of victory by constituency was relatively low. This points to broad but shallow support for Labour. Nevertheless, this result allows Labour to introduce the policies they set out in their manifesto with ease.

As we noted in our preview (see here) these policies are not especially ambitious. Some elements are growth-friendly, especially on planning reform. Construction could become an increasingly-important driver of activity in the UK. But there is a clear desire not to rock the boat when it comes to public finances. Labour’s manifesto suggests there will be just GBP 3.5bn of extra annual borrowing for investment – or 0.1% of GDP. Policymakers are likely treading carefully after the ill-fated Liz Truss ‘mini budget’ debacle, but we believe that there would be reasonable scope for extra borrowing without spooking market participants – especially if geared towards productive capex.

Labour have hinted at this with a tweak to the current fiscal rule (which limits the deficit to 3% of GDP in the fifth year of the forecast) by moving to a balanced day-to-day budget with additional borrowing for investment allowed. But the primary fiscal rule that debt-to-GDP should be falling over the medium-term, with no distinction made for whether that debt was accrued through borrowing for current or capital expenditure, will be retained. This limits the room for manoeuvre.

In terms of next steps, the new parliament will convene on Tuesday 9 July with the King’s Speech, where Labour’s legislative agenda will be formally set out, on 17 July. The first Budget event is likely to be in September or October (Labour has sensibly committed to just one major fiscal event a year). It’s possible that the fiscal rules could be adjusted beyond the manifesto proposals to carve out more space for investment. To our minds, it’s unlikely that would provoke much of a reaction in gilt markets provided a clear framework with OBR oversight is retained. Meanwhile we suspect that there will be some measures designed to increase revenues, perhaps with increases to capital gains/inheritance tax rates or tweaks to pension relief. Fiscal space under current plans is wafer-thin and it would otherwise be hard to fund any meaningful increases in expenditure on public services. This could be politically easier early on when it might be argued tax rises are necessary after some bean-counting due to mismanagement under the previous government.

Overall, drastic policy change seems unlikely under what looks to be a moderate and centrist government. The most significant shift is the return to political stability in the UK after the turbulence of the Brexit years. Labour have repeatedly highlighted that this will be a priority. Boring is generally good for businesses and we believe that increased stability is likely to support investment and activity more broadly. We remain cautiously optimistic on the UK economic outlook and our current forecast is for slightly above-consensus growth of 1.6% in 2025.

The BoE may now feel free to provide clearer guidance

On the BoE outlook, we look for the first rate cut at the next meeting in August (see here). The pre-election blackout period is now over and the BoE’s chief economist, Huw Pill, is due to speak next week. Free of political sensitivities, we suspect that policymakers could start to use speeches to firm up guidance around the timing of the first move, perhaps by providing more colour on the BoE’s reaction function to reduce the focus on services inflation prints. This week’s Decision Maker Panel survey data, which is closely watched by officials, was encouraging with wage expectations moving lower. There might be further evidence of increased labour market slack in next week’s REC report on jobs. That said, nominal pay growth, while a lagging indicator, is still high from a monetary policy perspective. We look for a gradual pace of rate cuts, with two moves this year.

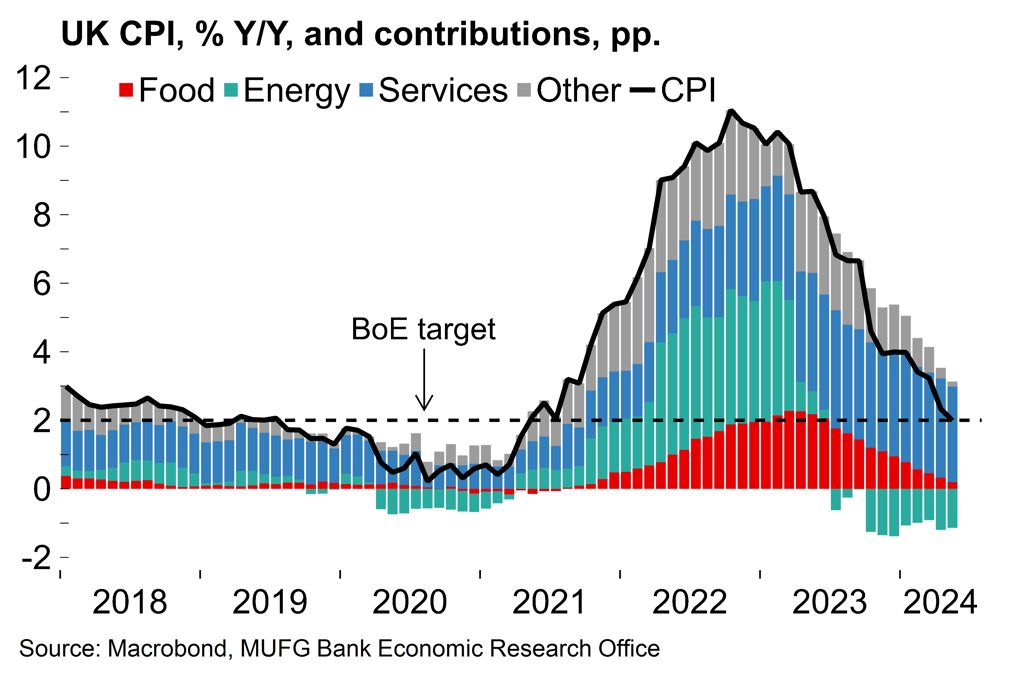

Chart 2: Headline inflation is back to target – but the services component is still a concern

Chart 3: The closely-watched DMP survey remains encouraging

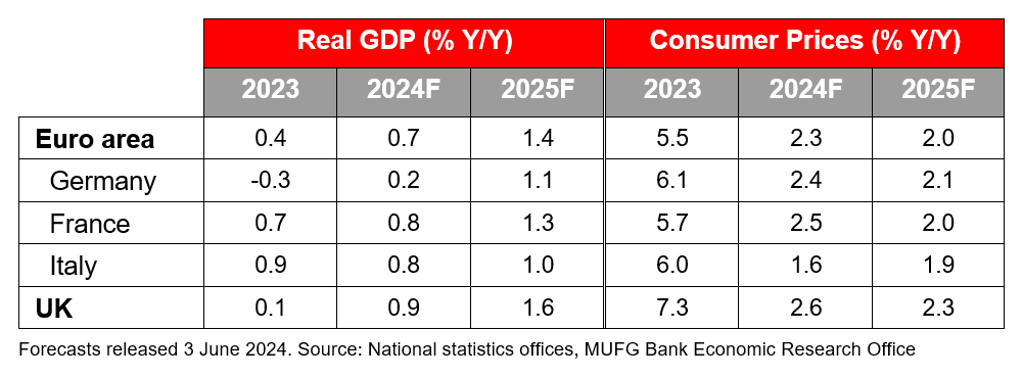

MUFG European Macro Outlook: Key points

- The euro area economy expanded by 0.3% Q/Q in the first quarter of the year, with all the major national economies growing at a faster-than-expected rate. The UK economy started the year strongly (0.7% Q/Q). While we look for slower growth rates in Q2, the recent uptick in momentum may well mark an inflection point after an extended period of stagnation. Broader growth conditions are set to continue to improve over coming months as real incomes recover and central banks start to ease policy.

- Nevertheless, it’s likely to be a case of moderate recovery this year rather than a rapid rebound. Business surveys have reinforced that message. The ECB followed through with its well-signposted cut in June, but the relatively hawkish tone suggested that policymakers remain wary about the inflation outlook. Monetary policy is set to remain in restrictive territory for some time. Meanwhile, many governments will need to make fiscal consolidation efforts after expansive spending in recent years, and structural pressures are set to continue to weigh on European manufacturing. The sudden increase in political risk following the announcement of a snap parliamentary election in France is also likely to weigh on sentiment. For these reasons we do not see growth sustainably exceeding potential this year or next. We expect average growth of 1.4% in the euro area in 2025 and 1.6% in the UK.

- Despite recent upside surprises in monthly inflation figures we expect that the disinflation process will reassert itself in H2 this year. Forward-looking survey indicators point to easing price pressures, household inflation expectations are well-anchored and there are mounting signs of increased slack in labour markets. We expect annual average euro area headline inflation will ease from 2.3% in 2024 to 2.0% next year. We expect a similar path in the UK, albeit with rates remaining slightly higher (2.3% in 2024).