Macro focus: Are we underestimating euro area growth risks? It’s now 12 weeks on from the start of the Iran conflict and evidence of a fragile euro area economy is mounting with the flash May PMIs dropping further into contraction territory. Other survey indicators look a touch more resilient and for now our base case remains flat Q2 GDP growth before a muted H2 recovery. But the euro area economy is clearly teetering close to a technical recession and we judge that there are downside risks around our already below-consensus 2026 forecast for growth of 0.6%.

What we’re watching next week: The focus now shifts to inflation with the first estimates of national HICP for May released next week. The German figure is set to slip back following government fuel support, but higher rates elsewhere will likely see the euro area aggregate move above 3% – and on course to hit 4% by year-end.

Macro Focus: Are we underestimating euro area growth risks?

Survey data increasingly points to softening activity – from a weak starting point

Our initial assumption was that the US-Iran conflict would last a matter of weeks rather than months (see here) – but it’s now 12 weeks on and we should probably start counting in the latter. The Hormuz problem is still proving intractable and the macro consequences of disruption will become increasingly visible in the data. We expected a below-consensus PMI reading this week but the slide was even sharper than feared. The composite figure fell to a 31-month low with the services component at the lowest mark since the pandemic.

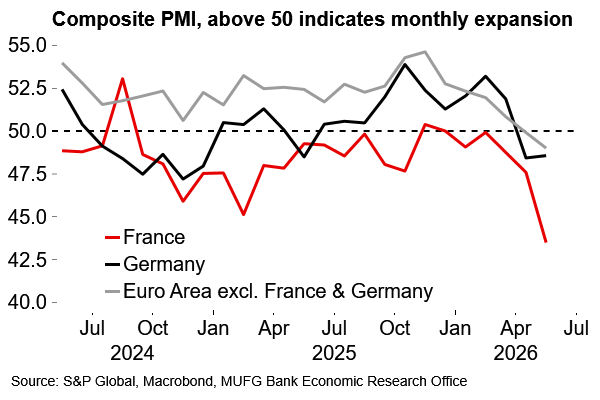

The euro area aggregate PMI was dragged down by a particularly weak French number (composite: 43.5). This looks out of kilter with a more resilient national French INSEE survey today. The German PMI, meanwhile, improved at the margin – and this was backed up by some improvement in the Ifo survey as well. It’s also worth noting that euro area consumer confidence edged higher in May. So, while the overall aggregate PMI alone is now consistent with a small Q2 GDP contraction, we stick with flat growth (i.e. 0%) in our base case. Beyond that we have pencilled in a muted expansion (~0.2% Q/Q) across H2. That is predicated on the assumption that eventual progress with Hormuz will lift confidence, but monetary tightening and delayed pass-through from the energy shock and wider supply chain disruption will prove a persistent headwind.

Our current quarterly profile leaves us expecting annual average euro area growth of 0.6% in 2026, which is 0.6pp below our pre-conflict baseline. This number is notably short of the European Commission’s latest forecast this week (0.9%, a 0.3pp downward revision), but we still worry about complacency on our part. Following muted Q1 growth (weighed down by volatile Irish data), it would take the mildest of technical recessions for growth to fall to the 0.4% mark set out in the ECB’s ‘severe’ scenario from March. The coming months will be a big test of the economy’s resilience.

It’s worth stressing that wholesale energy price developments, especially in gas, remain significantly more modest compared to 2022, and the economy has since shifted to a better-balanced energy supply mix. Support is set to come from the German fiscal boost, final NGEU disbursements, and AI-related activity. Labour markets are also still in reasonable shape with the euro area unemployment rate hovering around all-time lows.

But it is still a hefty terms-of-trade shock for Europe to bear and the economy is carrying less momentum compared to 2022. There is no boost from pent-up demand, households have lower savings buffers, and governments will be reluctant to roll out broad-based fiscal support given competing demands from defence and concerns around inflation. The ongoing competitive erosion from China in higher value-add trade is a long-term headwind.

Putting it all together, we still think it’s too soon to say that the economy is buckling into ‘non-linear adjustment’ territory. As discussed above, survey data, while certainly softer, is not flashing red. But we do think that a mild technical recession, at least, looks underpriced when we compare our forecast with the consensus.

France weighed heavily on the euro area PMI in May

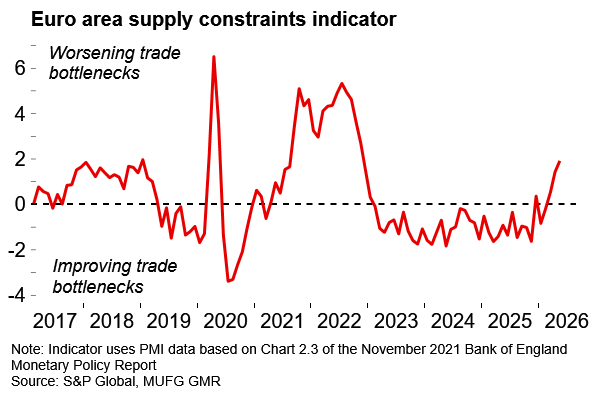

Evidence is emerging of worsening supply constraints

What we’re watching next week

Inflation to continue its upward march

The focus next week will be on the flash national inflation figures in the euro area. The German figure is likely to ease slightly following the government’s temporary fuel tax relief. We expect higher headline rates elsewhere, with the overall euro area aggregate (released the following Tuesday) moving above 3%. Further ahead, we think inflation will reach 4% by year-end. Elsewhere, we’ll be watching to see if the European Commission’s survey backs up the signals from the PMI discussed above. The ECB will also release the minutes from its April policy meeting. We continue to expect a rate hike at the next meeting in June with the central bank looking to keep a lid on second-round inflation risks.

Key data releases and events (week commencing Monday 25 May)

Day | Time | Region | Event | Period | Consensus | MUFG | Previous |

Thu 28 May | 10:00 | EC | Economic Confidence | May | 92.5 | 92.3 | 93.0 |

Thu 28 May | 12:30 | EC | ECB Account of Rate Decision | April | - | - | - |

Fri 29 May | 07:45 | FR | CPI EU Harmonized YoY | May P | 2.8 | 2.9 | 2.5 |

Fri 29 May | 08:55 | GE | Unemployment Change (000's) | May | 10.0k | - | 20.0k |

Fri 29 May | 10:00 | IT | CPI EU Harmonized YoY | May P | 3.3 | 3.2 | 2.8 |

Fri 29 May | 13:00 | GE | CPI EU Harmonized YoY | May P | 2.9 | 2.7 | 2.9 |

Note: All times are GMT+1 (London). Source: Bloomberg, MUFG GMR