To read the full report, please download the PDF above.

MENA Monthly Compendium

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

MENA Monthly Compendium

We are pleased to share in the link our latest MUFG MENA monthly compendium which aims to organise and highlight the array of themes surrounding the MENA region, from standalone thought leadership research, market developments and events to MUFG’s involvement on MENA related transactions as well as broader activities.

MUFG’s leading MENA regional financing for our clients

Since February 2024, MUFG was involved in the following prominent capital markets transactions:

- MUFG acted as Joint Lead Manager and Active Bookrunner for the Doha Bank PSQC ("Doha Bank") USD 500m RegS only 5-year bond offering. The transaction was an outstanding success, as illustrated by multiple milestones and achievements:

1. Securing a resoundingly strong order book of c. USD2.5bn (5x oversubscribed);

2. Healthy moves from IPTs to final landing levels of 35bps;

3. Pricing with a negative new issue premium; and

4. Attracting strong interest from high-quality international investors and thereby allocating more than half of the transaction with non-GCC accounts - including a robust interest from Asia with 18%.

MENA market perspectives

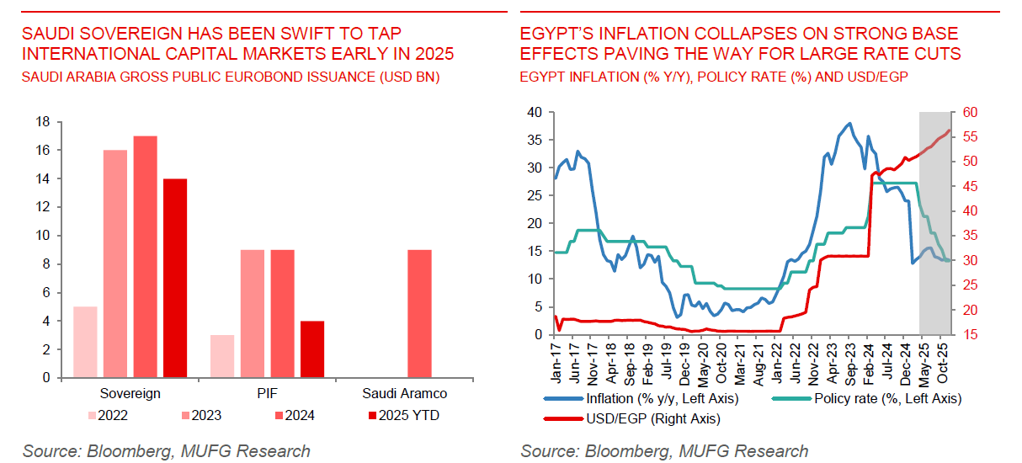

- Saudi Arabia issues its first sovereign green bond. Saudi Arabia has tapped international capital markets once again this year, this time around, issuing two Euro international bonds including its first ever green-bond. The two bonds were worth EUR2.25bn with the 7-year green one raising EUR1.5bn. This issuance, part of the Financial Sector Development Program, supports the Kingdom's goals of achieving net-zero emissions and advancing Saudi Vision 2030, while underscoring its commitment to investors and market participants. This follows the USD12bn issuance in January on the sovereign side and the USD4bn from PIF as financing needs remain large over major project spending and the linked twin deficit.

-

Strong base effects drive a collapse in Egypt’s inflation rate. Headline inflation in Egypt has declined from +23.9%yoy in January to 12.8% y/y in February (an 11.1ppt decrease). This represents a slight downside surprise to our (and consensus) expectations (MUFG: 13.8% y/y; consensus: 14.5% y/y). The predominant driver for the decline was the large base effects from the surge in recorded prices in February 2024 which witnessed the headline inflation rate surge by 11.4% m/m. Going forward, we forecast inflation to steadily rise to ~14.5% y/y between Q2-Q3 2025, and thereafter to recede to 13.4% y/y by year-end. Against this backdrop, we believe today’s current monetary policy stance is unduly restrictive, with real policy rates on a spot basis now ~15%. This should offer the Central bank of Egypt (CBE)t the space to promptly begin to ease rates, and we expect 600bps of cuts by end Q2 2025, with 400bps of easing at the next Monetary Policy Committee (MPC) meeting on 17 April. This should come despite the CBE’s still somewhat hawkish tone at its February MPC meeting where it flagged upside risks to the inflation outlook. While we acknowledge upside risks to inflation from global uncertainties, our benign inflation profile still allows the CBE to cut by an additional 800bps (cumulative) during H2 2025, to 13.25%.