To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil falls as US-Iran deal takes effect. Oil prices declined, with Brent falling toward USD78/b and WTI near USD76/b, as the US-Iran interim peace agreement formally took effect and markets shifted focus to the reopening of the Strait of Hormuz. The deal is expected to facilitate a gradual recovery in Gulf oil exports, including the return of Iranian crude to global markets and higher production from regional producers. While the industry remains cautious about the pace of normalisation, some tankers have already resumed movements and exporters such as Iraq are preparing to increase shipments. The prospect of additional supply has erased most of the war-related oil price premium, although global inventories remain tight, particularly in the US where crude stockpiles are near operational minimum levels. Overall, the agreement marks a significant step toward easing supply constraints and reducing pressure on global energy markets.

Gold gains despite hawkish Fed outlook. Gold rose to around USD4,330/oz after the US and Iran formally signed an interim peace agreement, helping ease concerns over the energy shock triggered by the conflict. The prospect of lower oil prices and a gradual reopening of the Strait of Hormuz supported market sentiment, although uncertainty remains over how quickly energy flows and fuel prices will normalise. Despite the positive geopolitical developments, gains in gold were tempered by the Fed’s hawkish stance, as policymakers kept rates unchanged but signalled the possibility of a rate hike later this year. In our view, gold is likely to remain under pressure in the near term as easing geopolitical risks, falling oil prices, and expectations of tighter monetary policy reduce demand for safe haven assets.

MIDDLE EAST - CREDIT TRADING

End of day comment – 17 June 2026. Cash prices lower/ UST unchanged to higher is a toxic combo for spread longs. Buyers are on strike, most likely awaiting the FOMC. Sellers though continued selling, and it was again concentrated in UAE index names. The move of the last 2 days wider brings us even wider than Friday morning when hopes were building for an imminent Iran deal. In terms of flows RM and ETF were sellers and the local bid was focused on some specific bonds only. ADGB is going out up to -0.625pt and 3/8bp wider with long end underperforming, 54s closed -0.625pt/+8bp. QATAR saw the same pattern but once again outperformed ADGB a touch, 50s closed -0.375pt/+5bp and into the close there is some activity in 10y bonds with 35s going out -0.25pt/+5bp. SHARSK/SHJGOV/OMAN outperformed and that tells you what international accounts are (not) holding, belly bonds in the 3 names closed unchanged and long end -0.125pt/+3bp. Quasis were quiet but followed sovgn moves, MUBAUH feels especially heavy but didn't found clearing levels and the curve is marked +3/8bp. Fins and corps were on the quiet side and are somewhat shielded from the index outflows. (Source: Dominik Roth, Credit Trader)

MIDDLE EAST - MACRO / MARKETS

UAE accelerates strategy to reduce Hormuz dependence. The UAE announced plans to significantly reduce its long-term reliance on the Strait of Hormuz despite the expected reopening of the waterway. The strategy includes expanding the eastern ports of Fujairah, Khor Fakkan, and Dibba, constructing additional ports outside the Gulf, and investing heavily in new oil pipelines, railways, and road infrastructure to strengthen alternative export routes. The UAE is also fast-tracking a second Fujairah oil pipeline and exploring further energy export infrastructure to support crude, petrochemicals, and LNG shipments. The conflict highlighted the strategic vulnerability of Hormuz, prompting the UAE to accelerate efforts to diversify its logistics network and enhance supply-chain resilience. While Hormuz remains critical to regional trade and energy flows, the UAE aims to strengthen its position as a regional trade and energy hub by reducing exposure to future geopolitical disruptions and improving connectivity between its production centers and eastern coastline export facilities.

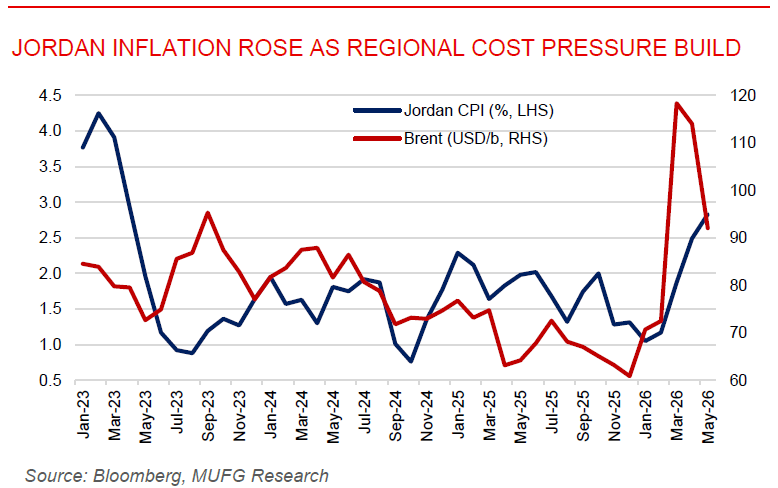

Jordan inflation accelerates as regional cost pressures build. Jordan’s inflation rate accelerated to 2.8% y/y in May 2026, up from 2.5% in April, marking the fastest pace of price growth in more than a year and suggesting that higher energy and import costs linked to the regional conflict are increasingly feeding into the domestic economy. While inflation remains moderate by regional standards, the upward trend signals growing price pressures in Jordan’s import-dependent economy and may encourage the Central Bank of Jordan to remain cautious in following any future Federal Reserve easing. Despite rising inflation, Jordan’s broader economic outlook remains relatively resilient, supported by stronger exports, a narrowing trade deficit, and the country’s growing role as a regional logistics and trade hub. The key question for the second half of 2026 is whether recent inflation pressures prove temporary as energy prices ease and trade routes normalise or evolve into a more persistent trend.