To read the full report, please download the PDF above.

Middle East Daily

SOOJIN KIM

Research Analyst

DIFC Branch – Dubai

T: +44(4)387 5031

E: soojin.kim@ae.mufg.jp

MUFG Bank, Ltd. and MUFG Securities plc

A member of MUFG, a global financial group

Middle East Daily

COMMODITIES / ENERGY

Oil rebounds as Iran negotiations face new obstacles. Oil prices rose after three consecutive sessions of declines as renewed uncertainty surrounding US-Iran negotiations damped optimism over a near-term resolution to the conflict. Brent climbed above USD104/b while WTI traded near USD98/b, with markets reacting to comments from Iran’s leadership insisting on retaining its uranium stockpile and disputes over control and tolls in the Strait of Hormuz. Although Iran said the latest US proposal had narrowed differences between both sides, conflicting signals from officials continued to cloud prospects for a breakthrough and a full reopening of the vital energy shipping route. The prolonged disruption in Hormuz has driven a sharp drawdown in global crude and fuel inventories, while the IEA reiterated its readiness to release additional emergency stockpiles if supply pressures intensify further.

Gold range bound as mixed Iran signals keep inflation concerns alive. Gold traded in narrow range near USD4,540/oz as conflicting signals surrounding US-Iran negotiations keep markets uncertain over the outlook for inflation and interest rates. While reports suggested recent talks had narrowed difference between both sides, comments from Iran’s leadership on retaining its uranium stockpile and disputes over the future management of the Strait of Hormuz continued to cloud prospects for a final agreement. The uncertainty has sustained concerns that elevated energy prices could keep global inflation pressure high, potentially forcing the Fed and other central banks to maintain higher interest rates for longer. Gold, which typically benefits from lower-rate environments, has therefore remained under pressure and is still down nearly 14% since the conflict began in late February, despite ongoing geopolitical risks.

MIDDLE EAST - CREDIT TRADING

End of day comment – 21 May 2026. Ydays tone was weak on a global risk on day, todays tone was strong on a global risk off day. Flows were balanced with a bit more ETF selling into the close, but the market largely ignored Iran related headlines nor did they altered flows meaningfully. There was especially a strong bid in long end IG bonds, led by QATAR long end where 50s closed +0.5pt/-6bp whereas ADGB 54s closed +0.25pt/-3bp. Quasi sovereigns had a quieter day, most activity was in ADQABU 54s which closed +0.5pt/-5bp. Financials were broadly flattish in cash price (-2/-3bp), new OMAB perp saw little activity and closed just wrapped around reoffer 100. Corps saw strength in DPWDU early morning, here as well especially in long end bonds (48s +0.75pt/-8bp) but into the close there are offers coming in at these higher levels. Overall, after the volatility into the close yday the market is still 1/2bp wider over two days in the main sovgn/ quasi names. Activity levels continue to decrease as the US-Iran standoff continues and a long weekend is already around the corner.

MIDDLE EAST - MACRO / MARKETS

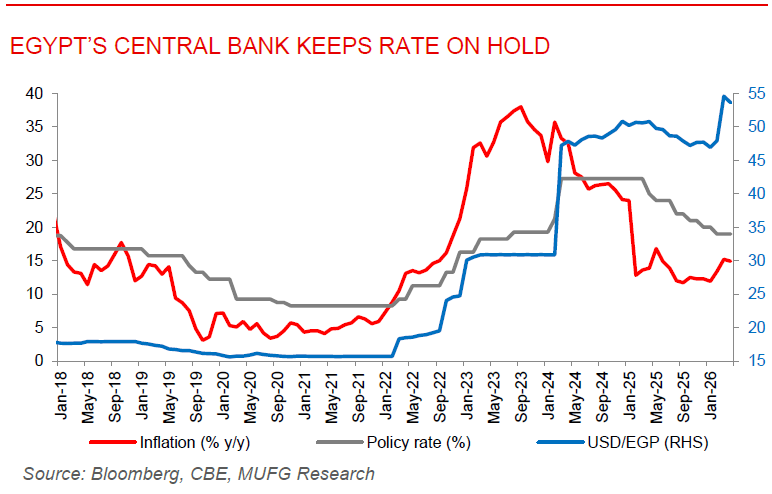

Egypt’s Central Bank keeps rate on hold as inflation risks remain elevated. Egypt’s central bank (CBE) left interest rates unchanged at 19% for deposits and 20% for lending, extending its cautious wait-and-see approach as policymakers balance slowing inflation against mounting risks from the Iran war and higher energy prices. The decision followed an unexpected decline in annual inflation to 14.9% in April from 15.2% previously, despite the sharp rise in oil and gas costs triggered by disruptions in the Strait of Hormuz. The CBE acknowledged that inflation is likely to accelerate again during the second half of 2026 due to exchange rate pressure, fiscal consolidation measure, and the delayed impact of higher fuel costs. Going forward, we expect rate to remain elevated throughout 2026, with some warning that prolonged energy market disruptions could even trigger additional tightening later this year. Meanwhile, Egypt continues to face external vulnerabilities from weaker Suez Canal revenues, tourism pressures, and FX volatility, although resilient remittances, IMF support, and improved policy flexibility have helped strengthen the economy’s resilience compared with previous crisis.

Turkey slashes US treasury holdings to defend the lira. Turkey sharply reduced its holdings of US Treasuries in March, cutting them to just USD1.8bn from USD16bn a month earlier, as authorities intensified efforts to stabilise the lira during the early stage of the Iran war. The selloff coincided with heightened pressure on Turkish markets after rising oil prices and regional instability triggered capital outflows and currency weakness. To support the lira, the central bank tightened funding conditions and intervened through foreign exchange and gold sales, including swaps involving gold reserves. Despite these measures, the currency has remained under pressure as the conflict continues, while inflation accelerated to 32.4% and bond yields climbed to record highs. The sharp reduction in Treasury holdings also highlights how geopolitical tensions and external shocks are straining Turkey’s reserve position and complicating efforts to restore macroeconomic stability.